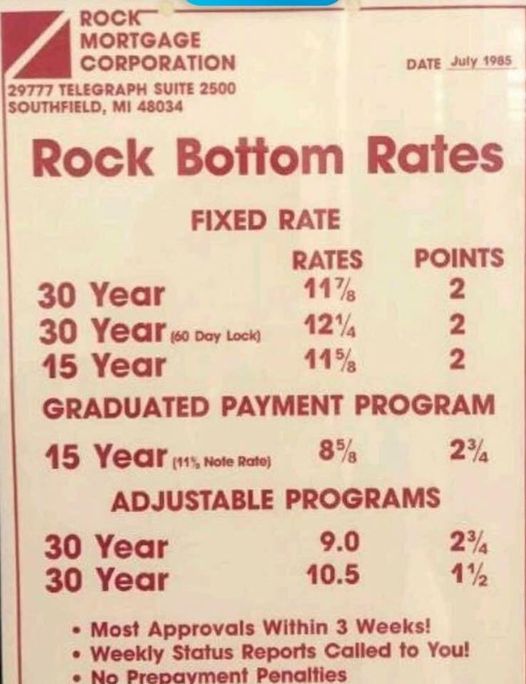

Mortgage rates in July, 1985

After the TV show, Derrick and I were discussing the good old days when homes were cheap and everyone moved often. He is a mortgage originator, so I asked him how many adjustable loans he has done this year.

His answer? None.

Back in the day, adjustable-rate mortgages were the preferred product. Look at the difference:

$300,000 loan amount

Monthly payment at 11.875% = $3,057

Monthly payment at 9.0% = $2,414

Difference = $643 per month!

Nobody looked too hard at the terms of the ARM because a) $643 per month was a ton of money back then, and b) no one planned to stay forever. Home buyers could always refinance if they had to, but many solved their ARM concerns by moving again – heck, there were lots of homes for sale!

Then the 2-out-of-5-year tax exemption was passed in 1997 which really juiced the market. Homeowners were rewarded with tax-free money for moving!

It was rare that anyone had the full $500,000 in net profit, mostly due to the lower home prices and because of other recent moves. Yet many moved again just to say they got their tax-free money!

At the same time, the mortgage industry, led by Countrywide, flooded the market with an alternative – the interest-only mortgage with a rate that was fixed for the initial period, and you could choose 3, 5, 7 or 10 years. Once those saturated the market, Countrywide stole the neg-am ARM idea from the S&Ls and spiked them with high margins, and, well, we know how that ended.

As the private mortgage companies exited the market, the government lowered rates, and backed Fannie/Freddie to provide market liquidity. For the last ten years, the only program being offered is the 30-year fixed rate mortgage, and because rates are so much lower than before, buyers didn’t mind.

The end result? Today, you never hear anyone buying a home for the short-term.

The combination of ultra-low rates and difficulty of finding a better home has locked in everyone into their current home. Even if the current home becomes unsuitable, it beats moving again.

The low-inventory era is here to stay, and will likely get worse.

My first home in 1991 was at 11.75% fixed for 10 years and amortized over 30 years. Bought home for $350k and dropped to $275k in 1998 and now sells for $1,300,000 at 3% fixed for 30 years.

What will happen when the tide ever goes out again? Will everyone be wearing a swim suit? Time will tell. Cash is king and equity is queen at low tide.

Also not a thing these days: assumable loans. I remember in the 80s it was popular to assume the seller’s low interest loan rather than try to get an 8-12% loan of your own. Lenders put an end to that.

The 5- or 10-year balloon payment was another popular tool for getting the monthly to a manageable size. As you said, just move again.

On a different topic, what do you think of this?

https://www.screaltors.org/problems-fair-housing-love-letters-revealing-protected-class-kids-race-disability/

“Sellers should not Facebook stalk buyers.”

Signing to close for my first home to actually live in late 80s they spring a new condition. Our adjustable rate loan tied to the 11th District cost of funds had a floor. I almost backed out. They thought I was crazy. Wasn’t crazy.

Ross,

If rates ever do rise significantly (doubtful because the Fed will keep manipulating), I can imagine a lot of creative rent-to-own contracts to keep the original financing in place.

Ross – The YouTube video in that article is awesome!

A heart-to-heart about ‘buyer love letters’ in real estate

https://youtu.be/xlO4jPFbnHk

“Sellers should not Facebook stalk buyers.”

The whole game is so in favor of the sellers, it makes you wonder when or if anyone will ever stand up and say, “hey, what about the buyers?”

We declare ‘no love letters’ and pretend that is enough to deter racism in the decision-making process. But if sellers want to Facebook-stalk the buyers and make decisions on what they find, can you stop them? Not really.

I’ve had two cases this year where my buyers made offers and lost on properties that, when they closed, we found that the winner offered the same price.

My clients were black.

In both cases, the listing agents were present for the showings.

If we made identical offers, how did they pick the winner? If the seller happen to ask the listing agent for some information about the buyers, did he happen to mention that they were black? And if he did, don’t I have a criminal case for discrimination? I think so.

Both were over $2,000,000 in toney neighborhoods.

In the one case where I got the listing agent on the phone (I had to call him from a different phone), he said the reason he took the other offer was because they offered a 28-day escrow, and we offered 45 days.

But you didn’t give me a chance. You didn’t tell me another offer came in after ours that coincidentally happened to match our price which was 22.5% over list so hard to imagine that they hit that exact number without you tipping them to the price.

It was like you were out to get us from the beginning.

Either you are a weak spineless bastard who has no intention to play fair with other agents, or you are a discriminating racist. Take your pick.

This is the real world of real estate.

Jim, this is why I am in full support of a live auction. No listing agent bullshit. Biggest wallet wins.