Earlier this year, I speculated that the market could endure – and probably snap up – additional inventory, as compared to last year. The 2023 inventory was like the Mohave Desert!

It seemed that 10% to 15% more would be easily digested, and maybe even +20% or +25%.

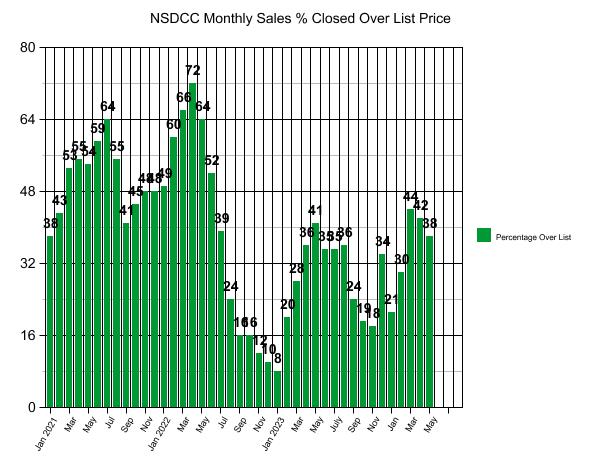

Bill’s new stats out today suggest how much, is too much:

Sales that close over their list price are tapering off now.

It’s not as bad as it was in 2022 when rates began their rise, but you can see that last year the percentage was steady through summer. Maybe our faster start this year exhausted the enthusiasm earlier?

Of the 38% of sales that closed over list, just over half of them were under $2,000,000.

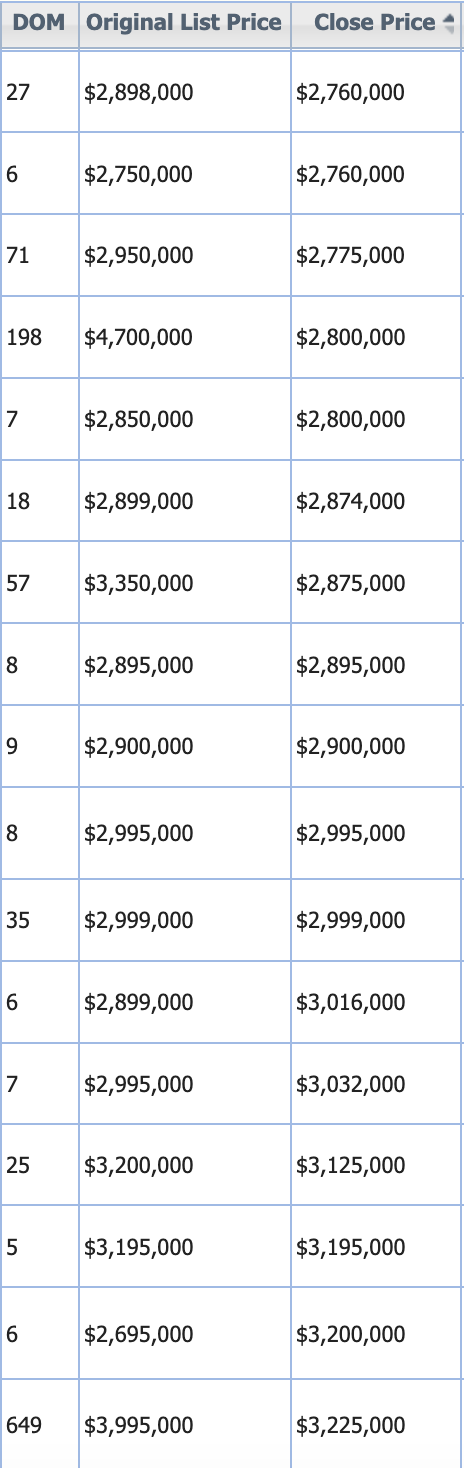

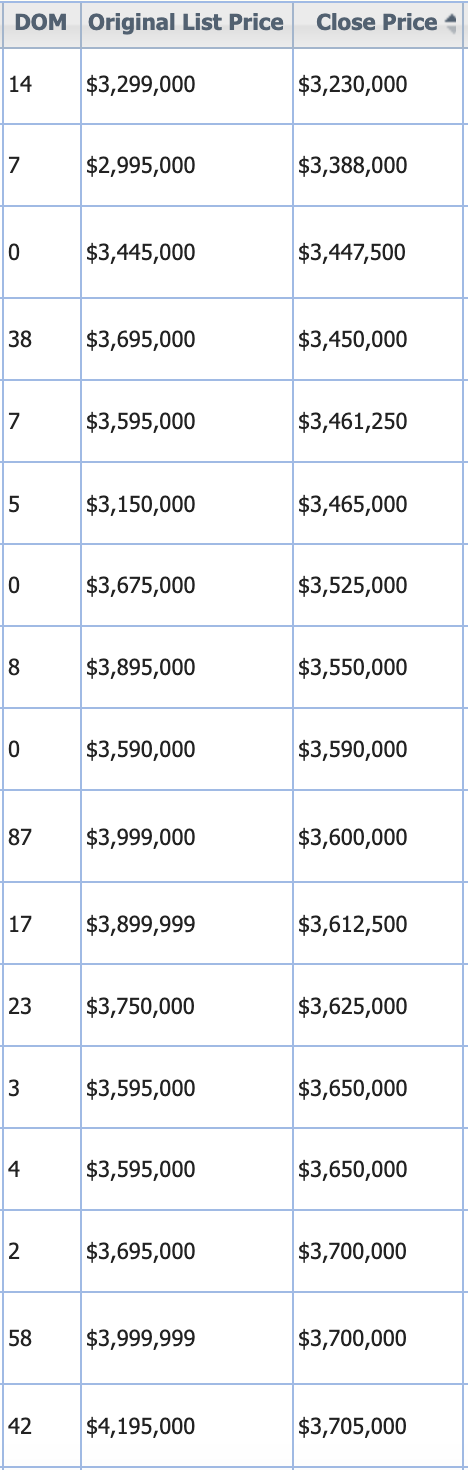

The pricing enthusiasm is cooling off too. Note the relationships between the DOM (days on market) and the discounts below. Exactly NONE of the these homes sold over their list price after they were on the market more than seven days:

Yesterday’s blog post identified one solution for buyers which we’ll call the Gunslinger Special – where you wait patiently for the perfect home and when it hits the market, call JtR and give it everything you got.

What are the other options?

First, let’s note that you will get credit for any seller contribution to the buyer-agent fee. On my 2% Gunslinger Special, I’m going to try to get the seller to pay all of it, and sellers who are offering 2.5% means you get the 0.5% extra paid towards your closing costs. The form you will sign states this clearly, and it will apply to any agent you hire.

But it will be smart to expect to pay all the fee, and if the seller happens to pay some or all of it, then yippee. Why? Because the hot buys – the houses you want to buy – will probably have multiple offers. You don’t want to lose out because you insisted that the seller pay some of your agent fee. Eventually, there won’t be any seller contributions any more, it is just how fast we get there.

Option B – You are early in your search, and you’ve already experienced the pesky open-house agents hounding you to sign an exclusive-representation agreement. But the idea doesn’t sound too bad because you know you need to hire an agent to see homes for sale that aren’t open houses, and you wouldn’t mind the extra help.

Their fees will vary wildly. Any agent who is charging 1% or less is only looking to open a few doors and have a $500 transaction coordinator manage the paperwork for you. Those who charge more will razzle-dazzle you with their list of 10,000 Things I Do For You.

Have them show you one house as a trial before signing. If they say anything about a “dream home” or only identify the name of the rooms when touring the house (“here’s the kitchen”), know that you can do much better when hiring an agent.

You will end up making a decision based on your gut feeling, but no matter who you hire, check their Zillow profile. Punch their name and the word Zillow into Google search, and it will pop right up. Here’s mine:

If the agent works on a team, read through the reviews to find their sales and see what their buyers had to say. Being the “Neighborhood Expert” isn’t nearly as important as having a solid and recent history of closing sales with buyers.

When you go to sign their form, choose the option that you can cancel any time.

Option C – Go direct to the listing agent. Don’t do this just to get a piece of the commission by reducing the price or having them pay your closing costs – it’s doubtful either will happen. Go direct to the listing agent only if you are absolutely desperate to buy this home. It’s likely that you’ll still have to pay well over list and get little or no help, but hey, you should get the house!

You will still have to hire them as your agent to buy the house, and it is inevitable that every listing agent will have you sign this form to say you are unrepresented, and they don’t owe you anything. It will make you think about getting good help on your side, but once you engage with them, it will be too late. They will hold it against you and sell the house to anyone else just tp teach you a lesson.

All of these options are terrible, and I apologize on behalf of the real estate industrial complex for screwing up this lawsuit so bad that it makes home-buying more difficult. Trying to buy a house is difficult enough!

If you want to avoid this misery, buy a house before August!

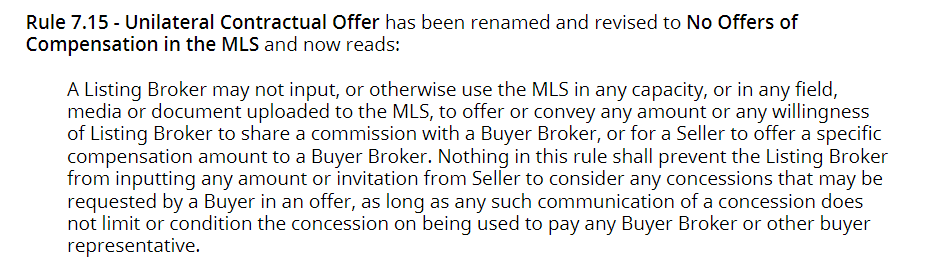

In mid-August, the new rule takes effect that NO buyer-agent commissions will be advertised on the MLS. Technically, sellers paying commissions to the buyer-agents will still be allowed for now – they just have to be negotiated outside of the MLS. There will be attempts to circumvent the new rule (see above), but sellers are going to think that they don’t need to pay anything.

I think we can expect seller-paid commissions to the buyer-agents to dwindle down to zero in the next 6-12 months. The DOJ has not insisted on this yet, but their attorney said the other day that they want the commissions decoupled, so it’s coming.

What’s next?

Buyers need to start getting used to the idea of paying for their agent.

Buyers will be required to hire a buyer-agent in writing to see homes, an idea that doesn’t sound great to anyone. Buyers don’t think they need an agent when they have Zillow at their fingertips, and agents will struggle to convince you that you need sign any agreement when you’re just looking.

I don’t want to be at your beck and call for the next 6-12 months and have to show you homes that I know you aren’t going to buy. But because we have a contractual agreement, you’ll be thinking……”hey, we hired you to be our agent, so snap to it.”

My Proposal:

You monitor Zillow via auto-notifications, and go to open houses all you want. You will be peppered by agents wanting you to sign an exclusive agreement for a year or two with the promise of showing you off-market deals that you won’t see on Zillow.

If you can resist that shady ploy, then when you finally find “the house” online, then I’ll get it for you. We will sign the agreement when I show you the house, and the agreement will be for this house only.

You’ll pay me 2% at close of escrow, with this guarantee:

If I don’t get you the house, you don’t have to pay me anything.

I’ll be the real estate gunslinger who will take care of business for you!

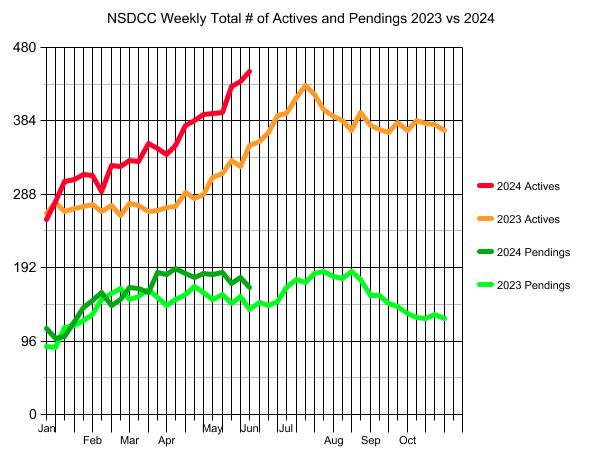

None of the pricing metrics are great but at least they demonstrate the trends over time. These graphs above are showing the latest data, including last month, and it’s all fairly positive….for now. With the extra inventory, buyers aren’t going to pay crazy money unless they see the perfect house. Sellers aren’t going to give them away though, so the trend for the rest of 2024 should be flat.

These graphs are interactive so scroll over to see the numbers.

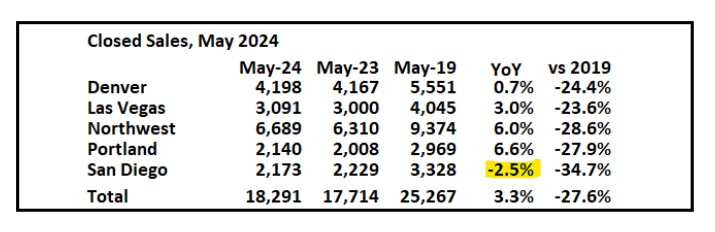

There is extra unsold inventory but nobody is going to call this a flood, especially vs. 2019:

Sales will suffer as long as rates and prices are high. Have we gotten used to having fewer sales yet? The trend is going to last a while – probably for years to come:

It looks like the home-selling season is losing any momentum it had in March-May when the pendings that closed escrow were being steadily replaced.

You can see that we had a mid-summer spurt of pendings last year, but with the political circus ramping up and buyer-agents being shown the door, I doubt that there will be any big breakout of new pendings for the rest of this year.

Our home values have been detached from “key economic factors” for years. More interesting would be studies that analyze what would happen to areas that are full of the older tract homes (1980s and before) that haven’t been improved much and are dumped onto the market for sale by money-grabbing heirs who just want fast cash. There could be a pricing downdraft of 10% to 15% in very short time – like a month or two.

Southern California home prices may seem insanely high, but two yardsticks of their underlying values suggest they’re not as crazy as elsewhere in the nation.

Let’s be clear. These measurements don’t say local homes are affordable. Nor does this math conclude what buyers are paying is normal. Rather, these studies show the overvaluation of Southern California homes compared with historical patterns is not massive on a national scale.

The first study is from Fitch Ratings, a Wall Street credit-quality tracking company. It compared pricing patterns in 50 U.S. metropolitan areas at year-end 2023 with key economic factors such as employment, interest rates and rents.

The other review is by two professors from Florida Atlantic University. Their price momentum model contrasted home prices in 100 metros for March 2024 with how costs gyrated over the long haul.

Fitch found one local problem spot: San Diego.

Its home prices, up 6.2 percent last year, were calculated to be 15 percent to 19 percent too high at 2023’s end, by this math. That’s the second-highest level of risk in the study.

Contrast that to Los Angeles and Orange counties, where prices rose 4.9 percent last year. Those homes were 5 percent to 9 percent overvalued at year’s end — the same risk score as the Inland Empire, where prices rose 2.1 percent last year.

The FAU professors pegged Inland Empire homes as the region’s most overvalued. The IE’s $579,000 typical house was 25 percent above its expected value in March 2024 — but that was only the 45th-largest overvaluation of 100 metros tracked nationally.

Homes in San Diego, worth $947,000, were 24 percent too high, by this math — the No. 50 overvaluation nationally. And in L.A.-O.C., with home prices running $947,000, overvaluation was 14 percent — the No. 85 overvaluation nationally.

Bottom line

The gaps between the two scorecards are a perfect example of what I’ve long said: The creation of any national ranking is part statistical science and part art. Just eyeball the most overvalued markets.

Fitch found seven metros were 20 percent to 24 percent overvalued: Memphis, Tenn.; Raleigh, N.C.; Indianapolis; Milwaukee; Nashville, Tenn.; Buffalo, N.Y.; and Birmingham, Ala. FAU’s top seven were: Atlanta (41 percent too high); Detroit (40 percent); Cape Coral, Fla. (39 percent); Tampa, Fla.; and Las Vegas at 38 percent, then Knoxville, Tenn., and Palm Bay, Fla., at 37 percent.

Or look at the differing levels of overvaluations.

Fitch graded all U.S. homes as 11% overvalued, with 44 of the 50 metros it tracked seen as overvalued by 5 percent or more. FAU’s median U.S. overvaluation was more than double — 24 percent with 97 of 100 metros tracked overvalued by 5 percent or more.

Or look at two Bay Area markets.

Fitch sees both San Francisco and San Jose as risky as San Diego — 15 percent to 19 percent overvalued.

But FAU professors have San Jose with their 15th-lowest risk (14 percent too high) and San Francisco with the third-smallest (2 percent too high).

Quotable

Contemplate the deviation in the national outlooks of the studies, too.

Fitch wrote that it “expects nominal national home price growth to decelerate from 5.5 percent in 2023 to 0 percent to 3 percent in 2024, which signifies the slowest pace since 2019. This forecast is based on the interplay between multiple factors, such as affordability challenges and a tight supply of homes, with the latter the more dominant factor in sustaining positive home price growth.”

FAU professor Ken Johnson wrote: “Home prices have become so out of line from their long-term trends that the risk of correction is rising. While it’s unlikely prices will plummet dramatically, price performance could go flat for the future, or home prices could see a slight decline even.”

Lansner is the business columnist for the Southern California News Group.

San Diego is a dream for many retirees. It offers nearly continuous sunshine, great restaurants and plenty of activities to keep you busy. Unfortunately, it’s also extremely expensive. According to Zillow, the average San Diego home price is $1.03 million.

If you’re seeking a warm, tropical location to enjoy your retirement, San Diego might not fit into your budget. Luckily, there are many other locations that offer the same great features of San Diego, without the price tag.

Myrtle Beach, South Carolina

The first location, Myrtle Beach, might be on the opposite side of the country, but it’s a popular spot for retirees. With an average home price of $307,680, owning a home will be much more affordable.

Similar to San Diego, Myrtle Beach is a tourist destination. Its population increases significantly during the summer months, with people coming to enjoy the great beach weather. But don’t let the crowds scare you away — Myrtle Beach has a great laid-back vibe.

One of the best aspects of Myrtle Beach is the abundance of things to do. Located on the Atlantic Ocean and near numerous lakes, there’s an endless supply of fishing holes to enjoy. Plus, the area has more than 90 golf courses. Myrtle Beach is also home to many great restaurants, breweries and distilleries.

One more reason to consider Myrtle Beach is that South Carolina is a tax-friendly state for retirees. Social Security benefits are not taxed, and retirees can enjoy a $10,000 taxable income deduction on other sources of retirement income.

A mini-ranch in Leucadia just sold for a little over the list price. Calling this a four bedroom is a stretch, but it had enough funky-cool to be an eclectic dream home for someone. Another all-cash buy too.

There will be fewer agents, which is a good thing. There are 20,000+ realtors in San Diego County, and last month there were 2,113 sales of attached and detached homes. Hat tip to Greg for sending in this article!

When real estate broker April Strickland looks at her local housing market in Gainesville, Fla., she sees a mismatch. Industry data shows that only a few hundred homes are sold each month, she said, yet there are more than 1,500 local Realtors.

Strickland has seen the ups and downs of the housing market since 1995, when she started managing her parents’ rental properties as a teenager. But she says the business environment of the past two years is the most challenging she can remember — slower even than the years following the 2008 financial crisis.

“Quite frankly, Realtors are running out of money,” Strickland said.

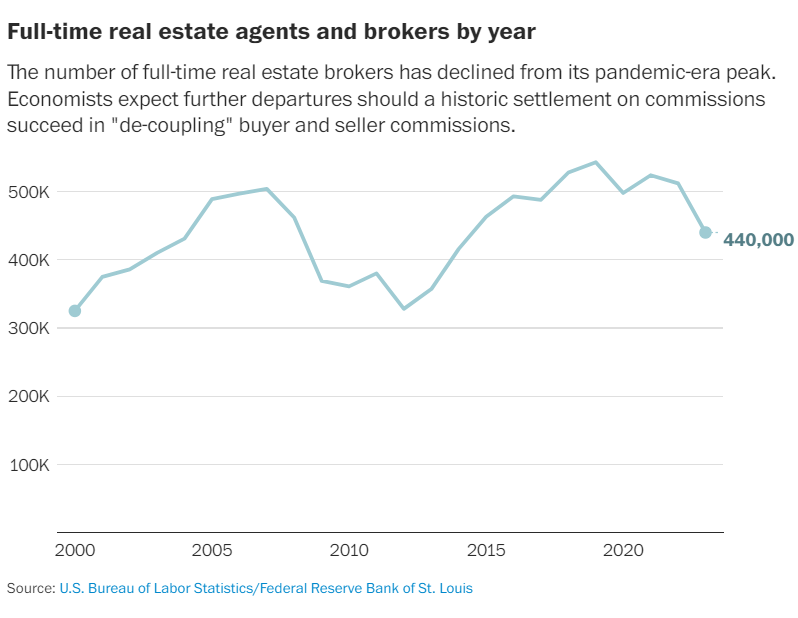

An industry that swelled with newcomers in 2020 and 2021 has recently experienced a harsh slowdown — leaving the field no choice but to downsize, experts say. One widely cited analysis predicts that as many as 80 percent of the country’s real estate agents could find a new line of work.

“Many industry leaders think there are way too many agents and would like to reduce the number so the professionals can service more clients, thus allowing a reduction in commission levels in order to maintain current incomes,” said Steve Brobeck, a senior fellow at the Consumer Federation of America.

By some measures, the exodus has already begun.

The Bureau of Labor Statistics recorded 440,000 full-time real estate agents and brokers in 2023, about 72,000 fewer than the year before.

Realtors will soon face new rules that could result in sweeping changes to how they do business and how they get paid.

Under the new rules starting in August, real estate databases no longer will include offers of compensation for buyers’ agents. That means those agents can no longer count on a cut of the seller’s windfall. Investment bank Keefe Bruyette & Woods has estimated that as much as 30 percent of the total U.S. commissions revenue might be lost as a result. They forecast that changes to the commission structure could cause 60 to 80 percent of U.S. Realtors to leave the profession.

CUNY Baruch College’s Sonia Gilbukh and Yale School of Management’s Paul Goldsmith-Pinkham estimated that about 56 percent of agents would exit the market if one side’s commission remained at 3 percent while the other became competitive, Gilbukh said in an email describing the study. A 2015 paper in the Rand Journal of Economics by Panle Jia Barwick and Parag Pathak predicted that a 50 percent reduction in commissions would result in 40 percent fewer agents.

Experts see a silver lining in a potential exodus of Realtors: Those who remain might be more experienced and competent. “This will be good for consumers because agents on average will be better at their job and will charge more competitive commissions,” Gilbukh said.

A “Realtor glut” has persisted since the industry’s pandemic high point, said Brobeck, who also sees a departure of real estate agents as probably a good thing for home buyers.

Gilbukh, the CUNY researcher, believes that only the most experienced agents will be able to keep charging high commissions.

Agents that survive the upcoming transition are likely to be better connected within their industry, having deeper relationships with professionals such as contractors, electricians, plumbers and appraisers, and “overall better poised to advise their clients,” Gilbukh said.

The proposedNAR deal was met with fear throughout the industry when it was announced in March, Strickland said. But the panic has given way to a “wait-and-see” attitude, she said.

She characterized the NAR deal as a positive thing overall:

“It will eliminate people who quite frankly aren’t up to snuff, who can’t do the work, who don’t want to educate themselves and learn new ways or working. … This will be a good pivot for our industry.”