Millennials aren’t buying homes in the same numbers as previous and older generations, but it’s not because they don’t want to. The vast majority of millennials do indeed aim to buy someday, or would even like to now if they could. Unfortunately, the numbers don’t look good.

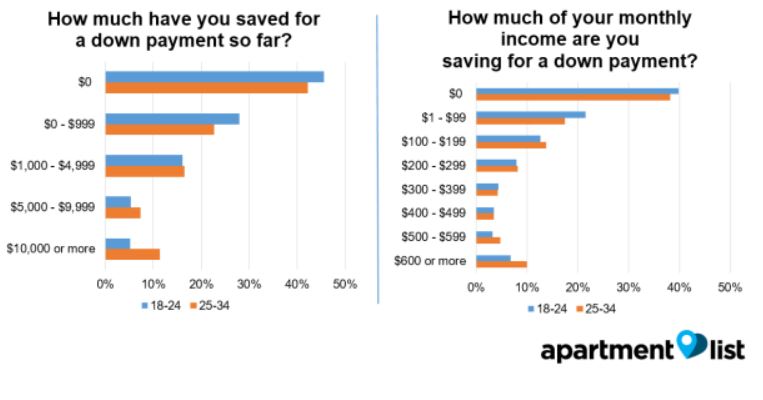

New data from Apartment List shows that, although 80 percent of millennials would like to purchase real estate, very few are in a good position to buy, largely because they have nothing saved. According to the report, “68 percent of millennials said they have saved less than $1,000 for a down payment. Almost half, or 44 percent, of millennials said they have not saved anything for a down payment.”

Depending on where they are looking to buy, given their current savings rate, millennials are 10 years or more away from home ownership. Young residents of pricey San Jose, Calif., will have to be exceptionally patient: Odds are they won’t be in a good position to buy an apartment there for “almost 24 years,” or “until the year 2041.”

Apartment List reports that millennials in San Francisco, San Diego, Los Angeles, Austin and other major metro areas each “face a wait of at least 19 years”.

IRS data for 2015 shows 207,861 tax filers — a good estimate of households — from other states lived in California the year before. We may miss those old relatives or friends, but they add up to only 1.48% of 14 million California filings. Only Michigan had a lower exits-to-population ratio.

California’s departure rate is far less than the national norm, which shows movers between states account for 2.14 percent of all U.S. filers. States that did a poor job at keeping its taxpayers included Utah (losing 2.33 percent of its filers); Arizona (2.72 percent); and Nevada (3.32 percent). These Western states, frequently cited as popular places for ex-Californians, have out-migration challenges, too.

The data also shows us the incomes that move with migration patterns.

To be sure, it’s eye-catching to see what departing Californians took with them: a combined taxable income of $16 billion in 2015. When you consider total incomes of Californian filers of $1.22 trillion, though, the outflow is only 1.3 percent of dollars earned – again, the second-best rate among the states (behind Michigan) and better than the national average of 1.8 percent.

Who’s leaving the state? IRS data suggest those with less wealth: the average income of movers was $77,000 per filing in 2015 vs. $87,000 statewide. But the tax data also shows California’s ability to retain population beats the national average at all six income levels broken out by the IRS — from those with little income to those making $250,000 or more.

Please note that one bit of homebuying data also shows Californians are pretty geographically stable.

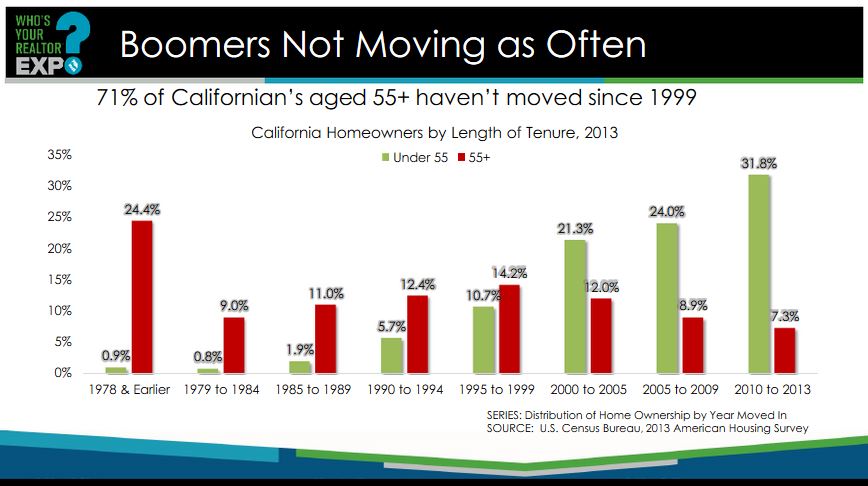

When Attom Data Solutions ranked five dozen major U.S. markets for how long recent home sellers had lived in their homes, five of the 12 markets with the greatest tenure were in California. Plus, the average length of ownership had grown by two years since 2012 to above 10 years in some cases.

In 2015, California gained 197,200 new filers with total incomes of $13.9 billion. But that’s tiny vs. the state’s huge population and economic heft. On a per-capita basis, only four states — Michigan, Ohio, Wisconsin and Illinois — fared worse in bringing in new taxpayers.

So, why have you heard tales of data showing large numbers of Californians leaving the state?

One often quoted metric is what is called the “net migration “– the difference between inbound and outbound.

Yes, population and tax data shows California with a negative net migration – more departures than arrivals. However, the seemingly large raw number of California exits is actually relatively modest when you compare it to the state’s scale as the nation’s most populous state.

IRS data shows 10,700 more departing Californian filers than arrivals, moving a “net” income of $2 billion out of state. Only three states — New York, Illinois and New Jersey — lost more “net” dollars in 2015. But when you see that net outflow in terms of California’s $1.11 trillion in taxable income, the state ranks 27th — middle of the pack – in proportional net income loss.

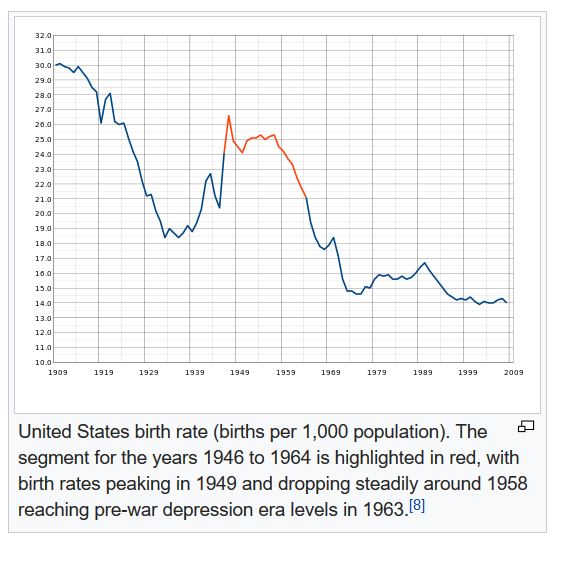

This guy saw it like I did – that there would be “the great senior sell-off”, but he had more concern that the millennials wouldn’t be there to pick up the pieces. He is back-pedaling now on when it will happen – and I think he is just guessing. It will happen when it happens, and each neighborhood will be affected differently. Hat tip daytrip!

It’s a dilemma that has preoccupied Arthur C. Nelson, a U of A professor who spoke with former CityLab staff writer Emily Badger in 2013 about what he dubbed “the great senior sell-off.” Nelson postulated that Boomers would soon be selling their homes in droves, but would be hard-pressed to find buyers—mainly because Millennials wouldn’t want to buy them.

Nelson pointed to the affordability issue as well as the fact that about a quarter of Millennials prefer urban housing, such as condos or townhouses, over the detached suburban homes that were the Boomers’ preferred habitat. Younger buyers, he said, will also be looking for starter homes—smaller than the big Colonials and split-levels that line America’s cul-de-sacs. “We can predict the next housing crash,” he said at the time. “That’ll be in about 2020.”

Four years later, Nelson tells CityLab that he believes the sell-off will still occur—but later, in the mid- to late 2020s.

This has to do with people deciding to defer selling their homes, hoping to get a better price later than settling for a lower price now. “Home values in much of the country are still less than those before the Great Recession of 2007 to 2009,” he says. Prior to the recession, the typical homeowner would sell a house about every six years. “It was like clockwork,” says Nelson. “This drove a lot of planning and development projections.”

“It’s not that Boomers are going to ‘age in place,’” says Nelson. “They’re going to be stuck in place, and they’re going to make the best of it.” Those who can afford it will remodel.

Though Jennifer Molinsky, a senior research associate at Harvard’s Joint Center for Housing Studies, agrees that exurbs and rural areas will likely be vulnerable to the Boomer/Millennial housing mismatch, she’s not as pessimistic about the sell-off as a whole.“The Baby Boomers are a large generation,” she says. “Nothing they do is going to happen en masse.” She also believes that the Boomers who don’t age in place will demand an increasing array of housing options that will help spread out sales over time, decreasing the likelihood of a sudden glut of housing.

Are you surrendered to buying a home from a down-sizing baby boomer? Be ready for some unique features! When this turns into a sticky substance, the new paint doesn’t stick well – I had a case where we were scraping the nicotine off the wall with razor blades!

Here are stats on the 99 NSDCC houses sold between March 1 and March 15th – these are the years when the sellers purchased the home they sold:

Year Purchased

12/12/15

3/19/16

6/18/16

12/13/16

4/3/17

0 – 2003

41%

42%

39%

57%

48%

2004 – 2008

23%

29%

24%

19%

15%

2009 – 2011

15%

11%

13%

6%

7%

2012 – 2016

18%

18%

19%

13%

25%

New Homes

2%

1%

5%

4%

4%

With roughly half the homes being owned by the sellers for at least 13-14 years, buyers can expect to do some repairs and improvements! It is interesting to note that 25% of the sellers were recent purchasers too. Is that a group consisting of divorces and move-up buyers?

More stats:

Other Categories

12/12/15

3/19/16

6/18/16

12/13/16

4/3/17

Number of Sales

125

114

144

112

99

Avg. $$/sf

$505/sf

$552/sf

$550/sf

$529/sf

$481/sf

Median SP

$1,080,000

$1,129,000

$1,291,500

$1,274,500

$1,110,000

Avg DOM

60

38

42

54

43

Sold in 0-10 Days

24%

32%

35%

28%

45%

Lost $$

11

3

7

7

0

DOM = 0

5

8

7

2

4

I don’t get worked up about the pricing stats – every group of houses is different, and the stats are going to bounce around. Other notable items:

Of the 99 sales, 24% of the buyers paid cash.

The median days-on-market was 13 days.

No sellers sold for less than they paid!

This is probably how the boomer liquidation will occur – one by one.

It’s happening throughout the county, and probably throughout the country. Everywhere you go, the majority of home sellers are older folks leaving the family homestead, or long-time residence.

Our local home prices have risen so quickly that it feels like we’re in ‘bubble’ conditions again – could the bubble burst this time?

The last two times the real estate bubble has popped, it was due to banks having to offload their foreclosed properties for whatever the market will bear. They flooded the market, and buyers – and prices – backed off.

But that has all changed now.

Look at the new devices being used to avoid a flood of desperate selling:

New accounting rules.

California Homeowners Bill of Rights

Reverse mortgages

The accounting rules were altered so banks could hold their REO properties longer, and the California Homeowners Bill of Rights has, in effect, stopped foreclosing. Lenders are now required to offer a loan modification to anyone in default, and only if the homeowner can’t or won’t qualify are they at risk of being foreclosed. With today’s higher rents, there isn’t much relief for those in default to give back their house and go lease one nearby. Besides, with our higher home values today, they can always sell before getting foreclosed.

Homeowners who need money can get a reverse mortgage too, as long as they haven’t been tapping into their equity already.

We end up with virtually no desperate sellers who need to dump on price. Someone who wants to cash out quickly can price their home at last year’s comps and look like a deal!

The game is rigged – the Banking Cartel won’t let the bubble pop again!

For the bubble to pop, we would need a dramatic shift in the supply and demand – either a flood of homes hit the market, and/or we run out of buyers.

I thought we’d be seeing more baby boomers unloading their homes due to downsizing or sickness, and while the market consists mainly of those listings, there aren’t enough of them to call it a flood – at least not yet. Because they are in quality locations, more kids are probably trying to buy out their siblings and take over their parents’ house, rather than sell it. They could be moving in with the folks too, rather than sending them to assisted living.

Could we run out of buyers? You would think there would be a price point where buyers can’t or won’t go any higher, but there seems to be a steady flow of people with more horsepower. We saw two weeks ago the prediction that the population of San Diego County is expected to grow by 700,000 people by 2050, which is over 21,000 per year – where are they going to live? Will they be rich? They will need to be!

There hasn’t been enough (has there been any?) sellers so desperate that they had to dump on price – instead, they just keep waiting. We would need more than a few price-dumpers to start a panic, which could cause the market to flood with supply and burst the bubble.

Some air might escape occasionally, but it is doubtful that a market change could occur without the government finding a way to save the bankers.

People like this guy think the conditions are ripe for a downturn. But if prices started falling, sellers are more likely to wait, than dump, which would cause our market to stagnate, rather than crash.

Are you getting the feeling that our low-inventory conditions are here to stay?

Our local Case-Shiller Index has risen 59% since April, 2009, and fewer people are selling? Instead, they appear to be riding into the sunset.

Consider these boomer stats from wiki:

60% lost value in investments because of the economic crisis

42% are delaying retirement

25% claim they will never retire (currently still working)

For those who moved up a couple of times, their current house is the best they’ve done, and is good enough to last them. There isn’t a compelling reason for boomers to move if they bought low, and the house is paid off or refinanced into an ultra-low rate.

Baby boomers are currently 53 to 71 years old, which should mean they could move if needed. They just don’t want to.

If things got tough, it’s more likely they would share with the kids. Either have a kid move in and help with care-giving, or go live with a child.

My mom is moving in with us this month.

My dad died in 2010, we sold their house, and mom has been on the move ever since. She tried living on her own, but that was boring, and then recently she lived with my little brother, which everyone will tell you is no picnic. She lasted 14 months with him, which is more than I would have!

But even with a life-changing event, there’s no change to real estate. Mom’s house was sold long ago, and we don’t need to move to accommodate her.

We’ll all just get along instead!

As baby boomers keep aging, many, if not most, will find a way to make do with what they have, rather than move. Upon their demise, one of the kids are more likely than ever to inhabit, rather than sell.

The rapid ascent of prices haven’t helped either – it’s probably one of the main reasons don’t want to move. It’s too expensive, compared to what they have, and they’d rather find a way to stay put.

The cheaply constructed mansions of old are plummeting in value as homebuyers are more discerning.

In an article in August 2016, Bloomberg cited data from the real-estate site Trulia that showed that the premiums paid for McMansions have declined significantly in 85 of the country’s 100 biggest cities.

For the study, Trulia defined a McMansion as a home that was built between 2001 and 2007 and that had between 3,000 and 5,000 square feet of space.

In one example, in Fort Lauderdale, Florida, the extra money that buyers were expected to be willing to pay to own a McMansion fell by 84% from 2012 to 2016. In that same city in 2012, a typical McMansion would be valued at $477,000, about 274% more than the area’s other homes. Today, a McMansion would be valued at $611,000, or 190% above the rest of the market.

Experts told Business Insider’s Madeline Stone that the youngest generations of homebuyers tend to value efficiency more than ever before and feel that McMansions are impractical and wasteful.