Thanks to their sheer numbers, the baby boomers have shaped society, driving social change and the economic expansion since the 1970s. But now they’re influencing society in a new way — by holding on to their homes.

The oldest baby boomers are now in their early 70s, an age that in previous generations signaled a desire to downsize into condos and apartments. But economists are finding that boomers aren’t yet downsizing, at least not in the numbers that some of them had predicted.

That may be adding to the ongoing inventory crunch facing homebuyers, said Zillow senior economist Aaron Terrazas. Boomers are healthier and working longer than previous generations, which means they aren’t yet ready to sell their homes and strike out for retirement developments. And some may not want to sell their homes because they then must jump into the homebuyers’ market, which is suffering from low inventory and high prices.

“Several years ago there was an expectation that as baby boomers move into retirement, there wold be a surge of homes hitting the market,” Terrazas said. “That really hasn’t materialized.”

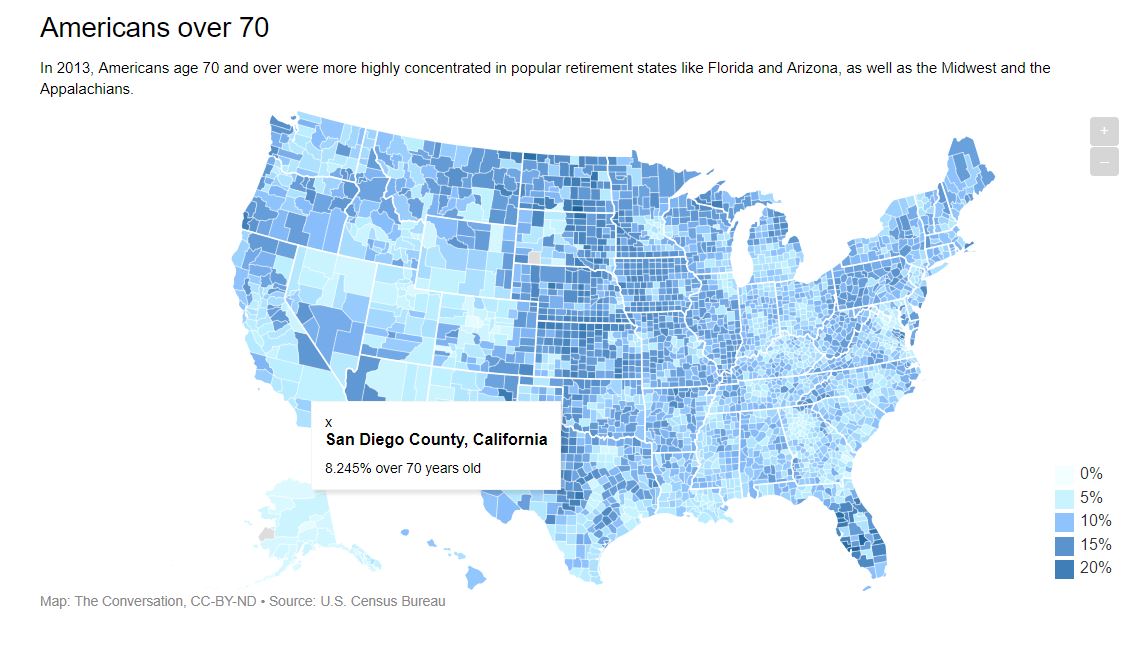

Five years ago, San Diego County had the second-highest number of people over 70 years old in Southern California (Riverside is higher), but other areas have many more. There are counties in Florida with over 25%!

Maybe those boomer liquidations might occur later than expected?

Want to hurry up with that empty nest? From cnbc.com:

A New York state judge has backed a couple’s battle to kick their 30-year-old son out of their home because he has not contributed toward household expenses or helped with chores and they wanted him to get a job.

New York State Supreme Court Judge Donald Greenwood on Tuesday ordered Michael Rotondo to leave his parents’ home in the town of Camillus, about 200 miles northwest of New York City, according to Anthony Adorante, an attorney for the parents, Mark and Christina Rotondo.

Adorante declined further comment on the decision, which ended a four-month family battle.

In court documents, Michael Rotondo referred to a “common law requirement of six-month notice to quit” before a tenant may be removed.

“I just wanted a reasonable amount of time to vacate, with consideration to the fact that I was not really prepared to support myself at the time where I was served these notices,” the younger Rotondo told local CBS television affiliate WSTM.

Another study that shows lower-income people leaving California, and rich people moving in. But what’s not examined is whether those leaving were long-time homeowners who sold their home and took a truckload of money with them to Texas:

Will the day come when boomers need to sell their house to survive? The reverse mortgages have offered a solution for some, but they are expensive and loan limits have been cut back recently. The general real estate market may not feel the impact of boomers running out of money, but you could see flare-ups of more inventory in older areas.

The grim outlook for many Americans approaching retirement age has some new stark statistics: One-third of respondents in a recent survey said they’d saved less than $5,000 for retirement.

Among baby boomers, one third said they had $25,000 or less in retirement cash available, according to a new data release from life insurance provider Northwestern Mutual.

Looking at the wider pool of Americans in general, 21% reported that they had zero retirement savings, while exactly three quarters agreed that Social Security is unlikely to exist in its current form when they eventually retire. And just about half said they’d done nothing at all to prepare for a future in which they outlived their retirement savings — despite the fact that two-thirds said that scenario was at least somewhat likely.

“As financial implications of retirement become increasingly complex, inertia just isn’t an option,” Northwestern Mutual vice president of planning Rebekah Barsch said in a statement announcing the results. “The good news is that it’s rarely too late to start.”

The survey also revealed that many Americans have resigned themselves to the idea of working longer before retiring, a strategy that’s increasingly preached even by financial planners. Nearly 40% of respondents in the Northwestern Mutual poll said they would work until at least age 70, more than the 33% who said they were targeting a retirement date sometime between 65 and 69.

In addition, the desire for more disposable income slightly outweighed professional satisfaction when respondents were asked why they planned to work past 65. That’s a shift from 2015, when the same study determined that 66% of Americans simply wanted to continue working for the fulfillment of it — as opposed to 60% who cited income as a concern.

“Continuing to work later in life should be a personal choice and not a mandatory requirement for survival,” Barsch said. “Proactive financial planning can be the difference between a desired and a default retirement lifestyle.”

Just talking about the GOP tax changes could slow down the market. Because the N.A.R. and others are suggesting publicly that home values could drop 5% to 10%, won’t potential home buyers wait to see if it happens?

The demand will still be there; it will just be more picky than it is today.

The move-up market is where we could see real impact from the proposed tax changes. If potential move-uppers don’t move, they would keep their mortgage-interest deduction and lower property taxes. If they do move and get a loan over $500,000, they’ll enjoy paying on a new mortgage for 30 years with no MID, and pay higher property taxes.

They won’t calculate the exact cost of losing the MID (it’s not that much) – and instead, it will be the last straw and they will just quit thinking about moving because they’re disgusted with politicians.

We will also lose a few who need to stick around longer to qualify for the tax-free gain on the sale of their house, due to the change of having to own/occupy the house for five out of the last eight years to qualify.

End result: Fewer people willing to move up, which would have a significant impact on the higher end market. True, the move-up buyers won’t be listing their lower-priced house for sale either, which would create a net-zero change, and potentially make the inventory tighter, which would be better for the remaining sellers.

But there hasn’t been a shortage of homes for sale listed over $1,000,000 (there are 1,395 homes for sale today in San Diego County priced over $1,000,000, and 327 sold in October).

Higher-end sellers will have to wait even longer for the trickle of buyers to reach them. Plus, if a neighboring seller or two dumps on price to unload theirs, the lower comps could add another six months to the selling timeline, or longer. The sellers who claim to be in no rush will be tested!

The environment will be compounded by the lack of experience in dealing with this type of market by everyone involved. For the last seven years, if you wanted to buy a house, you had to pay the sellers’ price….or more. Will that continue? Yes, for those selling a perfect house at the perfect price. But it will be too easy for buyers to pass on the clunkers or OPTs.

S-t-a-g-n-a-n-t C-i-t-y.

The lower end should stay red hot, but it won’t be trickling up as much.

And that’s not considering the possibilities of higher interest rates, earthquake or other natural disaster, nuclear war, or recession!

It’s all about millennials these days. Everything seems to center around these special snowflakes. But what about the original “me” generation? We’re talking about baby boomers, of course. What do these roughly 76 million Americans want when it comes to housing?

Well, they want multicar garages, for one thing. According to a recent survey by national homebuilder PulteGroup, they were the top feature boomers were looking for in a new home, followed by open decks or patios; eat-in kitchens; and a private yard.

About 38% of boomers plan to buy a home within the next three years, according to the report. About 11% expect to purchase a residence within the year.

The survey was of 1,043 folks between the ages of 50 and 65 who plan to buy a home in the next decade.

“Retirement marks a new phase in a baby boomer’s life, and it only seems natural to relocate or move to a new home when transitioning away from their primary career, or from the day-to-day rearing of school-aged children,” Jay Mason, vice president of market intelligence for PulteGroup, said in a statement. “It’s not surprising that the 55+ buyer wants a variety of options and choices in their homes.”

According to the survey, 39% of respondents said the main reason they’re moving is because they want to retire, 33% want to downsize, and 30% want to move to a more desirable location.

“One thing we know about boomers is they are not done yet,” says Amy Lynch, president of Generational Edge, a Nashville, TN–based company that consults with companies on generational differences in employees. “As a group, they are starting encore careers and also going back to school. And they often move to be near their millennial kids, who are having kids.” They also start new families of their own, through divorce or remarriage.

All of these situations may require a move. About 26% of boomers plan to stay in their current cities, but just move to a different home, while 34% want to remain in the state, but in a different city or town. Also, 38% hope to cross state lines.

Their top retirement destination? You guessed it: Florida. It seems you just can’t beat all of that year-round sunshine. The state was followed by fellow warm-weather states Arizona, North Carolina, and South Carolina. The cost of living is lower in these states than on the pricier West Coast or in the Northeast.

About 82% of boomers wanted to be someplace affordable, and 74% want to be close to their preferred health care programs.

But boomers don’t want to just pack up and leave their grandchildren. Being close to kids was their top consideration when choosing a new community. They also want to be near the water and park or other green space.

“We are in a period in this country where family life and family connections are very strong,” says Lynch. “There’s a lot of regret among boomers because they worked so many long hours when their kids were young. With grandkids, there’s a chance to make up for that.”

Jeff Swaney is worried about selling his 5,600-square-foot home one day.

In his neighborhood south of Atlanta, demand and prices for large ranch houses like his have declined over the last decade, as more young professionals move to smaller abodes in hipper areas. He doesn’t expect that to change anytime soon.

The 51-year-old real estate investor and owner of Swaney Consulting Group has personal reasons to hold on, at least for now. He may eventually move to a condo at the beach, but wants his future grandchildren to enjoy his pool, yard and basement. For these amenities, he spends about $18,000 annually in lawn maintenance, taxes, insurance and utilities alone.

The housing market, on the rebound since the Great Recession, is increasingly being driven by millennials and first-time homebuyers who “are hungry for starter homes and efficient layouts,” said Javier Vivas, manager of economic research for realtor.com.

The trend may leave some older homeowners in a lurch if they want to retire, downsize and cash in their nest egg.

Large single family homes — defined as the largest 25 percent of all listings on realtor.com and about 2,900 square feet to 4,000 square feet — receive 12 percent to 45 percent less views on realtor.com than the typical home in each market.

This year so far, large, single family homes are selling up to 73 percent (or 50 days) slower on average than the typical home in each market.

The often hefty price tags for bigger homes contribute to their lengthier sale times because there is a smaller pool of buyers who can afford them, said Artur Miller, founder and CEO of Miami-based AMLUXE Realty.

Even Swaney, whose 1994 home appraised for $350,000, thinks he may have a tough time selling.

“The McMansions that soon-to-retire people purchased in the 80s and 90s are a very difficult sell right now,” said Melissa Rubenstein, a former real estate attorney who now sells luxury properties with Re/Max HomeTowne Realty in Bergen County, New Jersey. Many are outdated and may not include a first floor bedroom and bath suite for aging in place or in-laws.

Listings of large homes are also up two percent from last year, suggesting owners are dumping them faster, while listings of all homes are down 10 percent from last year, according to the realtor.com data.

“We’re finding these homes are an albatross for clients,” said Michael E. Chadwick, a financial planner and owner of Chadwick Financial Advisors in Unionville, Connecticut.

“We’ve got several right now who have been trying to sell them and move south, and they’ve cut the asking price by over 30 percent each and they’re still not going anywhere fast,” he said.

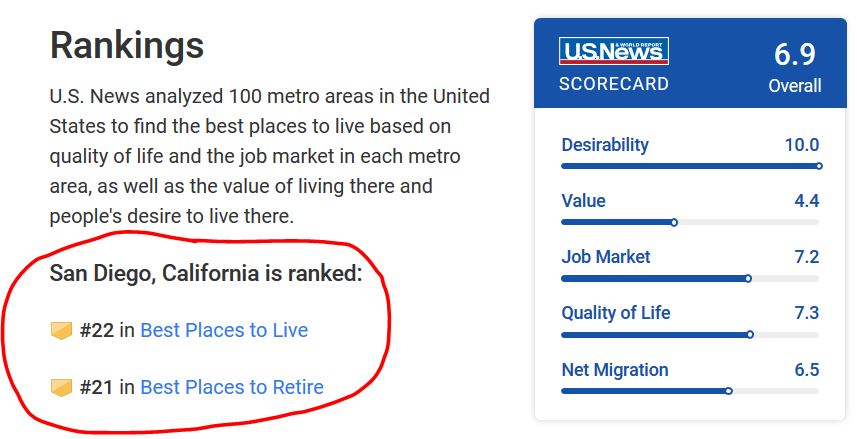

The 2018 rankings of the Best Places to Retire are out!

San Diego is ahead of other more-typical retirement towns like Charlotte, Phoenix, Las Vegas, and Denver, and the only California city in the Top 50. But there are twenty places ranked above us, so if you’re thinking of leaving us, here’s a guide: