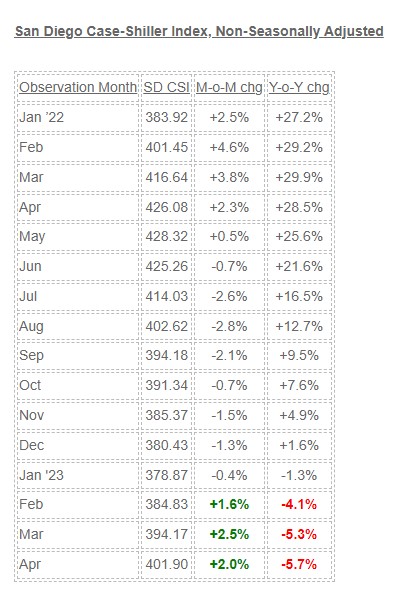

Even though we’ve had healthy gains in 2023, the YoY declines makes it look like we’re going backwards because the index was rising so quickly last year. Hard to imagine any more MoM gains of 3.8% or 4.6%!

April’s index is about the same as it was in February AND August, 2022.

Going forward, it should settle in to a range of 390-420 for the next couple of years.

However, the view from the ivory tower is that we’ve survived the downturn and we’re fine now. Because the Case-Shiller Index is so dated, he already knows that the next 2-3 months will be positive:

“If I were trying to make a case that the decline in home prices that began in June 2022 had definitively ended in January 2023, April’s data would bolster my argument. Whether we see further support for that view in coming months will depend on the how well the market navigates the challenges posed by current mortgage rates and the continuing possibility of economic weakness.”

My guess is that the second half of 2023 will go back to Plateau City, like it did in 2019:

Powell’s goal was to crush the real estate market…..

In June 2022, Powell told reporters that spiked mortgage rates would help to “reset” the U.S. housing market, and that “we need to get back to a place where supply and demand are back together and where inflation is down low again, and mortgage rates are low again.”

Then in September 2022, Powell told reporters that we had officially entered into a “difficult correction” that would restore “balance” to the housing market. At the end of November 2022, Powell went a step further, and said a “housing bubble” had formed during the Pandemic Housing Boom.

Last week, Powell said, “The housing market is bottoming and may already be improving.” He made the comment after the central bank kept benchmark rates steady but indicated more hikes may be needed later this year.

“Activity in the housing sector remains weak, largely reflecting higher mortgage rates,” Powell told reporters after the rate announcement. “Certainly, housing is very interest rate-sensitive, and it’s the first place, really, or one of the first places, that’s either helped by lower rates or is held back by higher rates. And we certainly saw that over the course of the last year. We now see housing putting in a bottom and maybe moving up a little bit. We’re watching that situation carefully.”

In his prepared statement yesterday, he said, “Although growth in consumer spending has picked up this year, activity in the housing sector remains weak, largely reflecting higher mortgage rates.”

Then he said,“We think housing inflation will be coming down significantly over the course of the rest of this year and next year. Consumer inflation has eased since last summer due mainly to falling energy and core good prices. In contrast, rents and other housing inflation has been moving higher.”

What he doesn’t see…..

Powell’s comments get turned into headlines, like this:

Potential home sellers take one glance and – even though they aren’t quite sure what he means – they decide the market is no good and that it’s smarter for them to wait for better times. It would take a flood of supply to effectively reset the real estate market, yet his policy is doing the opposite. Plus, his higher rates are pricing out the marginal buyers (the regular people), which creates less competition for those who can withstand higher rates – the affluent buyers.

The end result is affluent people chasing the few sellers who really need to move – just the type of buyer who can, and will, pay more to get what they want now….which will help to keep prices elevated.

What’s likely to happen:

The off-season will commence shortly and there will be fewer sales than ever, with an occasional deal here and there. The trendline will look softer than during the selling season, which will cause Powell and others to abandon the bottom talk and instead declare that their ‘housing inflation’ – code for rising prices – is coming down. Everyone will take it as a sign that the recession is finally here!

Then the 2024 selling season will get rolling in February, confounding the experts even more.

It might take a couple more years before they start believing that home sales are seasonal – if they ever do.

Here are expert opinions on the market. I disagree with all of them:

The year started out with signs showing that the Federal Reserve’s inflation-fighting tactic was effective in cooling down the hot pandemic housing market.

For the first time in 11 years, home prices dropped year-over-year in February as mortgage rates more than doubled following the Fed’s consecutive interest rate hikes, curbing affordability.

However, the median price of a home increased month-over-month for the second consecutive month in March. The median home price is projected to increase for a third month in a row in April to $393,300, which is 2% lower than the previous April’s median price of $401,700, according to data released in May by the National Association of Realtors (NAR).

One big factor behind the strengthening home prices and the decrease in sales volume — down 23% in April from a year ago — is the lack of housing inventory.

“Home sales are bouncing back and forth but remain above recent cyclical lows,” says NAR Chief Economist Lawrence Yun. “The combination of job gains, limited inventory and fluctuating mortgage rates over the last several months have created an environment of push-pull housing demand.”

Where are home prices headed?

Generally speaking, high mortgage rates should prompt house prices to trend downward.

“Yet, housing supply remains so restricted, that any uptick in demand will put upward pressure on prices,” wrote First American Chief economist Mark Fleming in a blogpost. “This is the dynamic that played out in March, as the spring home-buying season ushered in more demand for homes, while insufficient supply prompted buyers to compete and bid up prices.”

No return to typical seasonality in the market

There will be a lot of uncertainty in the economy over the next few months and prospective home buyers are going to be more opportunistic, as opposed to following traditional seasonal market trends, says Bright MLS Chief Economist, Lisa Sturtevant.

“There will continue to be volatility in mortgage rates as we wait to see what the Fed will do at its upcoming meetings and as we watch economic data roll in over the summer,” says Sturtevant. “Prospective buyers are going to be watching rates closely, and many will try to make an offer on a home when they see rates dip. As a result, we should expect less seasonality this year than we had prior to the pandemic.”

More sellers returning to the market

While inventory will remain low this year, we should expect to see more sellers who had been on the sidelines list their home for sale this summer and into the fall, says Sturtevant.

Many existing homeowners have been “locked in” with super low mortgage rates, which has discouraged discretionary moves.

“However, some people have to move, and others will decide to move for a bigger or smaller home, or to change jobs or neighborhoods, despite rates remaining elevated,” says Sturtevant.

The uptick in new home construction has provided more opportunities for move-up buyers who may have been staying in place because they did not have anywhere to move to.

“One thing that could shut down new listings is if we see a sharp spike in mortgage rates to 8 or 9%, a situation that is still unlikely but not out of the realm of possibilities,” she says.

New home construction

Instability of regional banks is a concern for builder and land developer financing going forward, says Robert Dietz, chief economist for the National Association of Home Builders.

Lending conditions for builders have tightened, and the interest rate for development and construction loans is now well above 10%, which threatens housing supply.

Single-family spec home building loans had an effective rate of 13% in the first quarter of 2023 compared to 9% in the first quarter of 2018.

“Our expectation is that the rate of these loans will move lower as the Fed cuts the federal funds rate, but our forecast is that will not happen until later in 2024,” Dietz told USA TODAY. “As a result, land development would be suppressed, and we risk loaning low on lots during a home building rebound in 2024. Lot development can take three years in a typical market.”

Zillow, Goldman Sachs, and every economist thought the 2023 market would be all negative.

But now….

Goldman Sachs originally forecasted home prices to fall by double digits. However, they have released a report titled – “As interest rates climb, the global housing market is surprisingly stable”. In it, they stated: “House prices [are] leveling out more quickly and at a higher level than would normally be expected given the rapid rise in mortgage rates. Home prices are defying expectations and RISING in major economies such as the U.S., Australia and Canada.”

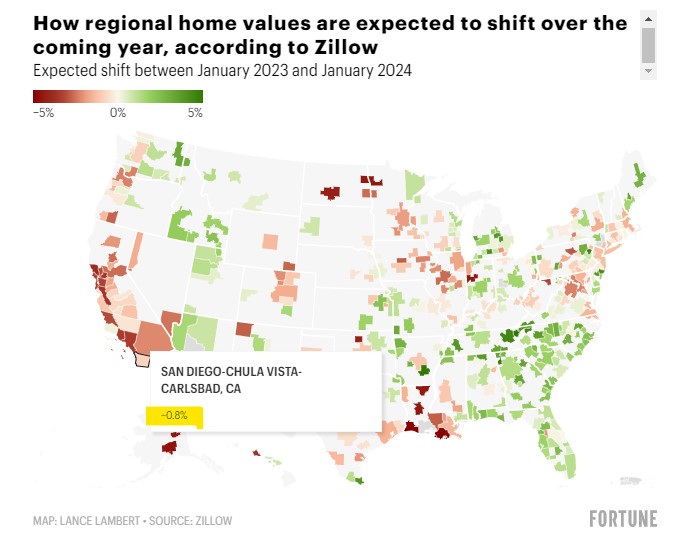

Now Zillow is forecasting 3%-ish appreciation here for the next year – which sounds like the old normal:

We know that the perception is more important than the reality, especially for potential sellers. If they see some media coverage that is slightly positive, maybe more will come to market this year, instead of waiting for some vague unknown day in the future when the market gets ‘better’.

An excerpt:

Zillow economists now believe they’re done issuing downward revisions. In fact, they think the national housing market correction could be nearing its bottom.

Heading forward, Zillow economists expect U.S. home values as tracked by the Zillow Home Value Index (ZHVI) to rise 0.5% between January 2023 and January 2024.

Among the 400 largest housing markets tracked by Zillow, the company expects 238 markets to see positive home price growth between January 2023 and January 2024, while it expects six markets to remain flat and 156 markets to notch a home price decline over the next 12 months. Simply put: Zillow expects only 39% of major markets to post a home price decline over the coming year.

Just what we need – a new model that comes to the same wrong conclusion……

A new model of forecasting home prices based on consumer demand predicts that prices for housing will decrease by 5% nationally and 12% in San Diego County by the end of this year. The model, which highlights online search activity, was recently published in a new study from the University of California San Diego’s Rady School of Management.

The model’s predictions have a proven accuracy rate of up to 70% and are unique to other price predictors — such as Zillow, Goldman Sachs and Redfin —because those consider a variety of factors like interest rates, wage growth, unemployment and housing supply. Whereas the housing search index created by Allan Timmermann of the Rady School and collaborators at Arhus University in Denmark, focuses on consumer demand by tracking the rate at which prospective buyers use the internet to search for homes.

“It is one of the purest measures of potential demand that you can get because the first thing you do when you’re looking for a house or interested in buying a house, is to go to the internet and look at what is available,” said Timmermann, a distinguished professor of finance at the Rady School. “Those in the market for a home leave a big footprint with their online search activity because of the time it takes – often several months – to find something that is the right fit.”

Cities like San Diego have housing prices dropping more than the national average because it’s where the market overheated the most during the pandemic, Timmermann said.

I was going to ignore one more forecast by a financial services company (what do they know about selling homes?), but this is from the squid, plus Derek mentioned it in the comment section.

None of these forecasts provide any evidence or reasons for their conclusions. They are just guessing, apparently, and merely searching for more eyeballs.

They are probably transfixed on the median sales price, one of the worst tools available.

San Diego County Detached and Attached Homes, Median Sales Price

April: $871,000

December: $757,250

Diff: -13%

There you go – the county’s median sales price has dropped 13% so far.

Do you see that much in the market?

I’ll give you a better example:

NSDCC Detached-Homes, Median Sales Price

March: $2,625,000

December: $1,895,000

Diff: -28%

Do you see houses between La Jolla and Carlsbad selling for 28% less than they did in March? Me neither. NSDCC sales dropped in half (207 vs 101), and the homes that are selling are smaller (average square footage is -13%) and more inferior which explains why the median sales price should be dropping. But nobody mentions the additional variables.

We are being dumbed down by the squid, and others.

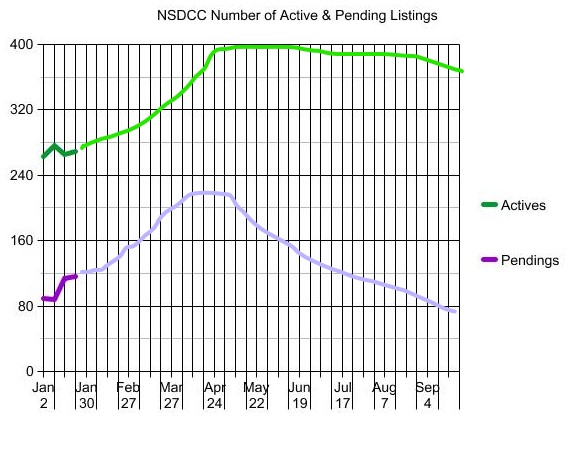

The graph above is boring this time of year, so I added my predictions in the lighter colors. I’m figuring that the Fed will be relentless and the higher rates in the second half of the year will cause the pricing gap between sellers and buyers to be tougher to bridge.

It’s because there will be some decent sales in April and May that keep sellers optimistic that the perfect buyers are coming tomorrow….or next week….or well, heck, let’s just wait until 2024.

Here is the graph from last year:

For our contest participants, there are 120 new listings this month – and we’ve had 36 new listings every week for the last three weeks. It means our contest should wind up around 170-180 listings?

My guess was that the NSDCC annual sales would be +5%, and pricing +15% in 2022.

It was a tough year for prognostications!

NSDCC YoY Statistics

Year

Annual Sales

Median SP

Median SF

December Sales

Median SP

Median SF

2021

3,184

$1,900,000

2,852sf

183

$2,165,000

2,804sf

2022

1,937

$2,300,000

2,722sf

100

$1,892,500

2,596sf

Diff

-39%

+21%

-5%

-45%

-13%

-7%

The smaller square footage takes a little bit of the sting out of it, but anyone who guessed right about the 2022 statistics was just plain lucky.

I was close on the annual price increase, but it doesn’t mean much after considering what the median sales price was last month – which is now back to the mid-2021 range.

I would have been way wrong on the sales prediction, even if the frenzy would have continued. The sales between January and May – when the frenzy was still raging – were down 28% YoY. It shows how insane the market was in 2021, and how unlikely it will be that we will ever seen anything like it again.

But have you seen ANY superior homes selling for a discount yet? Me neither, and one reason is because there are so few for sale. Once we wade into the spring selling season, we’re going to see how the market has divided in two segments – superior vs. inferior properties – and how the affluent buyers will pay the price for the top-quality homes.

The big question is what the realtors will do.

Any agent can sell a creampuff – the homes that are well-located, upgraded, tuned-up, easy-to-show, and priced attractively. But how many properties are in that category? Maybe 5% to 10% max? The overall market, and the changes in these dumb statistics that everyone thinks mean something, will be made in the trenches by the listing agents.

Will they game up and provide excellent salesmanship that keeps homes selling for about the same prices? Or will they be like prancing bullfighters and just get out of the way as the buyers come barreling through with their demands for discounts?

When we look at these stats next year, we will know the answer.