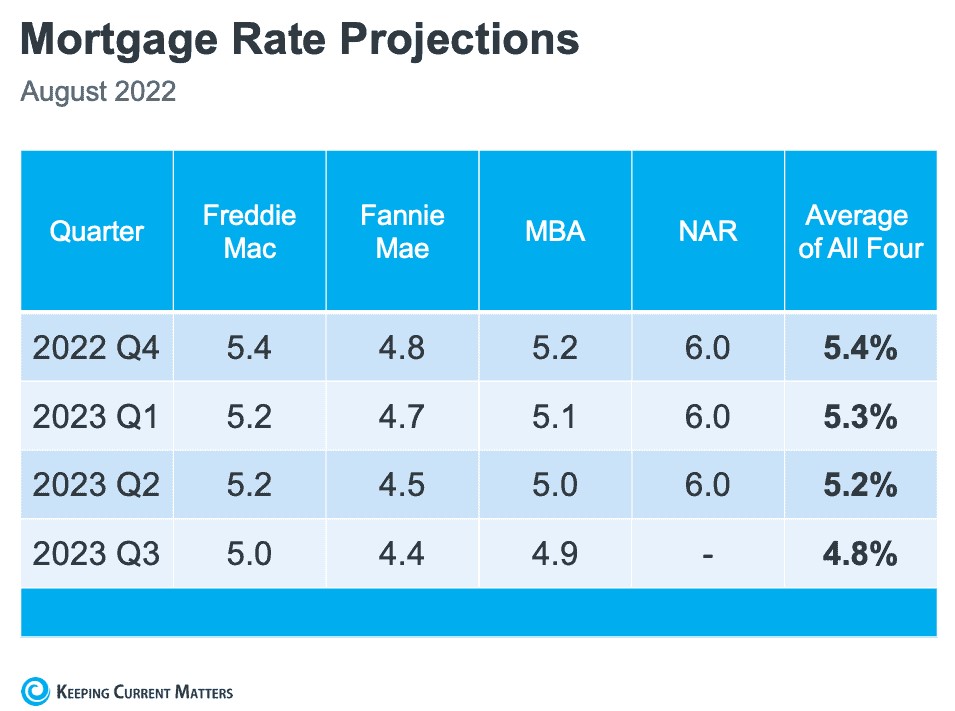

If rates would stay around 5% over the next four quarters, the market should digest it and get comfortable with the new era. But how reliable are these experts? After all, they are the mortgage business – shouldn’t their forecasts be pretty close? Well, hmm, no:

Zillow has recalibrated and is predicting a fairly flat 12 months ahead.

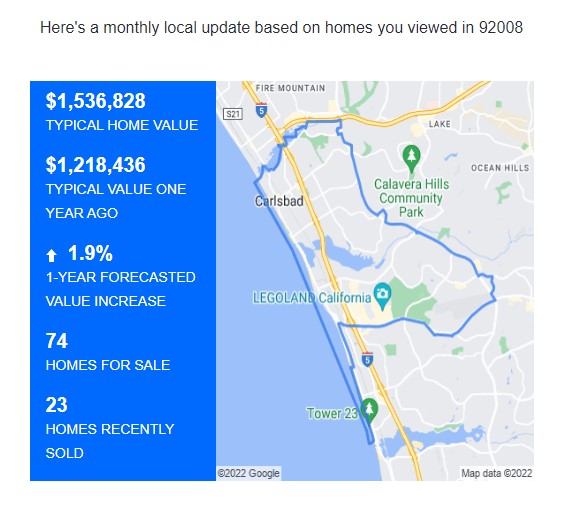

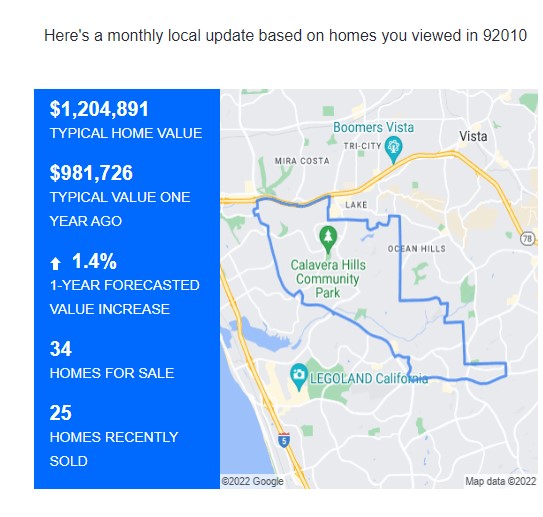

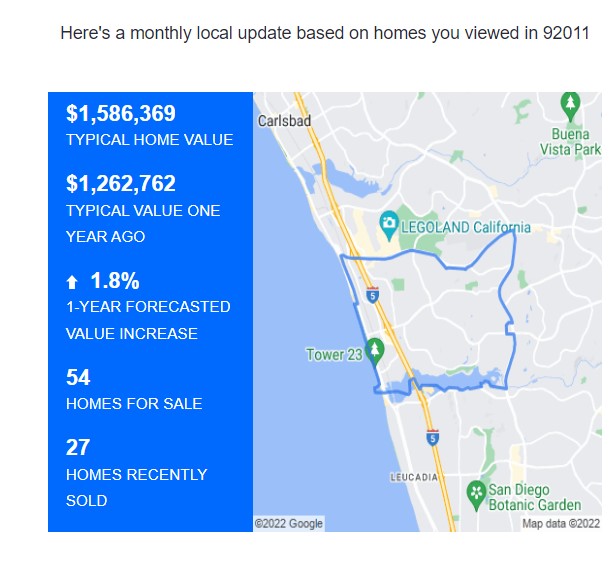

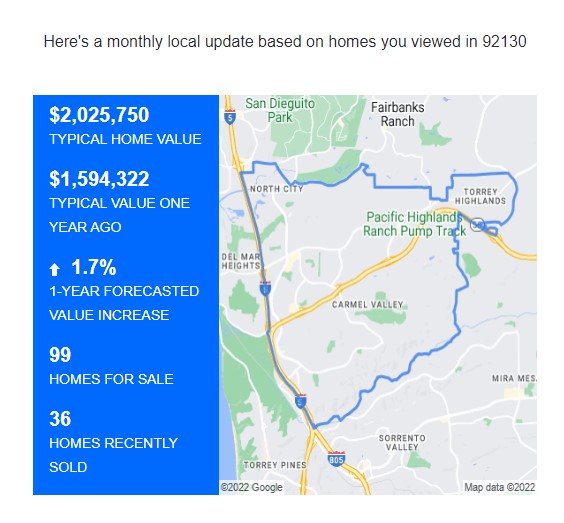

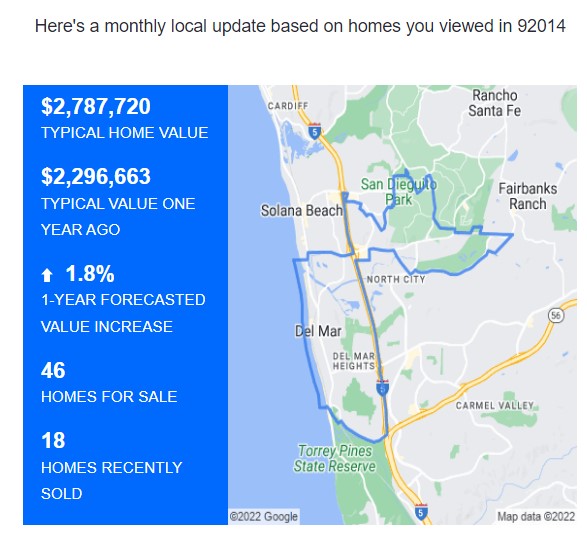

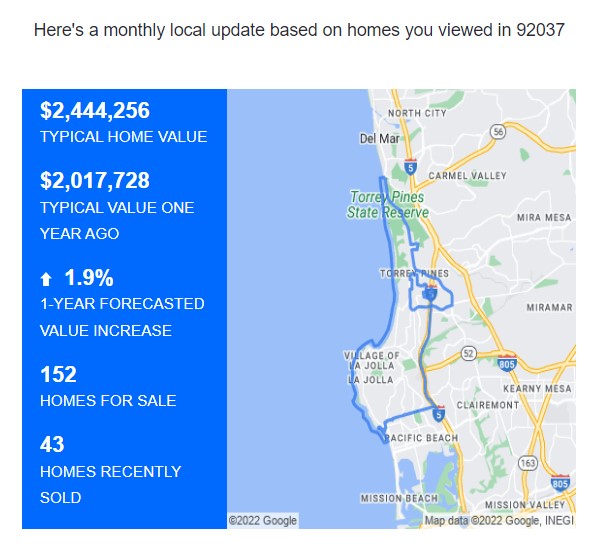

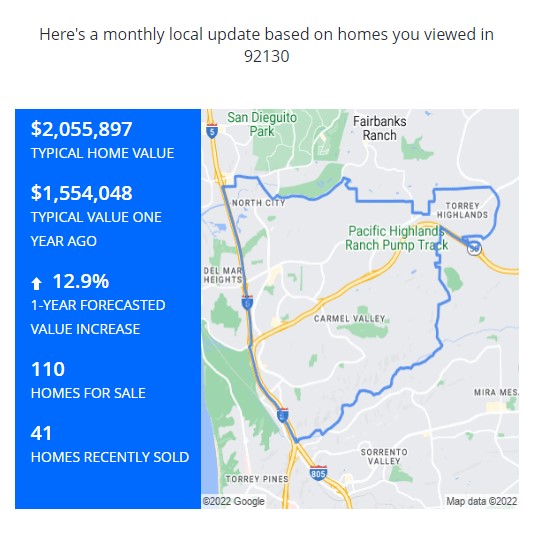

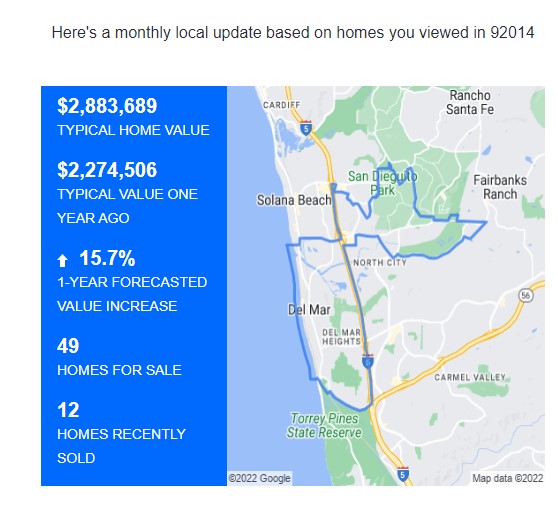

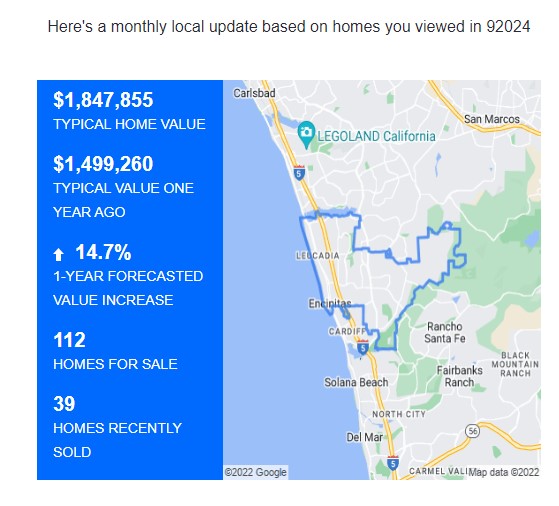

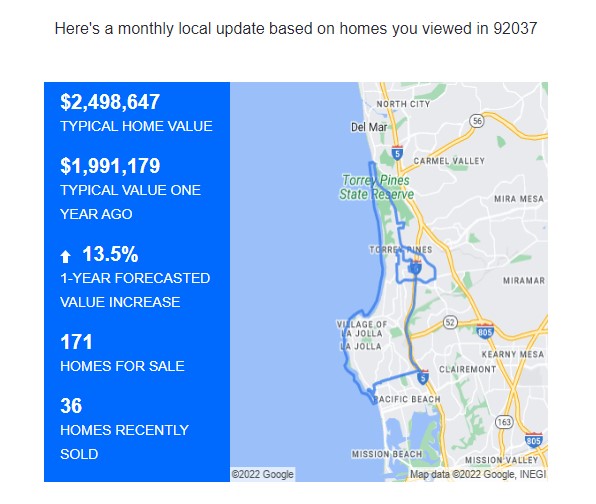

Here are the zip codes I’ve received so far, all ranging between +1.5% and 1.9% appreciation over the next 12 months – the rest of the local zip codes should be similar:

Yesterday’s Case-Shiller Index for San Diego was 425.26, which is 11% higher than it was in January.

But check how the trend increased between January and now.

Prices rose as fast as ever in early 2021 (yellow above). If they would have mellowed out along my red line, then we would have experienced slightly-increasing prices for the last year. But noooo! Instead, the early-2022 buyers – egged on by their realtors – insisted upon paying ridiculous amounts over the list price to win a house. Hopefully that practice is done.

The only reason the June reading was 11% higher than January was because it came down a bit. The San Diego Case-Shiller Index rose 11.2% between January and April, 2022, which was an annual clip of 33.6% – which nobody would have believed was sustainable after rising 43% since the pandemic started.

If the SD Case-Shiller just goes back to where it started in January, it will be a 10% drop from today, which will sound like a disaster. But the annual appreciation will be zero, which is not only reasonable, but sustainable for a while.

Is anyone going to mind if we start 2023 where we started 2022, price-wise? If mortgage rates can stay in the 5s, and hopefully the low-5s, we should be fine!

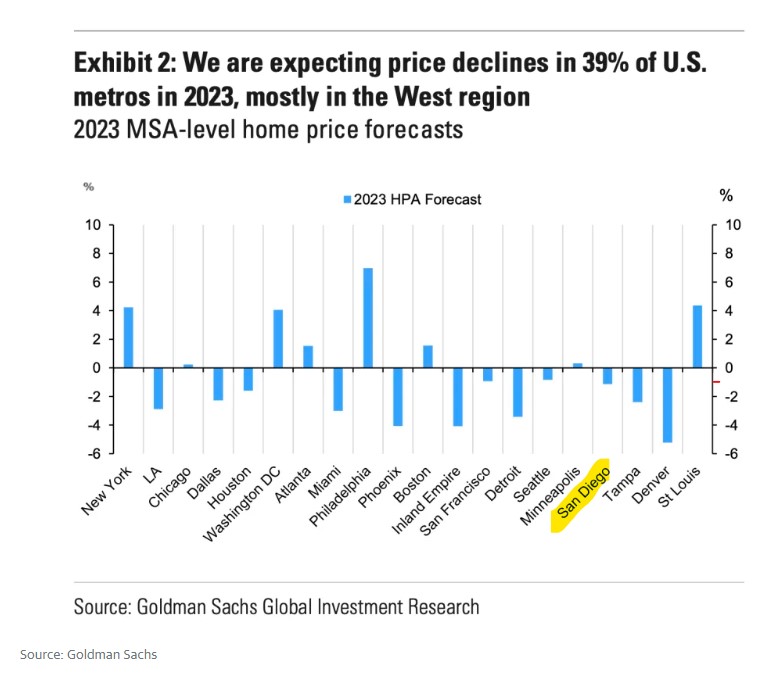

These guys are among the most negative in the business, so if they have San Diego County home prices changing –3.65% between now and the end of 2023, and then -2.9% by the end of 2024, then prices in the better areas will be positive.

The most likely to happen is that we’ll see a few wild sales at the extreme ends, and those will get the headlines. The rest will be +/-5% of the comps. Most will just fumble along – just like during the frenzy – with little or no quality data or advice.

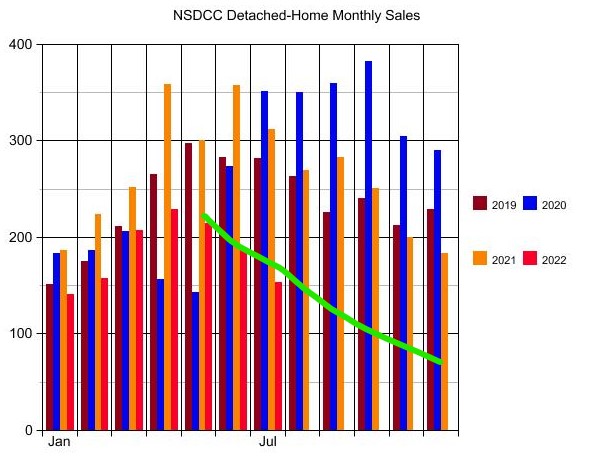

I think we can say that summer is over, and the off-season is here.

How will the rest of 2022 play out, and what will be the effect on the 2023 Selling Season?

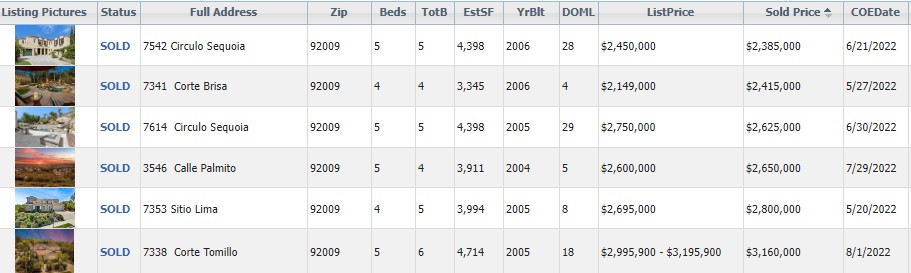

We know that the local NSDCC sales counts will be low for the rest of 2022. Last year we had 136 closings between August 1-15, and this year we’ve had 65. If we keep having about half of the 2021 sales, then our total sales between August and December will be 594, or an average of 119 per month!

It could look something like this green line:

We will probably have fewer listings than ever in 2H22, but those sellers should be motivated to sell. If they didn’t need to sell, wouldn’t they be tempted to just wait until spring to go on the open market?

We know that every seller has a load of equity, so if they have to lower their price to sell, they could. But will they? We can speculate that if they only had to lower their price by 5%, then they would make the deal. But going lower than 5% off is where the trouble starts – and the seller’s ego gets a vote.

If sellers continue to hold out on price, and sales follow the green line, it will look like a hard landing – and the 2023 selling season could end up being a dud. It would definitely get off to a slower start, and could sputter through the selling season if the inventory is lackluster and priced at retail, or retail-plus.

How likely is that? Very!

The second-half sellers of 2022 are going to determine our fate for the 2023 Selling Season. Expect next year’s market to be somewhere in the Sputter-to-Frenzy range, guaranteed!

But if you are a buyer, what are you going to do? Wait until 2024?

Let’s re-visit this in January. If sales beat the Green Line, then a more active market in spring is likely!

The latest Zillow 1-Year Forecasted Values are still expecting a fairly strong appreciation rate over the next year – these estimates are the same or higher than last month! I can see a path to how this could happen.

The Spring Selling Season gets frenzied up for 3-4 months where buyers and sellers all jump in at the same time, and then the market goes flat for the rest of the year…..kinda like this year!

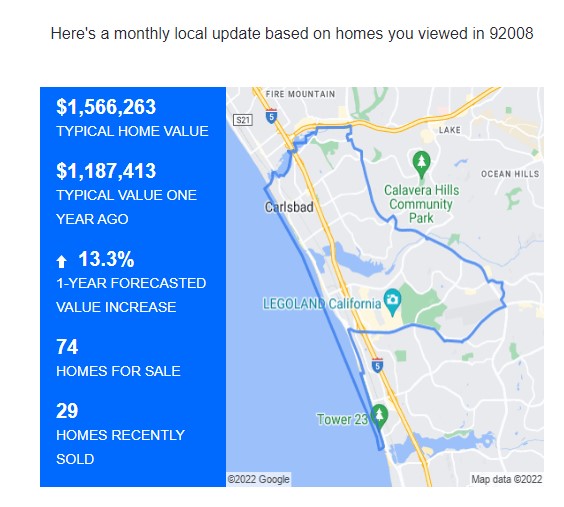

NW Carlsbad, 92008:

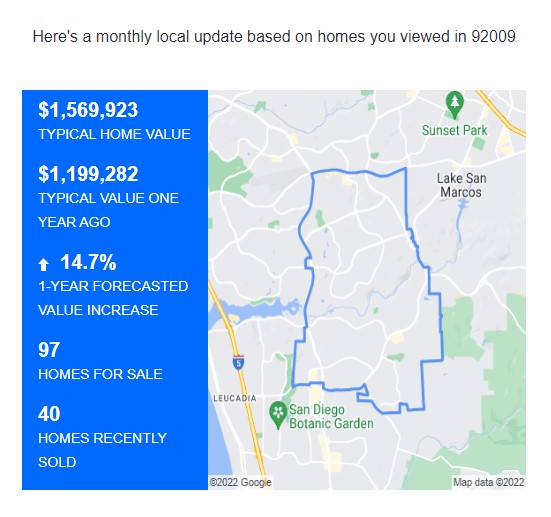

SE Carlsbad, 92009:

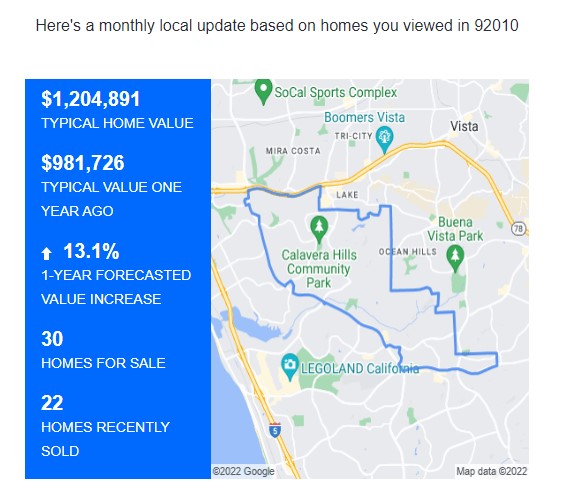

NE Carlsbad, 92010:

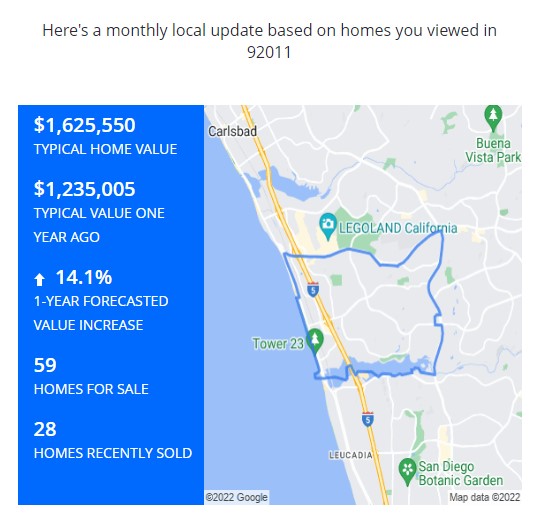

SW Carlsbad, 92011:

Carmel Valley, 92130:

Del Mar, 92014:

Encinitas, 92024:

La Jolla:

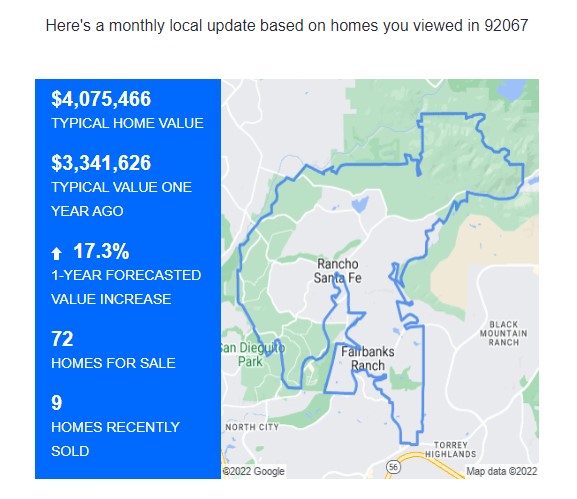

Rancho Santa Fe, 92067:

They do have website-viewer data that nobody else has, and hopefully they are using it to track the activity and make predictions.

I’ll find someone to buy my $2,295,000 listing in La Costa Oaks, and it could be the last LCO listing of the year. It will mean that LCO sellers will be expecting at least $2-something in the 2023 selling season, which won’t feel like prices dropped much while buyers were on vacation.

If the reason the housing frenzy stalled was due to higher mortgage rates – and then mortgage rates come down – shouldn’t it ease the concerns? Unfortunately, the national doom-and-gloom is heavy and persuasive, and reliance on ivory-tower guesses can become a self-fulfilling prophecy.

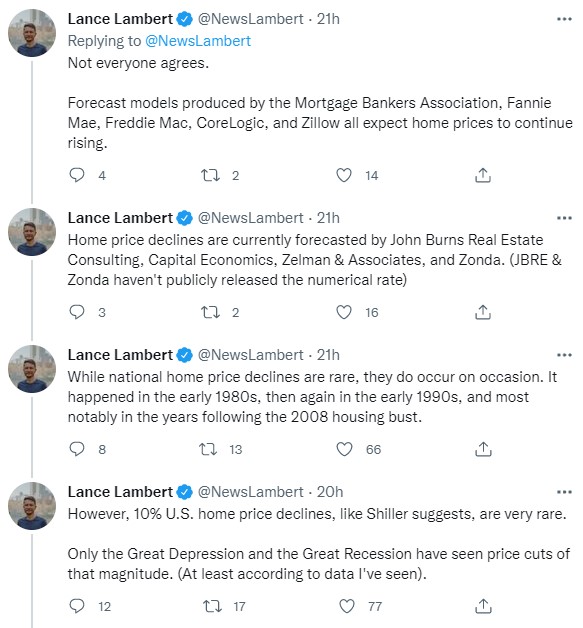

Shiller once again thinks the U.S. housing market is headed for trouble.

“Home prices haven’t fallen since the 2007–09 recession. Right now things look almost as bad,” Shiller said. “Existing home sales are down. Permits are down. A lot of signs that we’ll see something. It may not be catastrophic, but it’s time to consider that.”

A drop in home prices, Shiller says, looks very possible.

“The Chicago Mercantile Exchange has a futures market for home prices…That’s in backwardation now; [home] prices are expected to fall by something a little over 10% by 2024 or 2025. That’s a good estimate,” Shiller told Yahoo Finance. “The risks are heightened right now for buying a house.”

While Shiller thinks a double-digit decline in home prices is possible, many in the industry don’t agree. Over the coming year, home prices are expected to rise. That’s according to forecast models produced by the Mortgage Bankers Association, Fannie Mae, Freddie Mac, CoreLogic, and Zillow. Meanwhile, modest home price declines are currently being forecast by John Burns Real Estate Consulting, Capital Economics, Zelman & Associates, and Zonda.

Why do some industry insiders think home price declines are unlikely? For starters, the country outlawed the subprime mortgages that sank the market a decade ago. Not to mention, homeowners are less debt-burdened this time around. Back in 2007, mortgage debt service payments accounted for 7.2% of U.S. disposable income. Now it’s just 3.8%.

There’s another reason some firms refuse to get bearish on home prices: a historic undersupply of homes.

“Our economists have been chiming in on this for a bit now: The market is slowing down, but homes aren’t getting cheaper anytime soon. Price growth will slow/flatten (when compared to the breakneck start of the year), but the lack of supply is a fundamental pressure that will keep values aloft,” Will Lemke, Zillow’s spokesperson, tells Fortune.

In the eyes of housing bears, firms like Zillow are underestimating the possibility of oversupply. In their view, there’s a chance all those spec homes under construction could see markets like Atlanta, Austin, and Dallas get oversupplied in 2023. If that happens, it would put downward pressure on home prices.

“Housing is believed to be structurally undersupplied, but we run the risk of finding more homes on the market than buyers in the near term due to cyclical factors. I think there’s full awareness that in some markets, an increase in inventory may hit at a bad time—a time where demand has notably pulled back,” Ali Wolf, chief economist at Zonda, tells Fortune. “We are not under the belief that home prices only go up…Our forecast calls for a modest drop in housing prices.”

It doesn’t do any good to lower your price if there are no buyers. Sellers of superior homes should wait it out and take their chances later….because the next selling season is right around the corner.