Yesterday I joined Molly of Real Talk Media for a couple of thoughts about next year’s market:

The key to market conditions will be the inventory – no surprise there.

If there was a surge of newer McMansions for sale that were upgraded, well-presented, and had decent backyards, it would light the market on fire, mostly because we haven’t had many of those.

But it is more likely that we will have more of what we’ve had lately – homes for sale that are of the scratch-and-dent variety. They are ok, but not the premium creampuffs that every buyer desires.

The higher-end market will probably struggle a bit as sellers and agents slip back into the old normal where they ‘list ’em high and let them ride’, believing that it takes months to sell a more-expensive home. It doesn’t, but if you don’t have to sell, have plenty of time, and you’re not going to give it away, it is a fine strategy. Call Opendoor and see what they say.

There will be fewer realtors overall, and hardly anyone working with buyers – it’s too hard, and too time-consuming. With less good help, the price will really need to be right for buyers to proceed on their own.

Pricing? We don’t have a good way to measure, just bad ways. The median sales price will probably trend downward due to fewer of the higher-end sales. But sales of the sub-$3,000,000 creampuffs between La Jolla and Carlsbad will determine whether the median sales price goes up or down.

Yes the -0.01% isn’t much, but didn’t every casual observer think mortgage rates were going to rise again? That we were heading for 6% or 7% or 8%?

Everyone is going to get used to mortgage rates in the 5s, and by springtime this will all settle down and we’ll get back to a relatively normal market again.

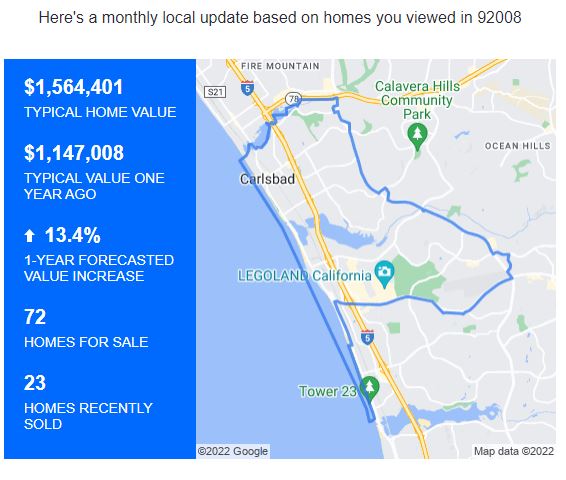

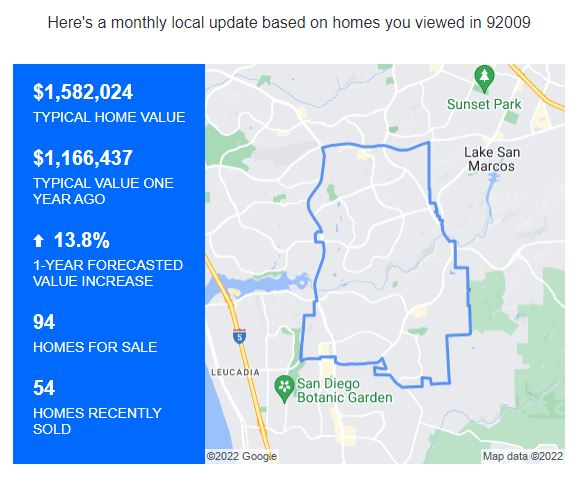

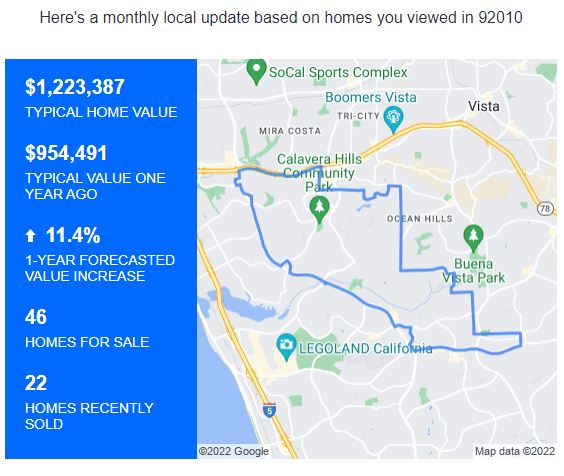

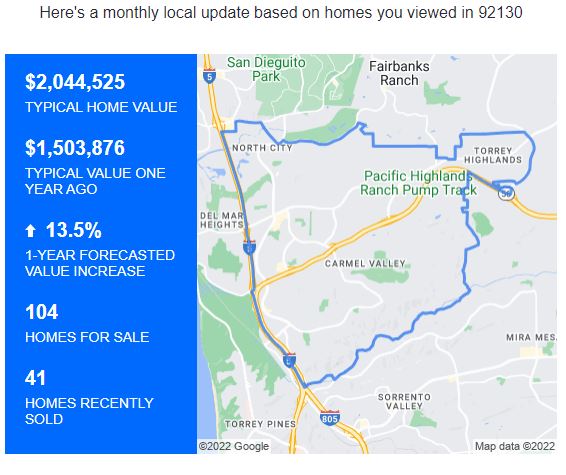

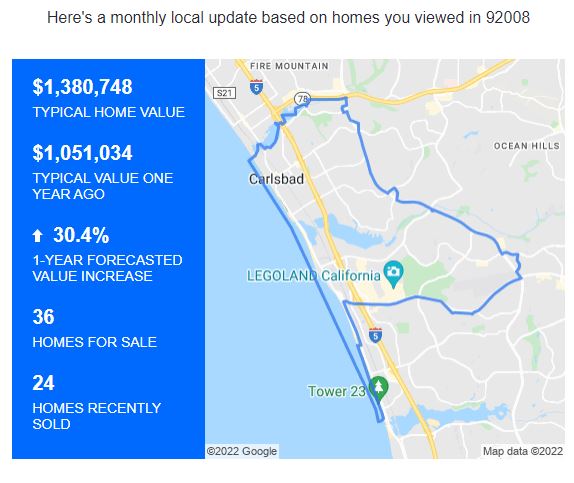

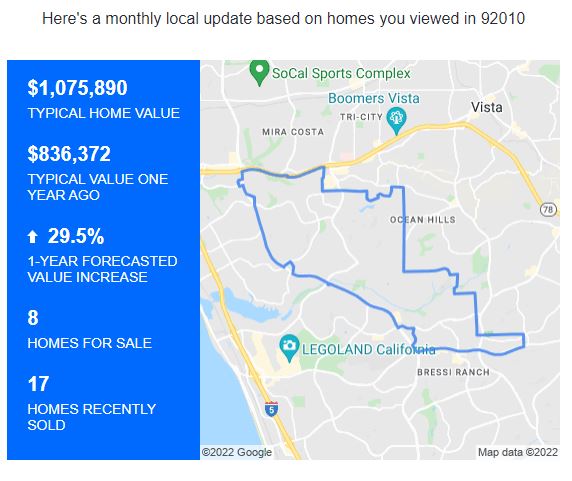

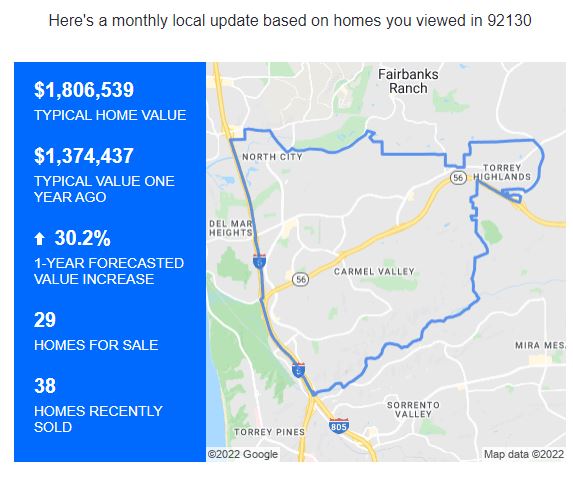

The latest Zillow 1-Year Forecasted Values are still expecting a fairly strong appreciation rate over the next year. In May, they were guessing +19% or more in all areas, so this looks like a soft landing:

NW Carlsbad, 92008:

SE Carlsbad, 92009:

NE Carlsbad, 92010:

SW Carlsbad, 92011:

Carmel Valley, 92130:

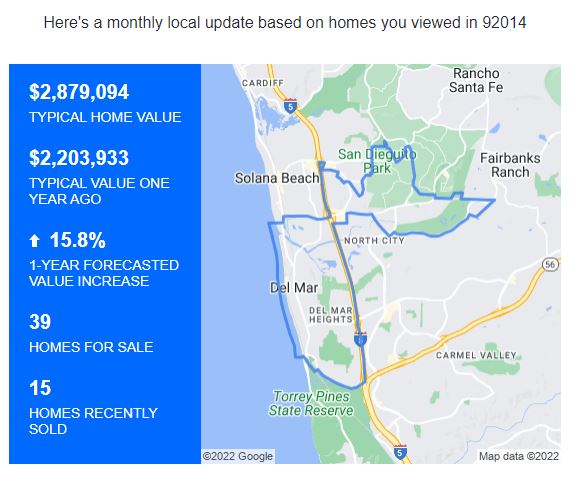

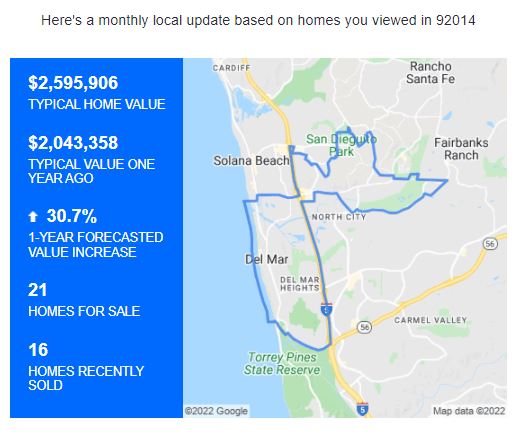

Del Mar, 92014:

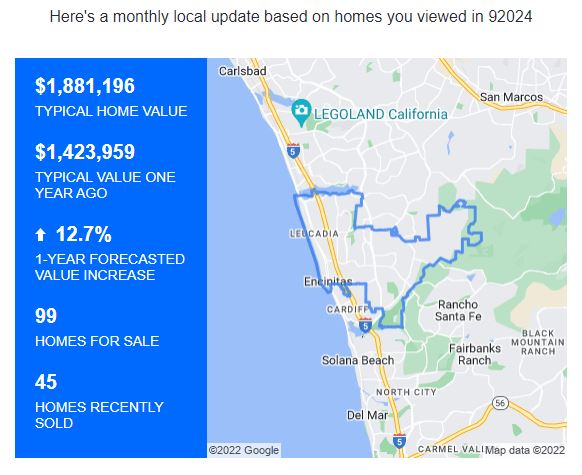

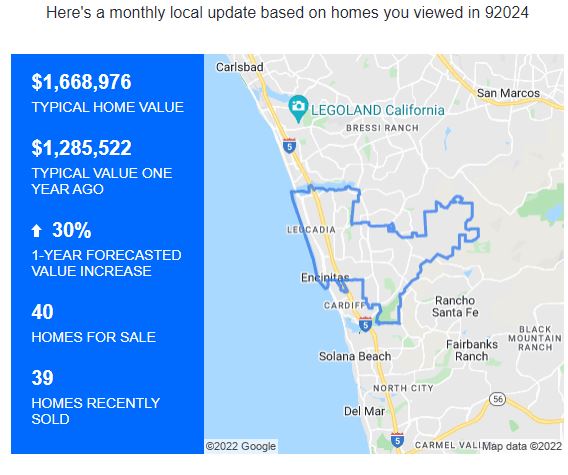

Encinitas, 92024:

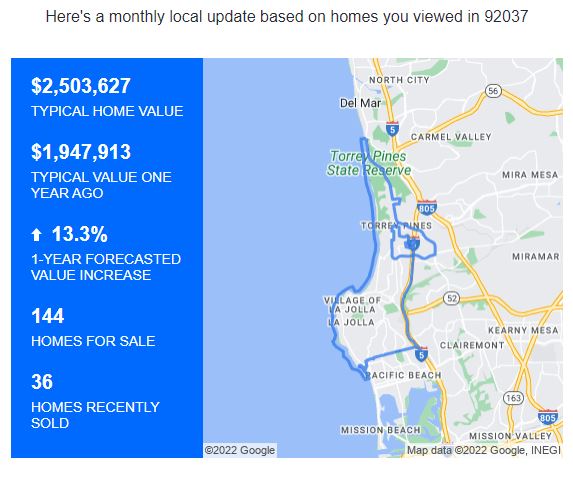

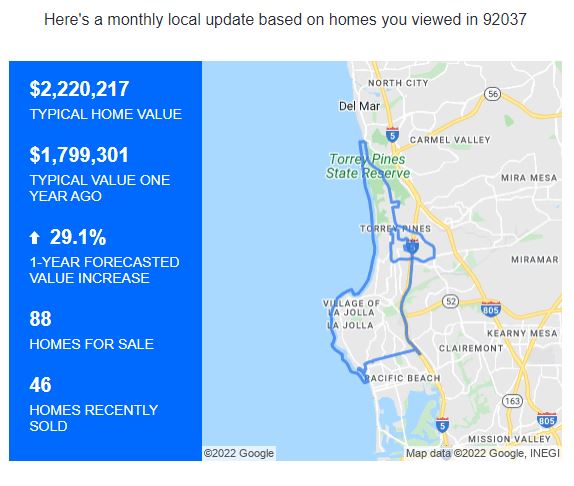

La Jolla:

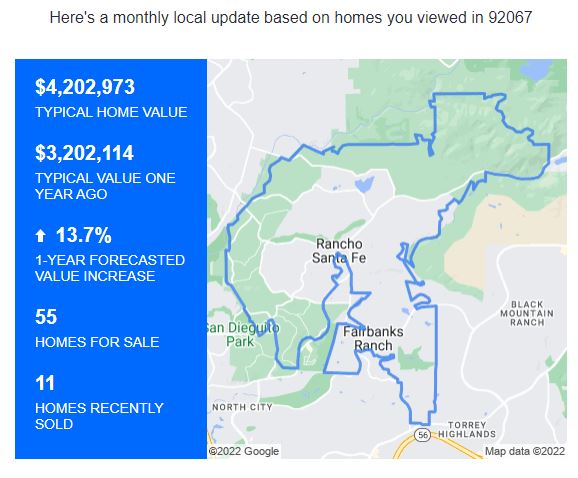

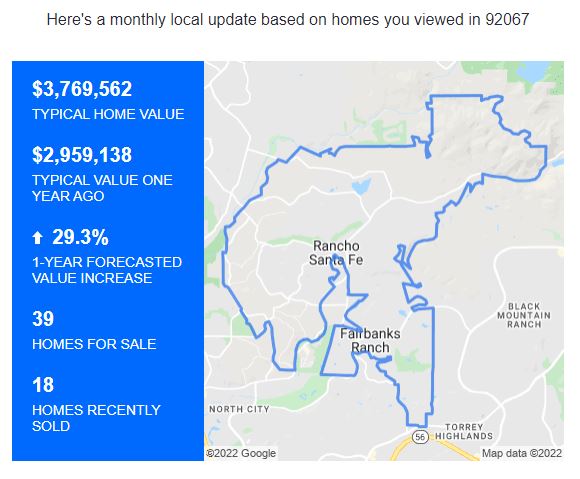

Rancho Santa Fe, 92067:

They do have website-viewer data that nobody else has, and hopefully they are using it to track the activity and make predictions.

By the end of today, the 30-year mortgage rate should be in the mid-6s – who would buy a house now?

Between higher prices, higher rates, and the hefty federal and state capital-gains tax, the move-up/move-down homeowners are effectively locked in to their existing home. It’s just too hard to make sense of a move, unless there is another strong reason to overcome those.

It would help if they don’t mind leaving town, and probably leaving California. But who wants to do that?

Without the move up-and-downers, the supply and demand will both be greatly diminished, and the number of sales should drop significantly. But there will always be sales!

Here are the potential buyers who might still be interested, even at 6%-7%:

The Mega-Rich – When they see something they like, they just buy it.

Tenants – They are sick of how high the rents have become, and they don’t want to keep moving around trying to ease the pain. Some inheritance would help.

Inheritance/Gifts – They have been waiting, and now their ship has come in.

Job Transferees – They are used to owning, and they usually have their company’s blessing – and relocation package ($$) to assist them with the transition.

Contarians/Opportunists – The deal hunting will kick into high gear.

Self-Employed – Lenders should ease up a bit on underwriting to keep the doors open, and the alternative mortgage products might get more love. Qualifying with 24 months of bank statements, instead of tax returns, and getting a 8% or 9% rate won’t sound as onerous as it did when rates were 3%.

Most Everyone at a 10% to 20% discount – Those who stay in the hunt might get lucky!

Hopefully, the floor for NSDCC sales should be around 100 per month while the market recalibrates in preparation for the next selling season.

If sales drop below 100 per month, then I’ll be looking for the panic button!

Coming off the initial covid months, everyone thought the red-hot market was an acceptable reaction to the way our world had changed. But it’s gone too far, and somebody had to do something – and the Fed is going to do it again tomorrow, which will continue the rise in mortgage rates.

It means sales are going to tumble, which is nothing we can’t handle.

Here’s how it looks so far:

NSDCC June Sales

2017: 360

2018: 299

2019: 282

2020: 274

2021: 357

2022: 61

Currently there are 198 homes in escrow, and 68 of those were marked pending this month.

Of those that went pending prior to June 1st, let’s guess that 100 of them will close in June – and there might be a few others that are just coming together this week with a quick close date in June too.

It will make for around 180-200 NSDCC sales this month! It’s quite a bit lower than usual, but we’ll survive.

We’ll have more unsold listings, longer market times, price reductions, and fewer sales – it’s all part of the recalibration! Additional price reductions are an unreliable indicator because you don’t know how crazy the recent list prices were in the beginning, and they have never been so optimistic, even for the frenzy.

The closed-sales pricing will be the last thing to change, if at all.

I’m sticking with my +/- 5% for NSDCC pricing here in Plateau City.

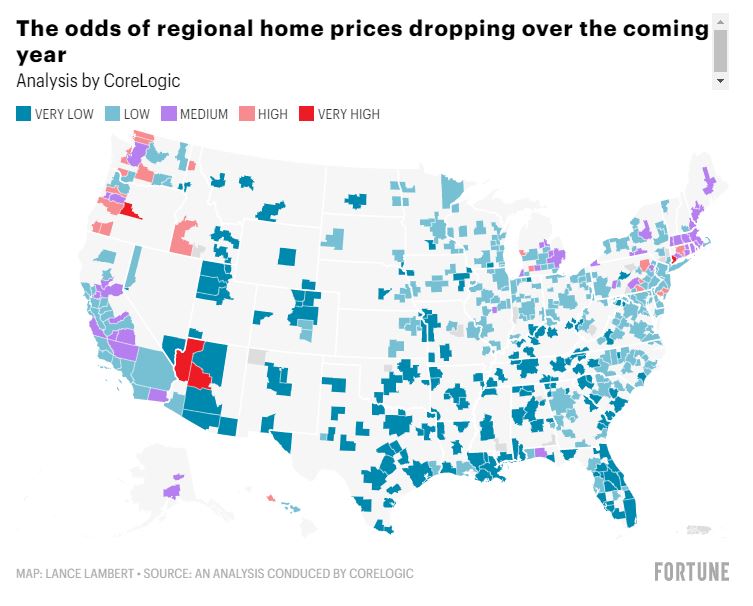

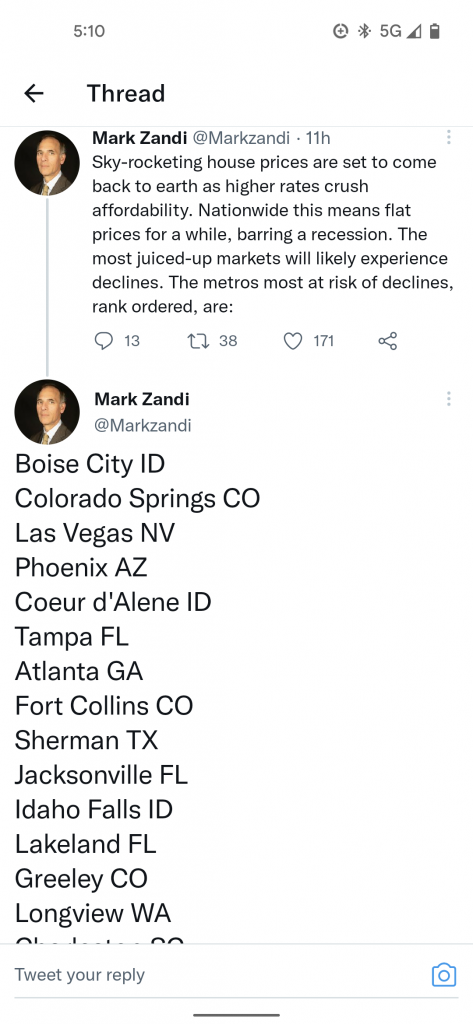

The headline writers are having fun with the current real estate market. They must challenge each other with whom can come up with the most outrageous headline, regardless of what’s in the article.

In this week’s article, he says, “that we’ve officially moved from a housing boom into a “housing correction.”

“The housing market has peaked…everything points to a rolling over of the housing market,” Zandi says. “In terms of home sales, they’re falling sharply. Housing demand is coming down fast. Home price growth [will] go flat here pretty quickly; we will see [home] price declines in a significant number of markets.”

But further into the article, they lay out the caveat that you see in every doomer article:

To be clear, Zandi doesn’t see a 2008-style housing bust or foreclosure crisis. While the spike in mortgage rates has pushed the housing market into the upper bounds of affordability, we don’t have the credit issues that plagued us last time. Homeowners are financially better off than they were in the lead-up to the 2008 financial crisis. This time around, Zandi says, we also don’t have widespread subprime mortgages. Also, if nationwide home prices do begin to plummet, he says, the Fed could always ease up on mortgage rates.

That said, Zandi says some regional housing markets have become historically “overvalued” and could see home prices decline 5% to 10% over the coming year. If a recession does come, Zandi says price drops in those markets could grow to between 10% to 20%.

Buried further is the map (above) that shows the areas with the greatest odds of home-price declines. There aren’t many, and none are in California.

None of these analysts want to consider that to have home prices decline, there has to be sellers who will sell for less. It’s much more likely – like 10x more likely – that our market will just stall out as sellers wait it out, rather than take less. They’re not going to give it away!

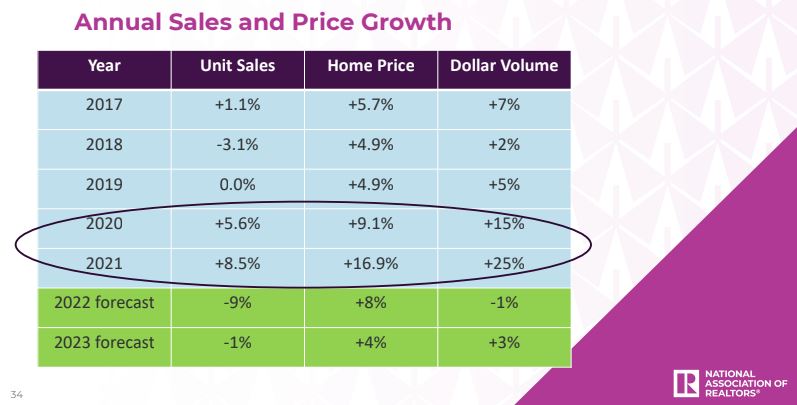

Yesterday, Lawrence Yun predicted that home sales will fall by 9% this year, and home prices will rise by 8%.

At the beginning of the year, his forecast was:

2022 Home Sales Forecast: -2%

2022 Home Price Forecast: +2.8%

2022 Mortgage-Rate Forecast: Rates to rise to 3.7% by the end of 2022.

His forecasts are just guesses, and subject to change!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

NAR calculates purchasing a home is now 55% more expensive than a year ago. These rising mortgage rates and prices hurt affordability, and although wages are improving, Yun says they are “wiped away” due to inflation.

“Wages have risen by 6% from one year ago and that’s good news,” he continued. “But inflation is at 8.5%.”

He estimates inflation will remain elevated for the next several months and that the market will see further monetary policy tightening through a series of rate hikes. Citing a five-month decline in pending home sales, as well as a drop in newly constructed single-family sales, Yun predicts the higher mortgage rates will slow the housing market.

I don’t care what color he’s seeing, if he sells his tony golf-course estate today and thinks he will buy it back later for less, he will be in for a rude awakening. Without foreclosures (now mostly outlawed in California) causing banks to give away homes, there won’t be any more downturns or cycles. But for those who agree with him, yes – please sell!

Bond manager Mark Kiesel sold his California home in 2006, when he presciently predicted the housing bubble would pop. He bought again in 2012, after U.S. prices fell more than 30% and found a floor.

Now, after a record surge in prices, Kiesel says the time to sell is once again at hand.

Sky-high values, soaring interest rates and other costs of homeownership — maintenance, property taxes and utilities — dampen prospects for future appreciation, according to Kiesel, chief investment officer for global credit at Pacific Investment Management Co. He’s weighing putting his Orange County house on the market and becoming a renter rather than an owner.

“I can look at my long-term 25-year charts and they tell me when to buy and sell and they’re flashing orange right now,” Kiesel, 52, said during an interview at Pimco’s Newport Beach, California, headquarters. “I think we’re in the final innings.”

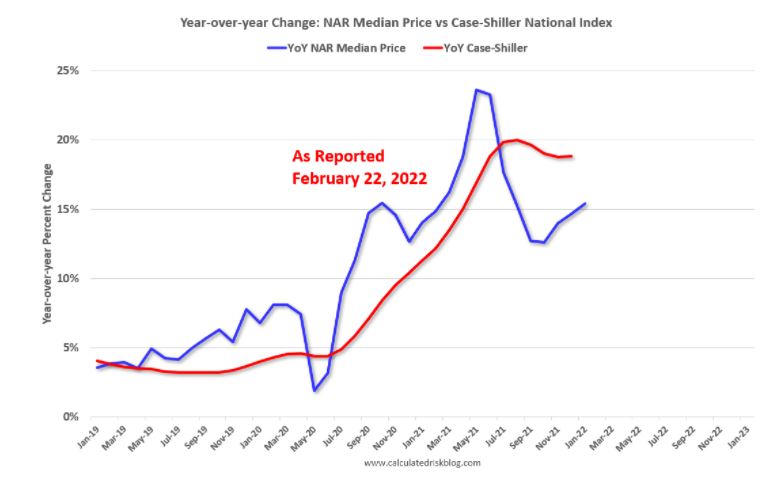

Home prices soared almost 20% in the 12 months through February, according to the S&P CoreLogic Case-Shiller Index, as pandemic moves, low borrowing costs and a dearth of inventory spurred heated competition for housing. But the market is now facing the fastest rise in mortgage rates in decades as the Federal Reserve works to tamp down inflation. The average 30-year rate is now 5.1%, close to a 12-year high, Freddie Mac data show.

Home sales contracts, a leading indicator, fell for the fifth consecutive month in March as rising borrowing costs added to affordability pressures, the National Association of Realtors reported on Wednesday.

Kiesel’s possible sale is a personal move and not a forecast of a crash by Pimco, which in March put out a note predicting “No Bust After the Boom” following years of housing undersupply. “Estimates of this secular shortage range from two to five million houses,” according to the authors.

But Kiesel’s past personal decisions have proved prophetic.

He sold his Newport Beach house in May 2006, calling housing “the next Nasdaq bubble.” Home prices peaked that year before going on to plunge, triggering the global financial crisis.

“It’s not just houses that will be for sale,” Kiesel said in a June 2006 interview. “You’re going to see financial assets for sale over time, and ultimately corporate bonds.”

Then in May 2012, Kiesel decided it was time to own again, buying a golf course-adjacent home.

“For those of you renting or on the sidelines, I recommend you at least consider getting ‘back in’ and buying a house,” he wrote in a credit market note. “The future is hard to predict, but U.S. housing is healing and is probably close to a bottom.”

U.S. housing prices have more than doubled in the past decade and the house Kiesel bought for $2.9 million in 2012 now has an estimated value of $5.5 million, according to Redfin Corp.

Buying a home in today’s market would likely yield about a 2% return, Kiesel said. He considers his home as an investment, refusing to form an emotional attachment to his property.

“It’s only a good investment if you buy it the right time,” he said. “If I were to buy a house today, I would probably get max 2% return on it. And I can find other things I can make money on other than a house.”

From yesterday’s article, which also ran in the SDUT today:

“There are so many strange things going on right now,” said Edward Seiler, the associate vice president for housing economics at the Mortgage Bankers Association.

It has been 40 years since rates have risen like this alongside similar home price growth and high inflation. This time around, the United States also has a severe housing shortage. And then there’s a new and uncertain dynamic — the sudden rise of working from home, which has the potential to change what home buyers want and where they live.

“Nobody really knows what’s going to happen over the next year,” Mr. Seiler said. That makes it hard to predict when rates might start to act as a brake on rising prices.

Nobody?

I have to take a swing at that one!

There are many variables that could slow the increases in home prices, and higher rates are just the latest excuse. Prognosticators said that last year’s velocity was the reason the home prices would cool in 2022 – no one could imagine that they could go up as fast as they did in 2021 – yet NSDCC the median sales price has INCREASED 21% BETWEEN DECEMBER AND MARCH!

But will rising rates be the final blow, and home prices start to decelerate?

Let’s try to predict the path of mortgage rates in 2022. How much worse could it get?

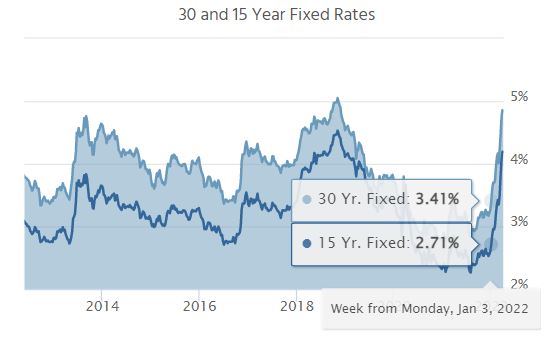

Mortgage rates are loosely tied to the 10-year T-bill, which has risen 0.824% this year:

The Fed is expected to raise their benchmark rate 1.5% this year (6 x 0.25%), so the 10-year yield has another 0.676% to go to reflect the anticipated 1.5% increase in 2022.

Mortgage rates have mirrored the 10-year, plus 1.75%, for decades.

Today’s 30-year fixed mortgage rate is 4.84% so let’s add the additional 0.676% = 5.516%. Because mortgage lenders are like gas stations – quick to overshoot rates on the way up, and sluggish on the way down – we will probably see 6% mortgages this summer as lenders continue to get out in front.

Let’s note that today’s 10-yr yield is 2.452% plus 1.75% = 4.202% which means today’s mortgage rate is about 0.6% overshot too high.

To further demonstrate the current mortgage-rate overshoot, here was the rate on January 3rd:

The 10-year has gone up 0.824% YTD, and mortgage rates have risen 1.43% YTD.

We are due for pullback, but the mortgage lenders will more likely just let it ride, knowing that more Fed increases are coming. They will panic (again) and mortgage rates will probably be touching 6% in a couple of months, but we should settle into a range of 4.75% to 5.5% by the end of the year – which isn’t much different than it is today. It coincides with the January’s 3.41% plus 1.5% = 4.91%.

Will higher rates than today affect home prices? It depends on the sellers – they get a vote.

If relatively nobody wants to sell at these prices, they sure won’t want to sell at lower prices! Rather than lowering the price, they will blame their realtor for their home not selling, and try again next year.

They’re not going to give it away!

There isn’t going to be a surge on inventory, because it would have happened by now. But I’m sure there are buyers running to the sidelines in droves, wanting to believe it’s going to be different, later. There will be fewer offers on homes for sale, and some may not get any! All we have to do is monitor the two metrics, the days-on-market, and the actives vs pendings, to know the trend.

But there are additional variables that will keep prices in this range:

The affluent buyers who aren’t as affected by rates. As long as we don’t run out of them, home prices will stay right where they are, or keep trending upward.

All buyers, affluent or otherwise, will buy the dips. There will be an occasional home priced under the comps (usually the dated estate sales) and buyers will jump to pay less. But they will get bid up to within 5% of retail and create the floor.

Buyers who are affected by higher rates can get a 2.375% ARM, fixed for ten years.

Realtors will keep pumping the seller’s market because it’s all they know.

We are pulling into Plateau City.

Even if the buyer psychology crashes, and only the desperate buyers stay in the game for the next few months, we can easily predict what will happen in the second half of 2022. Because both sellers and buyers who didn’t transact in the first half of 2022 will pack it in for the rest of the year, sales will plummet in the last half of 2022. It’s what happens in the early stage of a market shift, because sellers can’t believe they missed the peak and would rather wait, then lower. It will takes several failures before sellers re-consider their price accuracy – and some never will.

The NSDCC median sales price in December was $2,165,000. In March, it was $2,625,000.

I expect that the December, 2022 median sales price will be within 5% of $2,625,000 (plus or minus).

Then in 2023, the market will be flooded with lookers, who will be hoping for lower prices than what they remember from summer. But sellers will be packing a little extra on their price, just in case.

What do you think?

Before commenting, spend 15 seconds to watch this response to a ~$3 million off-market listing:

Zillow has also done a reversal on where they think home prices are going.

After forecasting three months in a row that homes in our local zip codes would be rising around 20% in 2022, their most recent guesses dropped to around +16% here:

They have been sending me their forecasts one by one over a couple of weeks. Here are their forecasts I’ve received at the end of February for our local areas (more to come):

NW Carlsbad, 92008

SE Carlsbad, 92009

NE Carlsbad, 92010

Carmel Valley 92130

Del Mar, 92014

Encinitas, 92024

La Jolla, 92037

Rancho Santa Fe, 92067

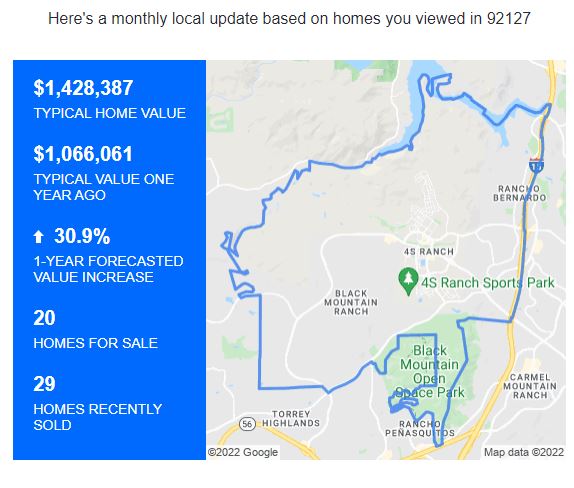

West RB, 92127

Can we do +30% two years in a row? Or is Zillow off their rocker?

They do have something that none of the ivory-tower economists have – the real estate viewer data.