Another story demonstrating how free enterprise is being squeezed:

California is taking steps to avoid a repeat of the conversion of thousands of single-family homes from ownership to rental properties as occurred during the Great Recession. In late September, the state’s governor Gavin Newson signed a bill that will give tenants, affordable housing groups and local governmentsthe first crack at buying foreclosed homes.

As homes were foreclosed by the millions following the housing crisis, Wall Street stepped in and investors, according to Zillow, gobbled up over 5 million homes, turning them into rental properties. They were bought as individual homes, via bulk sales of lender real estate owned (REO), or as distressed loans upon which the investors later foreclosed.

It was expected that these houses would return to owner-occupied status once home prices recovered and the investors, largely big hedge funds, could realize a profit. Instead they have found ways to manage the geographically dispersed properties and continue to hold hundreds of thousands of them.

This has been problematic. While the investor purchases helped put a floor under home prices at a time when there was little appetite for buying distressed properties, it has continued to reduce the inventory of available homes for sale. There have also been many complaints of tenant abuses and deferred maintenance. Many of these were spotlighted last March in a New York Times Magazine article, “A $60 Billion Housing Grab by Wall Street” by Francesco Mari. We summarized her work here.

The California legislation, SB1079, was the brainchild of an activist Oakland group, Moms 4 Housing. It bars sellers of foreclosed homes from bundling them at auction for sale to a single buyer. In addition, it will allow tenants, families, local governments, affordable housing nonprofits and community land trusts 45 days to beat the best auction bid to buy the property. It also creates fines of as much as $2,000 per day for failure to properly maintain properties.

So far, the COVID-19 pandemic has not resulted in massive foreclosures due both to mortgage forbearance programs and a foreclosure moratorium put in place by the U.S. Congress’s Cares Act. Still mortgage delinquencies are rising, and weekly first-time unemployment claims have remained above 800,000 since March. Most forbearance plans are due to expire by next March lacking further government action.

With our unemployment rate being higher than it was during the Great Recession, it would be prudent to worry about homeowners defaulting on their mortgages…..except we didn’t even make this list:

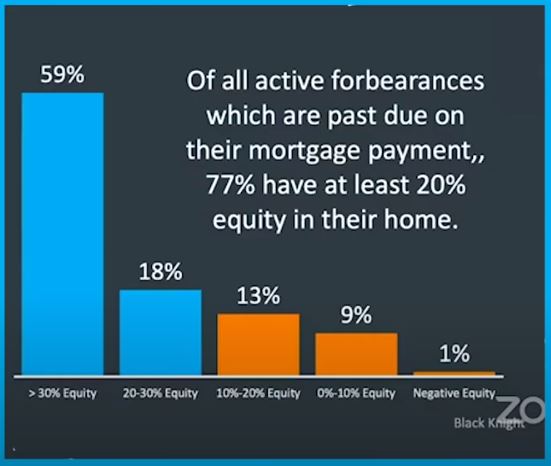

Those who do go into default should find their lenders being very accommodating even after the moratoriums expire…..unless the homeowner has a load of equity, which virtually all do in San Diego.

Realistically, the worst thing that will happen is that they will have to sell!

Our reader ‘just some guy’ sent in this article and quipped about these writers who insist on promoting a foreclosure scare due to the pandemic. But it is worth noting because it could become a self-fulfilling prophecy just due to the lack of a counter-argument being published at large.

This article is quick to point out that there isn’t a problem yet:

Even after the foreclosure moratorium expires, homeowners on a government-backed loan will have a forbearance option to fall back on, so there’s no need to panic just yet. But digging into mortgage-delinquency data shows how much water is building behind the dam that is these government backstops.

In January, just 3.22 percent of mortgages were in delinquency. By May, that number shot up to 7.76 percent — about three points shy of where the delinquency rate peaked during the financial crisis of 2008, which was at 10.57 percent.

Prior to the the pandemic in March, the number of mortgages in forbearance was fewer than 100,000. Currently, there are roughly 4.5 million mortgages in forbearance, although this is obviously a reflection of homeowners having the option of forbearance, but it gives you a sense of the scope.

Not every homeowner in forbearance is past due on their payments; some went into forbearance as a precaution, or just because they could. Some homeowners were in forbearance and have since gotten out, either because there didn’t end up being a need or they got a new job. For June, 21 percent of mortgages in forbearance were current on their payments, but as the pandemic goes on, more will enter into serious delinquency that would normally trigger a foreclosure.

With the forbearance option available for up to a year, economists have baked into their models a wave of foreclosures in the spring of 2021, which they say would cause a very rare drop in U.S. home prices.

I haven’t heard anyone predict falling home prices in 2021, and Zillow is forecasting a 5.7% increase.

We also know that the loan-modifications that worked last time will get employed again before banks lose a penny. The only people they might foreclose on are homeowners with sufficient equity, but if it comes to that, then those folks will sell their house instead and make out nicely.

It does add an interesting component to next year’s selling season though, which should be a humdinger!

BTW, I don’t have any insider info on the rumored Compass/Keller Williams merger. Even if it’s been discussed, it’s hard to believe the egos involved would allow for it.

This presentation covers both sides of the concerns about home values plunging because of the effects of the pandemic on the economy.

Suze says don’t buy a house until later this year because there could be foreclosures, and David points out that the CARES Act already gives those in forbearance at least 6-12 months. I’ll point out that the rules changed after the last crisis, and now lenders don’t have to foreclose if they don’t feel like it – which makes foreclosure an option, not a requirement. It’s a huge change that Suze doesn’t see.

Our society is now geared to take advantage of other people’s misfortune, so insiders will pounce.

A viewer’s comment on YouTube led me to this terrific inside view of the 2008 financial crisis, and the resulting impact on the world. It rightly blames the entire fiasco on the Tan Man, who pitched his mortgages to Wall Street based on the yields generated if borrowers made their full-interest payments, when in reality, only a much smaller minimum monthly payment was all that was due.

It’s eerie to watch today as our financial markets are in question again:

I make a quick comment in at the 2:38-minute mark, standing in front of the most-expensive REO listing we received in the era – a 2,900sf house in downtown Carlsbad that sold for $603,000 in December, 2009. It’s still owned by those buyers! The realtor.com estimate today is $973,900.

They won’t foreclose on you, but your credit score will be affected. From the AP:

Certain borrowers nervous about missed house payments got some relief as two major government backers of mortgages have said they’re stopping foreclosure work for the next 60 days.

The Federal Housing Administration and Fannie Mae announced moves to help out borrowers behind on house payments as part of effort to mitigate the financial impact of the coronavirus outbreak.

Loan servers of FHA and Fannie Mae loans have been directed to stop starting new foreclosure actions; suspend foreclosures in progress; and not evicting residents of foreclosed properties with loans backed by these agencies. Borrowers in financial trouble are encouraged to contact their loan servicer to inquire about various relief programs.

“Today’s actions will allow households who have an FHA-insured mortgage to meet the challenges of COVID-19 without fear of losing their homes, and help steady market concerns,” said U.S. Department of Housing and Urban Development Secretary Ben Carson. “The health and safety of the American people is of the utmost importance and the halting of all foreclosure actions and evictions for the next 60 days will provide homeowners with some peace of mind during these trying times.”

Kayla flew home from Manhattan this morning on Delta – there were only 20 people on the plane!

Her Douglas Elliman offices are closed through March 31st and probably longer. Hopefully she didn’t bring the bug back with her, but it’s better than her catching it there and having to cope with it alone.

She loves being in Manhattan, and plans to go back, of course.

But what will the market be like for newer agents everywhere?

The big, successful agents will use this off-time to prepare additional marketing materials, and be ready to go once the virus is done. We’ll have 1-3 months of pent-up supply and demand, so we’ll try to squeeze the whole 6-month selling season into 60 days. The crafty experienced agents will be glad to facilitate those sales, but there won’t be enough to go around for everyone.

I’m guessing that we will probably sell 20% to 30% fewer homes this year, and it could be less. The sales will drop off long before sellers think about dumping on price, and because the virus isn’t a permanent change in the marketplace, it will be too easy for sellers to wait it out instead. It will be tough on every agent who is on the edge.

Somebody said today that they expect to see big price declines and foreclosures in the next 2-3 months, but that’s not happening. The moratoriums are in place, and homeowners who can’t make payments will get as much time as they need. It’s more likely that we will experience the Big Stall-Out, with the market still airborne and just waiting for the engine to kick back on.

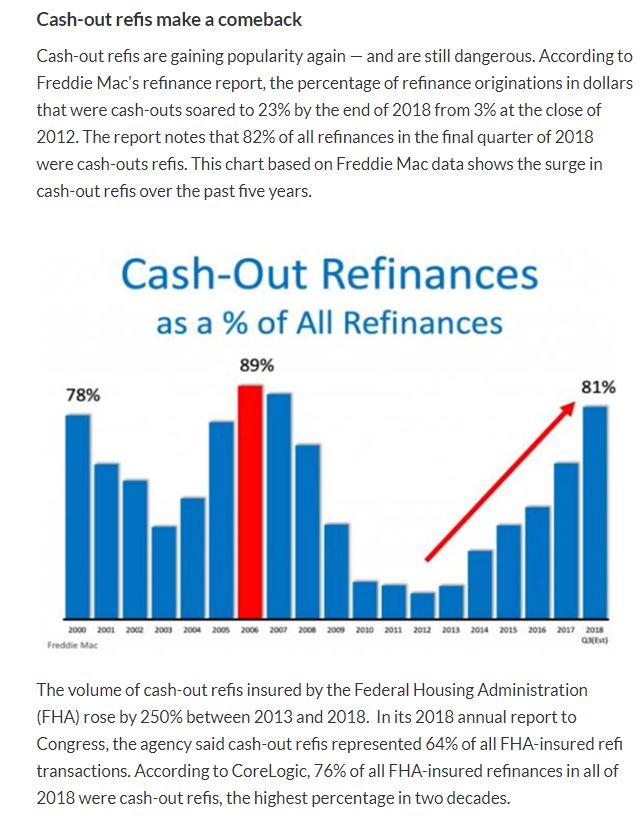

Low mortgage rates and large down payments are how buyers today are able to afford these lofty prices. Wondering where the big money comes from? Some of it could be from cash-out refinances:

The article has a couple of other zingers too – excerpts:

In recent years, wealthy homeowners have gotten into the cash-out refi game in a big way. A CoreLogic report in January 2019 found 230 active giant refinanced mortgages between $10 million and $20 million — most originated since 2013. Almost half of these loans were identified as cash-out refis. The average amount of cash pulled out was $6.6 million. Last year, the average had risen to $8.3 million.

Almost 10 million cash-out refis were originated during the wildest bubble years of 2004–07. While a significant number of them have been foreclosed, most still have not. As I noted in a previous column, mortgage servicers nationwide have been extremely reluctant to foreclose on long-term deadbeats since 2012.

Another column earlier this year laid out the enormous problem of modified mortgages that have re-defaulted one or more times. Close to two-thirds of all sub-prime bubble era mortgages had already been modified by 2015. The re-default disaster was so great that by mid-2010 there were more subprime modified mortgages re-defaulting than there were delinquent loans being foreclosed and liquidated by mortgage servicers.

The author is probably the biggest doomer on the beat. He called me once and insisted that I agree with him on his gloomy predictions, and when I wouldn’t, he hung up on me. But his articles here are a good reminder – whatever happened to those loan modifications?

Readers have wondered about the story of the billion-dollar property being bought for $100,000. It was the lender (who was the previous owner) who got the property back, and who is now in position to make a tidy profit on their original $45 million mortgage:

On Tuesday, it sold for a mere $100,000 at a foreclosure auction, a fraction of the $200-million loan outstanding on the property.

A markdown of 99.99%, of course, comes with some fine print. Any other buyer would have been on the hook to repay that loan — and this buyer has to eat that loss.

That’s because the buyer is the estate of late Herbalife founder Mark Hughes, which previously owned the property. The estate set this current saga into motion by selling it to Atlanta investor Chip Dickens in 2004.

Dickens borrowed around $45 million from the Hughes estate to buy the property, and that debt has since ballooned to roughly $200 million with interest and fees. Three years ago, Dickens transferred ownership to a limited liability company controlled by his partner on the project, Victor Franco Noval.

Noval is the son of convicted felon Victorino Noval, who pleaded guilty to mail fraud and tax evasion in 1997 and was sentenced to federal prison in 2003.

Unable to pay the debts, their limited liability company, Secured Capital Partners, tried — and failed — to declare Chapter 11 bankruptcy last month, which led the Hughes estate to force a foreclosure auction to either sell the property in hopes of recouping its losses or buy it back, likely losing the $200 million they were owed in the process.