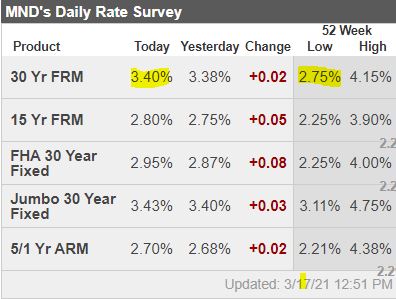

Mortgage Rates Continue Upward

One of these days, rates are going to matter.

Today is probably not that day.

But when we get close to 4%, then buyers are going to put on the brakes and expect sellers to do a little something for them, price-wise.

One of these days, rates are going to matter.

Today is probably not that day.

But when we get close to 4%, then buyers are going to put on the brakes and expect sellers to do a little something for them, price-wise.

My theory this week to explain what’s happening today?

The ultra-low mortgage rates are the problem.

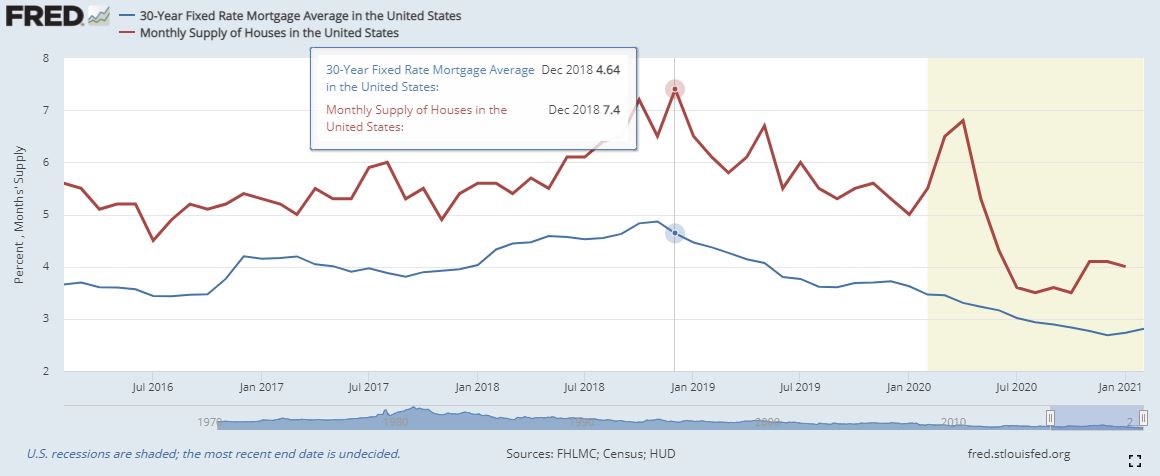

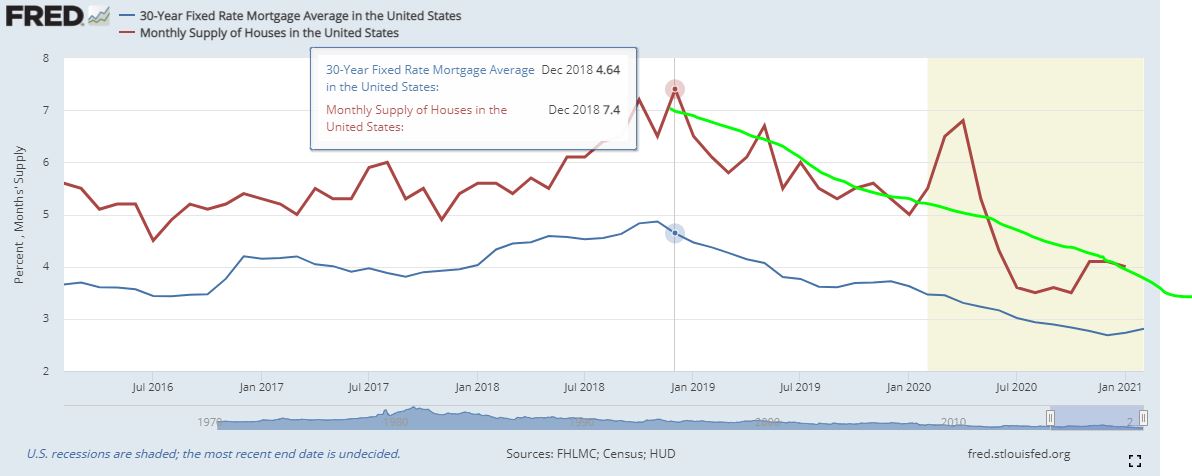

Specifically, the decline in mortgage rates over the last two years have caused more of the existing homeowners to refinance, rather than move. In the graph above, you can see how the supply of homes for sale has declined in a similar trend to mortgage rates. Low rates have spurred more interest from buyers, but the drop in supply hampers their ability to take advantage of it.

If and when rates rise, it won’t change the problem with low supply because the refinanced homeowners have packed it in – they’re not moving no matter what happens to rates. They are locked in forever!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

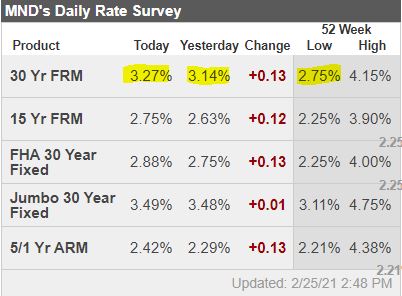

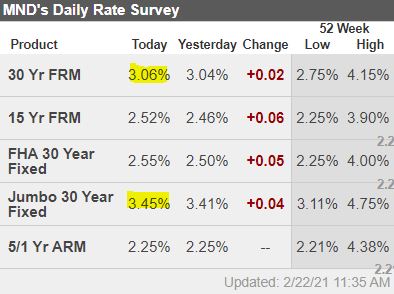

This is turning into the February mortgage-rate massacre, and there’s no real end in sight. But home sellers aren’t going to believe for weeks or months that they might have to back off their price, so don’t expect any changes.

To say that bond market volatility has been elevated recently is an understatement of extreme proportions. Things are happening that haven’t happened in years. Some measures of volatility rival the March 2020 panic surrounding covid, only this time, there’s no catalyst other than the market movement itself.

Today was by far the worst of the bunch when it comes to this most recent spate of volatility.

Most any mortgage lender added another eighth of a percent to their 30yr fixed rate offerings. Over the course of the past week, most lenders are .25-.375% higher. And compared to the beginning of last week, many lenders are a full HALF POINT higher. In other words, what had been 2.75% is now 3.25%. What had been 2.875% is now 3.375%.

Are this high rates in a historical context? Not at all. Before covid, they’d be in line with record lows.

But relative to the recent lows, this rate spike is getting to be about as abrupt as we’ve seen in the past few decades–not quite on par with the worst offenders, but close enough to be in their same league.

http://www.mortgagenewsdaily.com/consumer_rates/968604.aspx

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Rising rates only has moderate cooling effect on housing, says Black Knight’s Andy Walden from CNBC.

If you are thinking of selling your house this summer, expedite your plans!

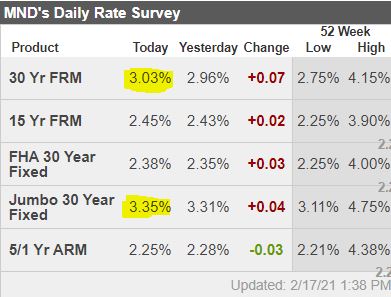

Volatility has returned to the mortgage market in grand fashion this week with many lenders quoting rates that are as much as a quarter of a point higher than they were last week. That means if you were looking at something in the 2.75% neighborhood on Friday, it could be 3.0% today. What gives?

The upward pressure is nothing new, really. It has existed in the broader bond market since August, but only recently began spilling over to the mortgage market. We’ve been discussing the increased risks of such a spillover in the event of a sharper bond market move and yesterday brought just such a move. Today was much more docile by comparison, but it didn’t do anything heroic to push back against yesterday’s weakness.

Still, there could be some promise of stability in the fact that the bond market was even able to hold steady today. Reason being: economic data and other events clearly suggested another bad day for bonds. Retail Sales surged at one of the best paces on record and inflation rose abruptly at the producer level. Both of those headlines make strong cases for higher rates, but Treasury yields ended the day slightly LOWER than yesterday. That sort of resilience may be a clue that bonds have had enoughweakness for now (bond weakness = higher rates, all other things being equal).

Mortgage lenders are WIDELY stratified in terms of rate offerings with the more aggressive crowd averaging 2.875% (no points) on top tier 30yr fixed refinances and the less aggressive crowd being closer to 3.125% (conventional 30yr fixed).

Link to Article

A good article by Matthew on the current rate environment:

Bonds find themselves in an interesting position heading into February.

On the one hand, there’s a well-established tepid recovery narrative that coincides with gradually rising 10yr yields for the past 6 months and, more recently, mortgage rates that begun to take notice. On the other hand, several of the inputs driving those trends are open to criticism, push-back, or other intervening factors that may collectively say “not so fast” to the rising rate trend.

Econ data can bat for either team in this regard and this week brings the month’s biggest reports with ISM PMIs and the big jobs report (NFP). A unified message from the data will likely matter to the bond market, but it might be hard to tell unless those “not so fast” factors are staying silent.

For the sake of clarity, let’s identify these teams.

Team Rising Rates

Team Not So Fast

Economic data occupies a very interesting space on both of these teams. Sure, it’s all about covid first and foremost, but covid’s market impact is really all about the economy. In that sense, econ data does more than anything to decide who wins this game.

So why don’t we see bigger reactions to the data? Simply put, even when it comes to significant reports, they’re nothing more than points scored in the middle of a very long, very close game. As long as both teams continue to score, econ data will be hard-pressed to cause a panic in the bond market. But if one team manages to dominate the momentum–i.e. multiple successive econ reports that are much stronger (or weaker) than forecast–rates would likely react accordingly.

Even then, the nature of covid and the current economic reality means that the data could still be questioned if there are current fundamental developments that logically argue that case. For instance, data could be tepid, but if covid case counts are dropping and vaccination rates are ahead of schedule, traders might trade a brighter outlook and simply wait for the econ data to confirm. Conversely, data could be on the up and up, but if something about the covid/vaccine situation deteriorates, traders could disregard near-term economic successes for fear of more lockdowns and unemployment.

http://www.mortgagenewsdaily.com/mortgage_rates/blog/966385.aspx

Excerpts here from an article yesterday about the Fed’s involvement. The rapid run-up in home prices is brutal on home buyers, but for home sellers, realtors, and the overall economy, it is great news. Expect that the Fed will be very accommodative for longer than it takes to get employment on track, which means we should have low mortgage rates – and higher home prices – for at least the next year.

But what if the run-up in home prices is temporary?

Does Powell expect home prices to come down when rates go up? I hope not, because sellers get a vote – and we know they will be VERY reluctant to sell for less. Either we will have low rates forever, or once they go up (back to 4-something), the bubble created won’t pop or crash – instead it will ooze like slime while participants grapple with an unprecedented marketplace with little or no help:

Powell explained that the Fed has had to use its extraordinary policy to help the economy with still more than 9 million people out of work.

“It’s very much appropriate that monetary policy be accommodative,” he said. Powell also said with regard to financial stability, the Fed considers asset prices, leverage in the banking system and nonbanking system, as well as funding risk.

“I would say financial stability vulnerabilities are overall moderate,” he said, adding the Fed’s goals are also to prevent long-term damage to the economy and make sure the financial system is resilient to shocks. He said he believes the run-up in housing prices is temporary, and the pandemic has created a surge in demand because of people working from home.

“I think he’s reluctant to talk about specific stocks and even when he was asked about the housing market, he feels as though some of that is specific to the idea that supply was constrained, and there was pent-up demand and it’s temporary,” said Michael Arone, chief market strategist at State Street Global Advisors. “I wouldn’t expect the Fed chairman to acknowledge that Fed policy helps create bubbles.”

The Fed’s zero rate policy has helped fuel a mortgage boom with record low lending rates. Home prices were up 9.5% in November from a year earlier, the strongest annual growth rate in over six years, according to S&P CoreLogic Case-Shiller Home Price Indices. It is one of the strongest annual gains in the 30-year history of the data.

Powell, during the briefing, said the latest run-up in asset prices was not due to monetary policy but due to news on vaccines and fiscal stimulus. “He’s overstating the ability of the Fed to help the economy and understating its ability to help markets,” said Peter Boockvar, chief investment strategist at Bleakley Global Advisors. “He keeps deflecting.” Boockvar said the Fed’s policy impact is clearly felt across markets, including junk bonds where yields are at historic lows and some prices are at record highs.

“They’re solely focused on the virus and they don’t care what the side effects are of what they’re currently doing. Buying $80 billion of short term Treasurys, how does that translate to better economic growth?” he said. “Powell was so nonchalant about these hikes in home prices. It’s just temporary. Tell that to the first time homebuyer who is trying to buy a home and keeps getting outbid.”

Rupkey said the Fed is more concerned about other problems and does not see an issue yet.

“This Federal Reserve is not going to respond to asset prices unless they go up another 100%. This Fed is more concerned than ever about maximum employment,” Rupkey said, “helping those on the very fringe of the labor market.”

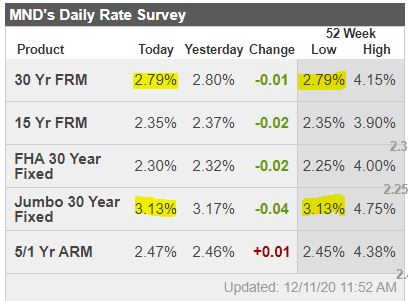

Rates keep hitting all-time lows!

It reminds me of Prop 19.

It would be nice to get the lowest rate in history and/or take the old property taxes, but there are additional variables to moving that complicate it. Not many can just get up and move today!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

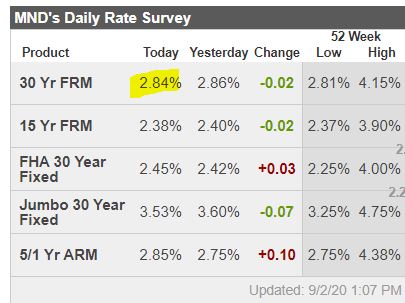

Rates have come back down a bit, so if buyers can just find a house to buy!

We’re sold out – all current listings are pending. I also had buyers yesterday who offered the high end of the variable-price range on a new listing and we got smoked by a higher bid that was $75,000 over the top end – yikes! There were six offers, according to the listing agent.

We kind of assumed they would have to keep rates low, but now it’s official:

The Federal Reserve announced a major policy shift Thursday, saying that it is willing to allow inflation to run hotter than normal in order to support the labor market and broader economy.

In a move that Chairman Jerome Powell called a “robust updating” of Fed policy, the central bank formally agreed to a policy of “average inflation targeting.” That means it will allow inflation to run “moderately” above the Fed’s 2% goal “for some time” following periods when it has run below that objective.

The changes were codified in a policy blueprint called the “Statement on Longer-Run Goals and Monetary Policy Strategy,” first adopted in 2012, that has informed the Fed’s approach to interest rates and general economic growth.

“Many find it counterintuitive that the Fed would want to push up inflation,” Powell said in prepared remarks. “However, inflation that is persistently too low can pose serious risks to the economy.”

Link to CNBC Article

Are you looking for an experienced agent to help you buy or sell a home?

Contact Jim the Realtor!

CA DRE #01527365, CA DRE #00873197