Yesterday’s blog post identified one solution for buyers which we’ll call the Gunslinger Special – where you wait patiently for the perfect home and when it hits the market, call JtR and give it everything you got.

What are the other options?

First, let’s note that you will get credit for any seller contribution to the buyer-agent fee. On my 2% Gunslinger Special, I’m going to try to get the seller to pay all of it, and sellers who are offering 2.5% means you get the 0.5% extra paid towards your closing costs. The form you will sign states this clearly, and it will apply to any agent you hire.

But it will be smart to expect to pay all the fee, and if the seller happens to pay some or all of it, then yippee. Why? Because the hot buys – the houses you want to buy – will probably have multiple offers. You don’t want to lose out because you insisted that the seller pay some of your agent fee. Eventually, there won’t be any seller contributions any more, it is just how fast we get there.

Option B – You are early in your search, and you’ve already experienced the pesky open-house agents hounding you to sign an exclusive-representation agreement. But the idea doesn’t sound too bad because you know you need to hire an agent to see homes for sale that aren’t open houses, and you wouldn’t mind the extra help.

Their fees will vary wildly. Any agent who is charging 1% or less is only looking to open a few doors and have a $500 transaction coordinator manage the paperwork for you. Those who charge more will razzle-dazzle you with their list of 10,000 Things I Do For You.

Have them show you one house as a trial before signing. If they say anything about a “dream home” or only identify the name of the rooms when touring the house (“here’s the kitchen”), know that you can do much better when hiring an agent.

You will end up making a decision based on your gut feeling, but no matter who you hire, check their Zillow profile. Punch their name and the word Zillow into Google search, and it will pop right up. Here’s mine:

If the agent works on a team, read through the reviews to find their sales and see what their buyers had to say. Being the “Neighborhood Expert” isn’t nearly as important as having a solid and recent history of closing sales with buyers.

When you go to sign their form, choose the option that you can cancel any time.

Option C – Go direct to the listing agent. Don’t do this just to get a piece of the commission by reducing the price or having them pay your closing costs – it’s doubtful either will happen. Go direct to the listing agent only if you are absolutely desperate to buy this home. It’s likely that you’ll still have to pay well over list and get little or no help, but hey, you should get the house!

You will still have to hire them as your agent to buy the house, and it is inevitable that every listing agent will have you sign this form to say you are unrepresented, and they don’t owe you anything. It will make you think about getting good help on your side, but once you engage with them, it will be too late. They will hold it against you and sell the house to anyone else just tp teach you a lesson.

All of these options are terrible, and I apologize on behalf of the real estate industrial complex for screwing up this lawsuit so bad that it makes home-buying more difficult. Trying to buy a house is difficult enough!

If you want to avoid this misery, buy a house before August!

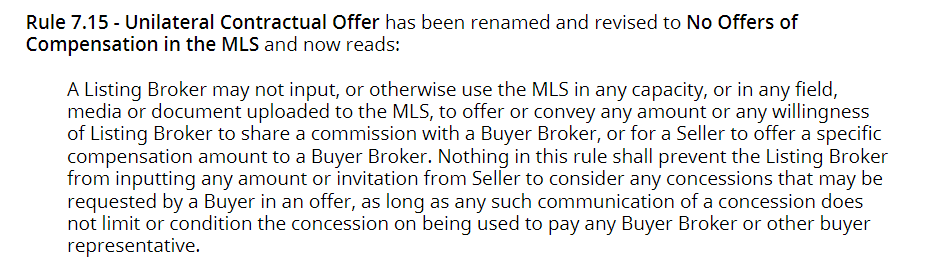

In mid-August, the new rule takes effect that NO buyer-agent commissions will be advertised on the MLS. Technically, sellers paying commissions to the buyer-agents will still be allowed for now – they just have to be negotiated outside of the MLS. There will be attempts to circumvent the new rule (see above), but sellers are going to think that they don’t need to pay anything.

I think we can expect seller-paid commissions to the buyer-agents to dwindle down to zero in the next 6-12 months. The DOJ has not insisted on this yet, but their attorney said the other day that they want the commissions decoupled, so it’s coming.

What’s next?

Buyers need to start getting used to the idea of paying for their agent.

Buyers will be required to hire a buyer-agent in writing to see homes, an idea that doesn’t sound great to anyone. Buyers don’t think they need an agent when they have Zillow at their fingertips, and agents will struggle to convince you that you need sign any agreement when you’re just looking.

I don’t want to be at your beck and call for the next 6-12 months and have to show you homes that I know you aren’t going to buy. But because we have a contractual agreement, you’ll be thinking……”hey, we hired you to be our agent, so snap to it.”

My Proposal:

You monitor Zillow via auto-notifications, and go to open houses all you want. You will be peppered by agents wanting you to sign an exclusive agreement for a year or two with the promise of showing you off-market deals that you won’t see on Zillow.

If you can resist that shady ploy, then when you finally find “the house” online, then I’ll get it for you. We will sign the agreement when I show you the house, and the agreement will be for this house only.

You’ll pay me 2% at close of escrow, with this guarantee:

If I don’t get you the house, you don’t have to pay me anything.

I’ll be the real estate gunslinger who will take care of business for you!

Our home values have been detached from “key economic factors” for years. More interesting would be studies that analyze what would happen to areas that are full of the older tract homes (1980s and before) that haven’t been improved much and are dumped onto the market for sale by money-grabbing heirs who just want fast cash. There could be a pricing downdraft of 10% to 15% in very short time – like a month or two.

Southern California home prices may seem insanely high, but two yardsticks of their underlying values suggest they’re not as crazy as elsewhere in the nation.

Let’s be clear. These measurements don’t say local homes are affordable. Nor does this math conclude what buyers are paying is normal. Rather, these studies show the overvaluation of Southern California homes compared with historical patterns is not massive on a national scale.

The first study is from Fitch Ratings, a Wall Street credit-quality tracking company. It compared pricing patterns in 50 U.S. metropolitan areas at year-end 2023 with key economic factors such as employment, interest rates and rents.

The other review is by two professors from Florida Atlantic University. Their price momentum model contrasted home prices in 100 metros for March 2024 with how costs gyrated over the long haul.

Fitch found one local problem spot: San Diego.

Its home prices, up 6.2 percent last year, were calculated to be 15 percent to 19 percent too high at 2023’s end, by this math. That’s the second-highest level of risk in the study.

Contrast that to Los Angeles and Orange counties, where prices rose 4.9 percent last year. Those homes were 5 percent to 9 percent overvalued at year’s end — the same risk score as the Inland Empire, where prices rose 2.1 percent last year.

The FAU professors pegged Inland Empire homes as the region’s most overvalued. The IE’s $579,000 typical house was 25 percent above its expected value in March 2024 — but that was only the 45th-largest overvaluation of 100 metros tracked nationally.

Homes in San Diego, worth $947,000, were 24 percent too high, by this math — the No. 50 overvaluation nationally. And in L.A.-O.C., with home prices running $947,000, overvaluation was 14 percent — the No. 85 overvaluation nationally.

Bottom line

The gaps between the two scorecards are a perfect example of what I’ve long said: The creation of any national ranking is part statistical science and part art. Just eyeball the most overvalued markets.

Fitch found seven metros were 20 percent to 24 percent overvalued: Memphis, Tenn.; Raleigh, N.C.; Indianapolis; Milwaukee; Nashville, Tenn.; Buffalo, N.Y.; and Birmingham, Ala. FAU’s top seven were: Atlanta (41 percent too high); Detroit (40 percent); Cape Coral, Fla. (39 percent); Tampa, Fla.; and Las Vegas at 38 percent, then Knoxville, Tenn., and Palm Bay, Fla., at 37 percent.

Or look at the differing levels of overvaluations.

Fitch graded all U.S. homes as 11% overvalued, with 44 of the 50 metros it tracked seen as overvalued by 5 percent or more. FAU’s median U.S. overvaluation was more than double — 24 percent with 97 of 100 metros tracked overvalued by 5 percent or more.

Or look at two Bay Area markets.

Fitch sees both San Francisco and San Jose as risky as San Diego — 15 percent to 19 percent overvalued.

But FAU professors have San Jose with their 15th-lowest risk (14 percent too high) and San Francisco with the third-smallest (2 percent too high).

Quotable

Contemplate the deviation in the national outlooks of the studies, too.

Fitch wrote that it “expects nominal national home price growth to decelerate from 5.5 percent in 2023 to 0 percent to 3 percent in 2024, which signifies the slowest pace since 2019. This forecast is based on the interplay between multiple factors, such as affordability challenges and a tight supply of homes, with the latter the more dominant factor in sustaining positive home price growth.”

FAU professor Ken Johnson wrote: “Home prices have become so out of line from their long-term trends that the risk of correction is rising. While it’s unlikely prices will plummet dramatically, price performance could go flat for the future, or home prices could see a slight decline even.”

Lansner is the business columnist for the Southern California News Group.

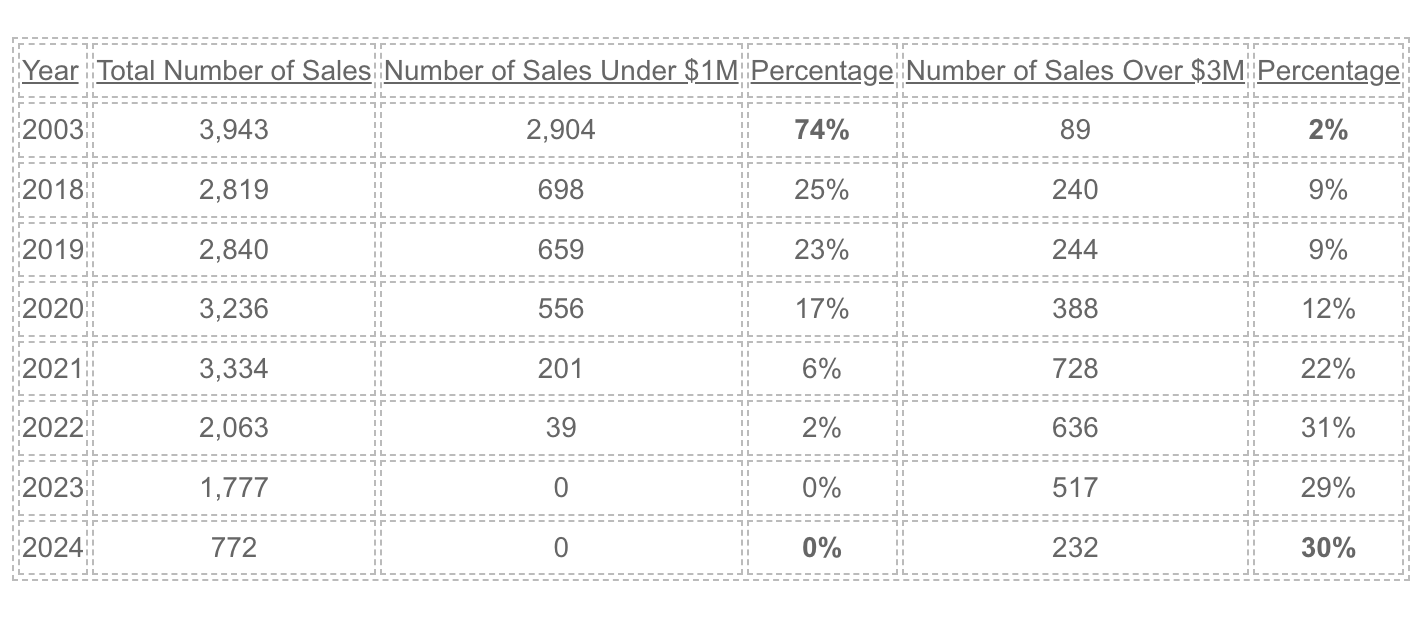

Here’s a snapshot of how fast the local market has changed. It went from a relatively-modest suburban area where 3/4s of the houses sold for less than a million dollars in 2003……to a very affluent market!

NSDCC Detached-Homes Annual Sales

True, the inflation rate since 2003 was 70% and a dollar doesn’t buy what it used to back then. But the median sales price went up from $730,000 in 2003 to $2,344,000 this month – an increase of 320%!

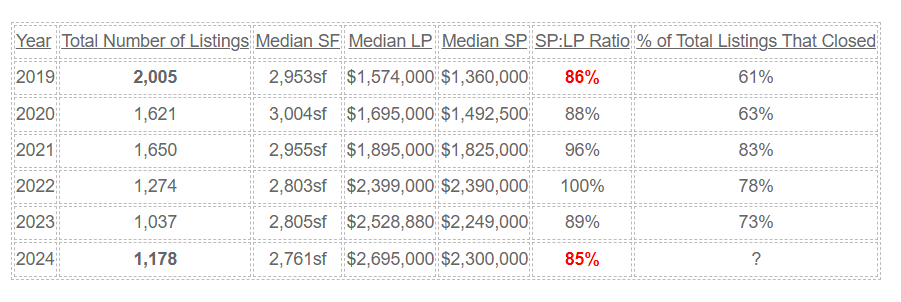

Can we use statistics to describe the market conditions today?

This chart above helps a little. Even though the number of listings is drastically lower than it used to be, apparently the market has been adjusting – mostly by price!

I mentioned that it seemed like everything is priced $200,000 more than it was last year, and the median list price reflects a similar number. Buyers aren’t taking the full plunge though, and the 85% SP:LP is a sign of normalizing (buyers having more negotiating power).

The frenzy that caused virtually everything to sell is long gone, and we’ll probably be back to having 30% to 40% of the listings not selling. This chart doesn’t show the number of refreshed listings where agents cancel and then re-input right away to “refresh” it – but be on the lookout. We will be seeing more of those this year.

Statistically, the market conditions look fairly healthy. Though different than the recent past!

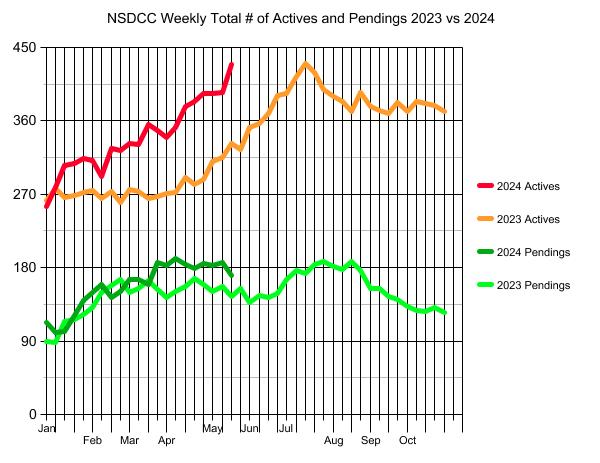

The NSDCC inventory has gotten off to a hot start in 2024 – it’s already at the level it was at in July of last year! As long as the pending keep up….oh wait.

Well, maybe there will be a surge of new pendings on the way? There was a late-summer surge last year, and if it was going to happen, it really should happen earlier this year too.

Pricing of the unsolds probably won’t change much:

The last time mortgage rates were 7% was 22 years ago when local home prices were about one-third of what they are today. As a result, the only semi-relevant comparisons are to last year!

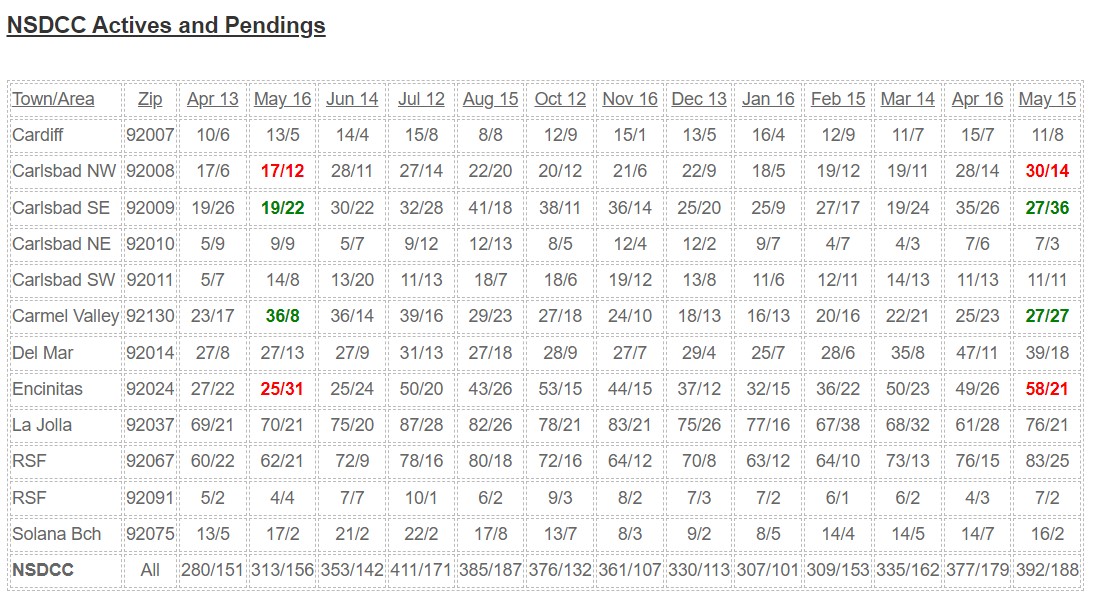

This chart shows identifies the hot spots, and not-so-hot spots, as compared to last year. Southeast Carlsbad and Carmel Valley both have substantially more pendings this year, and NW Carlsbad and Encinitas have roughly double the number of actives and where potential gluts might be forming.

Overall, there are 25% more active listings, and 21% more pending listings – so much of the additional inventory is getting soaked up.

Pricing is about the same as last year:

NSDCC Median List Price of Active Listings

May 15, 2023: $3,749,400

May 15, 2024: $3,895,000

NSDCC Median Sales Price in May

2023: $2,362,500 (178 sales)

2024: $2,310,000 (68 sales so far)

After last month’s eye-popping 200 sales, there was some hope that this month would be equally productive. But it looks like we’ll be fortunate to match last May’s count.

A new $3,000,000+ listing hit the MLS this week that was offering a 1/2% commission to the buyer’s agent.

They also noted that to show the property, buyer-agents needed to submit proof of funds (bank statement) and pre-approval letter plus a 24-hour notice was required. Only one photo was included and no videos or matterport. In other words, they aren’t interested in incentivizing the buyer-agents – instead, they will make it as tough as possible for them to earn a living here.

It’s ok with me if you want to publicly embarrass yourself in front of your fellow realtors.

But know that you are also contributing to the demise of buyer-agents.

When other agents see that you have no regard, or respect, for what buyer-agents do, then they will learn from you – and assume that this must be how the future of commissions is going to play out. Then they will do the same thing.

Because ‘commissions are negotiable’ is such a touchy subject, nobody in the business talks about it. But we should discuss the role of the buyer-agent, and how they will soon be extinct – which is NOT good for anyone involved, especially the buyers.

There are two other new listings this month (of 63) that are offering NO buyer-agent commission.

The agents are happy to note that it will be negotiated in the offer. Your list prices are ridiculously high, you make it hard to show, and you refuse to offer ANY commission rate? Why is that a sound strategy? How does that make any business sense?

If the listing agent is unwilling to commit to paying any commission, then they must be thinking that the eventual rate negotiated with the offer will be less than 2% – because if the listing agent was willing to pay at least 2%, they’d would publicize it as a feature, wouldn’t they?

These are listing agents that prioritize the torture of the buyer-agents over what is best for their seller. It’s a very strange control/dominance issue – and they should really seek some help with that before they take another listing.

As the market slows down – and the commission debacle will be a contributing factor to the slowdown – the buyer-agents will be needed more than ever. Will listing agents adjust in time, or just blindly run off the cliff like a lemming? I don’t have a lot of faith in the former.