The thing I think you miss most or maybe overlook is how overleveraged the average person is. I do commercial real estate and routinely have access to small business owners financials. Equity rich in their homes but cash poor with credit card debt and car loans up the wazoo. Any bump in the road will send them into disarray. Selling the house may be the only way they can survive. I think rocky times ahead.

We can speculate about what might be or what could happen, but in the end we’re all just guessing. Blog reader ‘Another Investor’ believes the opposite – that boomers are flush and not moving until they go feet first…..so we have balance here at bubbleinfo.com!

Let’s use statistics to help guide us.

If there were trouble brewing, then more people would be trying to sell.

Not everyone would sell, because their motivation might not be strong enough to take what the market would bear. So let’s just consider the number of listings – and also consider that there are probably more re-lists now than ever:

NSDCC Total Number of Listings Between Jan-Oct:

Year

# of Listings

2014

4,278

2015

4,583

2016

4,698

2017

4,248

2018

4,389

2019

4,327

Boomers or others aren’t trying to sell any more than they used to – so no obvious surge yet.

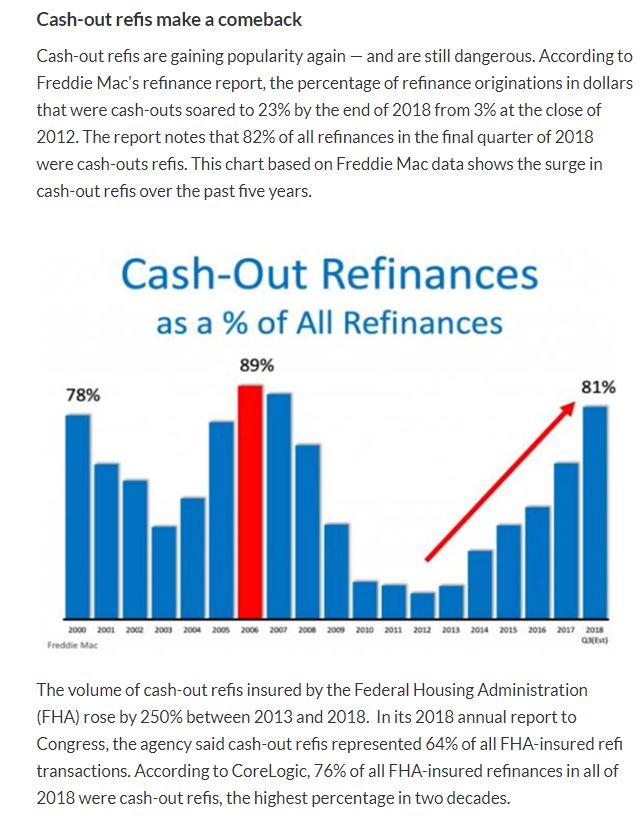

But the number of cash-out refinances was somewhat alarming yesterday. But everyone has to qualify for those mortgages, so even if more people are tapping their equity, they must be able to afford it.

But like Eddie89 said, the rules have changed, so all previous assumptions don’t apply.

I think any distressed homeowners will wait until the very end before deciding to sell because they really don’t want to move. It will drag out the inevitable, but it might just cause a softer landing because each homeowners ability to last longer will vary.

Let’s keep an eye on the number of new listings – that’s where you’ll see it first!

Low mortgage rates and large down payments are how buyers today are able to afford these lofty prices. Wondering where the big money comes from? Some of it could be from cash-out refinances:

The article has a couple of other zingers too – excerpts:

In recent years, wealthy homeowners have gotten into the cash-out refi game in a big way. A CoreLogic report in January 2019 found 230 active giant refinanced mortgages between $10 million and $20 million — most originated since 2013. Almost half of these loans were identified as cash-out refis. The average amount of cash pulled out was $6.6 million. Last year, the average had risen to $8.3 million.

Almost 10 million cash-out refis were originated during the wildest bubble years of 2004–07. While a significant number of them have been foreclosed, most still have not. As I noted in a previous column, mortgage servicers nationwide have been extremely reluctant to foreclose on long-term deadbeats since 2012.

Another column earlier this year laid out the enormous problem of modified mortgages that have re-defaulted one or more times. Close to two-thirds of all sub-prime bubble era mortgages had already been modified by 2015. The re-default disaster was so great that by mid-2010 there were more subprime modified mortgages re-defaulting than there were delinquent loans being foreclosed and liquidated by mortgage servicers.

The author is probably the biggest doomer on the beat. He called me once and insisted that I agree with him on his gloomy predictions, and when I wouldn’t, he hung up on me. But his articles here are a good reminder – whatever happened to those loan modifications?

The mainstream media is prone to look for anything wrong with the housing market, and they are known to manufacture it if they have to!

You’d think an article that begins with the headline above will include some ultra-high end cities like San Francisco or New York City, but it doesn’t. Instead, it mostly names small towns in flyover states as places that could be in trouble someday. The only two in California are Menifee and Bakersfield!

CNBC is usually the negativity leader, but thankfully in their article yesterday they did include one quote from a realtor (which is rare) and another from a buyer that sum up the general market conditions:

At an open house in Dallas on Sunday, a few dozen potential buyers toured a home listed at just under $1.4 million. The agent for the home said the market is still moving, but buyers are getting more picky.

“I definitely think it has softened a bit,” said Kelley McMahon a Dallas-area agent with Compass. “It’s not a seller’s market right now. Now is not the time for sellers to put out these crazy prices. Appraisals have gotten a lot harder, and buyers are a little more cautious. They’re more willing to take their time.”

McMahon said the concern is less about the overall health of the housing market, and more about the future of the economy.

“I think people are a little more cautious to pull the trigger, and I definitely think that people want to get through the election year, just kind of see what happens,” she added.

Dustin Collins and his wife toured the Dallas property while carrying their new baby. They are watching interest rates closely but don’t feel the pressure to move quickly, the way so many buyers did last year.

“For us, knowing that that kind of the frenzy is over, it’s more about finding the right house for us than paying too much for it,” Dustin said. “I feel like now houses are sitting a little longer, it just gives us a little more opportunity to find the house we want.”

Those sentiments describe a healthy environment where the price gap between the cream-puffs and the fixers is returning. Buyers are taking their time, and passing on the fixers or demanding a better price on them, and yet are willing to pay the money for a turn-key property in a quality location.

I describe the strategy for sellers here, because buyers need to be on alert 12 months out of the year. Why? Because you only care about buying the right house at the right price – which isn’t affected by the general market conditions. You are looking for the one-off.

Ryan is probably the most similar blogger to me because he’s in the business and sees what is actually happening on the street. He does a ton of charts and graphs, so if you’re analytical give his blog a look:

He sums up his current market conditions quite well with these thoughts:

Normal: The market felt really dull last year, but it’s been a somewhat normal year so far in 2019. There are certainly concerns about affordability, but from a stats perspective it’s been a pretty standard first half of the year. Pendings continue to be strong also, so buyers still clearly have a strong appetite for the market.

14 months in a row of slumping volume: Despite mortgage rates being low we’re seeing somewhat sluggish sales volume. In fact, sales volume was down 11.6% in the region last month and it’s down 8.6% so far in 2019. Moreover, we’ve had fourteen months in a row with lower sales volume compared to the previous year. In my mind it’s still best to say we’re having a slower year instead of a volume meltdown because levels aren’t alarmingly low by any stretch. Let’s watch this carefully.

Dude, rates will never get below 4% again: It’s been a little surprising to see how low rates have gone again, right? The narrative for a while was, “Dude, they’ll never go below 4% again. We’ve bottomed out.” Yet here we are. My sense is if rates keep going down it’ll only increase competition and artificially inflate prices. That would be temporarily nice for buyers, but an unfortunate byproduct is low rates in a wider picture tend to create less incentive for sellers to move. Why sell if you’re sitting on a 3.5% mortgage rate?

Purplebricks & the tech invasion: Last week it was announced that Purplebricks will be exiting the United States housing market after a 75% loss in shares. This company is going to the grave in the U.S., but the reality is we’re still in a market where tech companies are trying to disrupt the traditional real estate model. Next up? Zillow is said to be coming to Sacramento by the end of the year.

Joe Montana’s $49M overpriced listing: Former Quarterback Joe Montana listed his property for $49M and it didn’t sell because it was profoundly overpriced. In fact, the price has now been reduced to $28M. Many sellers are like Joe in trying to attract mythical unicorn buyers who will mysteriously overpay for some reason. My advice? Be aware that today’s buyers are incredibly picky about paying the right price.

The dream of selling at the top: I met a guy who wants to sell because he says the market might top out soon. His concern is a friend sold two years ago thinking the market was at its peak, but it wasn’t. The truth is it’s not so easy to time a market perfectly. We talk about how simple it is to do this, but most people pull it off from dumb luck more than anything. The reality is the bulk of buyers don’t buy based on price metrics, but rather lifestyle and affordability.

My thoughts on his thoughts:

The first time mortgage rates went under 4%, it did spark a mini-frenzy because no one had seen that before. Those who moved up – or refinanced – were able to mitigate their payment shock with a lower rate than they had before. But now the sub-4% rates are a yawner for those who already have them, and as a result, we’re not seeing the same enthusiasm we saw previously.

I’ll add a bit to his thoughts on Joe’s mansion. Are buyers being extremely picky? Yes, absolutely, yet it’s more about finding the perfect house than the perfect price. Once buyers find a great fit, they will pay whatever it takes. I saw a starter home in Carlsbad yesterday get four offers over list price, which will make it the most expensive sale for that model ever. But it was also a great location and house was dialed in.

Selling at the top used to be a big driver for decision-making back in the old days. But the market is so tight today that you can’t just go out and replace a quality home without a real struggle. Now, selling at the top is only one of the criteria for home sellers, and it’s dropped down the list for most.

I don’t know if they surveyed actual home sellers, but if these stats demonstrate the current sentiment, it shows how critical it is to list a home at ‘market price’ vs. ‘dream price’.

You’ve listed your home for sale, and no one is taking the bait. One month passes, then two. How long do you wait before you increase the odds of an offer by dropping the price?

According to a recent survey, most American home sellers opt to reduce their asking price after three months of zero offers.

Specifically, a survey of 1,000 consumers revealed that 33% would opt for a price reduction after three months, making it the most common choice.

Just under 20% said they would wait one month, while 17% would wait five months. For about 9%, it would take an entire year before they’d reconsider their price.

But for others, they’d rather not sell at all as opposed to selling for less than they originally wanted, with about 12% said they would never lower the price of their home.

The 33% would wait three months, but 38% would wait at least five months or longer to lower their price, if at all (17%+9%+12%).

Zillow says that the average price reduction is 2.9%, which isn’t going to impress buyers much. When prices were rising 5% to 10% annually, the market would catch up with a wrong price before too long. But now that pricing is flat, we don’t have that luxury – and we need to be smarter about price strategy.

Bill (in Giants jersey) from the Bay Area has been reading the blog for the last ten years!

He won the earlier contest for Padres tickets, so when he and his family were here on vacation, they took in the first game of the series last night – a 13-2 shellacking by the Giants! They got on TV too:

Congrats Bill and family!

The contest was predicting how many new listings we would have in the first two months of 2019. Bill’s guess was 777, which was the third lowest of those submitted – we all thought more sellers would want to cash out at these prices!

Yesterday’s doomer was looking for the right evidence – historically, one of the first signs of trouble is a surge of inventory. We saw it last time in the first half of 2006 when listings jumped 23% as sellers started scrambling to get out:

NSDCC Detached-Home Listings Jan 1 to June 30:

Year

Number of Listings

Median List Price

2005

2,892

$1,150,876

2006

3,547

$1,120,000

2007

3,120

$1,182,500

But still no surge here locally in 2019.

Our inventory count this year is looking normal – and 24% under the 2006 count:

NSDCC Detached-Home Listings Jan 1 to June 30:

Year

Number of Listings

Median List Price

2013

2,790

$1,179,000

2014

2,713

$1,120,000

2015

2,871

$1,182,500

2016

2,999

$1,425,000

2017

2,712

$1,425,000

2018

2,700

$1,499,000

2019

2,705

$1,569,000

In the first half of 2005, we had 400 sales close under $750,000, and this year we had 55.

We had 560 homes list for $2,000,000+ in the first half of 2005, and 238 closings. This year, we had 901 listings over $2,000,000, and 298 closings!