I don’t care what color he’s seeing, if he sells his tony golf-course estate today and thinks he will buy it back later for less, he will be in for a rude awakening. Without foreclosures (now mostly outlawed in California) causing banks to give away homes, there won’t be any more downturns or cycles. But for those who agree with him, yes – please sell!

Bond manager Mark Kiesel sold his California home in 2006, when he presciently predicted the housing bubble would pop. He bought again in 2012, after U.S. prices fell more than 30% and found a floor.

Now, after a record surge in prices, Kiesel says the time to sell is once again at hand.

Sky-high values, soaring interest rates and other costs of homeownership — maintenance, property taxes and utilities — dampen prospects for future appreciation, according to Kiesel, chief investment officer for global credit at Pacific Investment Management Co. He’s weighing putting his Orange County house on the market and becoming a renter rather than an owner.

“I can look at my long-term 25-year charts and they tell me when to buy and sell and they’re flashing orange right now,” Kiesel, 52, said during an interview at Pimco’s Newport Beach, California, headquarters. “I think we’re in the final innings.”

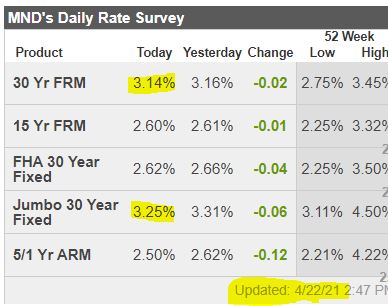

Home prices soared almost 20% in the 12 months through February, according to the S&P CoreLogic Case-Shiller Index, as pandemic moves, low borrowing costs and a dearth of inventory spurred heated competition for housing. But the market is now facing the fastest rise in mortgage rates in decades as the Federal Reserve works to tamp down inflation. The average 30-year rate is now 5.1%, close to a 12-year high, Freddie Mac data show.

Home sales contracts, a leading indicator, fell for the fifth consecutive month in March as rising borrowing costs added to affordability pressures, the National Association of Realtors reported on Wednesday.

Kiesel’s possible sale is a personal move and not a forecast of a crash by Pimco, which in March put out a note predicting “No Bust After the Boom” following years of housing undersupply. “Estimates of this secular shortage range from two to five million houses,” according to the authors.

But Kiesel’s past personal decisions have proved prophetic.

He sold his Newport Beach house in May 2006, calling housing “the next Nasdaq bubble.” Home prices peaked that year before going on to plunge, triggering the global financial crisis.

“It’s not just houses that will be for sale,” Kiesel said in a June 2006 interview. “You’re going to see financial assets for sale over time, and ultimately corporate bonds.”

Then in May 2012, Kiesel decided it was time to own again, buying a golf course-adjacent home.

“For those of you renting or on the sidelines, I recommend you at least consider getting ‘back in’ and buying a house,” he wrote in a credit market note. “The future is hard to predict, but U.S. housing is healing and is probably close to a bottom.”

U.S. housing prices have more than doubled in the past decade and the house Kiesel bought for $2.9 million in 2012 now has an estimated value of $5.5 million, according to Redfin Corp.

Buying a home in today’s market would likely yield about a 2% return, Kiesel said. He considers his home as an investment, refusing to form an emotional attachment to his property.

“It’s only a good investment if you buy it the right time,” he said. “If I were to buy a house today, I would probably get max 2% return on it. And I can find other things I can make money on other than a house.”

When people are looking for the perfect ‘forever’ home that will last them for a lifetime, any additional cost isn’t going to phase them – or at least it won’t affect the affluent folks. Most are making it up elsewhere when they sell their previous home or rental properties, inherit big money or receive a gift, and/or sell their businesses/stocks or other assets and just want a trophy property.

If they weren’t bothered by home prices rising 60% to 80% over the last two years, a measly 2% increase in the mortgage rate isn’t going to stop them.

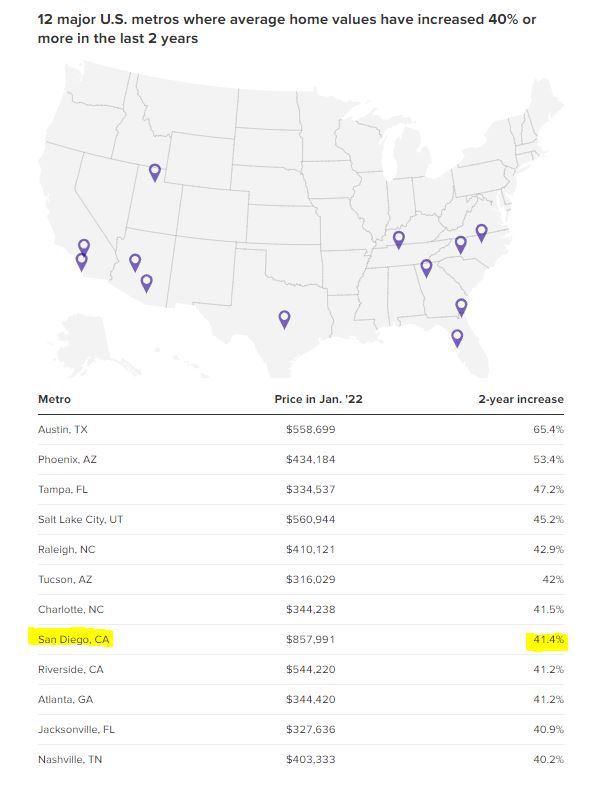

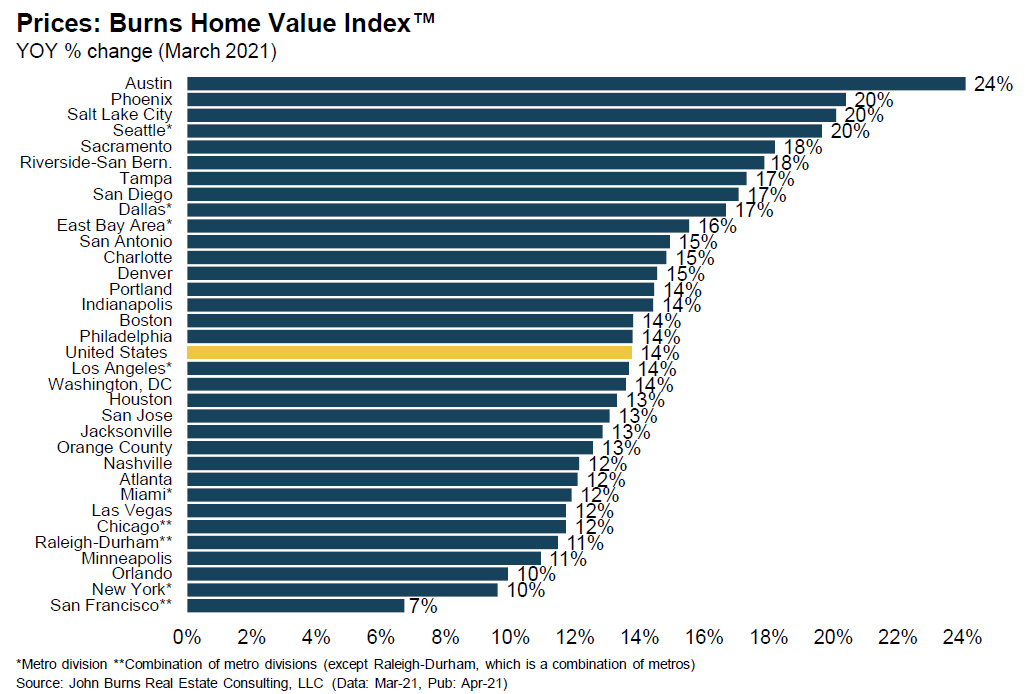

Sure all the California-feeder towns have risen 40% to 50%, but look at those price points! You don’t see any other city on this list with home prices as high as ours.

Of all the areas in the country, San Diego has to be one of the best places to live – and the affluent who can live anywhere have to be considering San Diego as one of their top choices.

But nobody wants to leave! We are currently offering millions of dollars to long-time homeowners to get them to move, and it’s not working! The supply and demand has never been so out of balance.

Eventually, we could have the highest home prices in the country!

The San Diego housing market is a popular choice for those who are leaving the Bay Area (population of 6,404,512 in the five counties). It’s looks like more are coming – a report from sfgate:

Joint Venture Silicon Valley, in partnership with the Bay Area News Group, polled 1,610 registered voters across five Bay Area counties: Alameda, Contra Costa, San Francisco, San Mateo and Santa Clara.

A shocking 71% of respondents said the quality of life in the greater Bay Area is worse now compared to five years ago. Fifty-six percent of respondents said they are considering leaving in the next five years — including 53% of respondents who work in the tech sector.

“It’s the cost of living, high housing costs. I think that is the dominant thing. It’s housing housing housing,” said Russell Hancock, President and CEO of Joint Venture Silicon Valley, in a press briefing. “…That is driving almost all of the results.”

Hancock said the 53% figure is the highest percentage of people who have said they want to leave the Bay Area compared to previous polls conducted outside of Joint Venture.

Indeed, an overwhelming majority of respondents said it’s high housing costs (77%) and cost of living (84%) spurring their desire to seek out greener pastures. Homelessness, wildfires and drought were also issues respondents considered when mulling the decision to leave the Bay Area.

“We’ve long been a high-stress region. Staggering housing prices, rising homelessness, a stark income divide and a host of sustainability challenges have had us on edge for some time,” Hancock writes in the introduction to the poll. “But when you toss a highly infectious disease into the mix you get a smothering amount of anxiety.”

But as Hancock noted, these feelings go beyond the pandemic and its challenges.

“We’re split (48% to 52%) on whether the Bay Area is headed in the right direction,” he said.

The poll paints a disturbing picture of life in the Bay Area, but it’s not all doom and gloom. About 65% of respondents said “they feel a strong sense of belonging to the Bay Area” — even more so than they feel connected to their neighborhood and city. Many (66%) applauded their employers’ response to the pandemic and now feel differently about their work-life balance.

As Hancock pointed out in the briefing, polls “tell us how people are thinking. And that’s worth knowing.”

“Perception,” he added, “is also a form of reality.”

If there were 56% of their population who left, it would equal 3,586,526 people – which would create a whole new experience for those who stay! But we know that talk is cheap, and once all the other variables are considered, most people don’t move.

But we’ll probably get a steady flow for the foreseeable future.

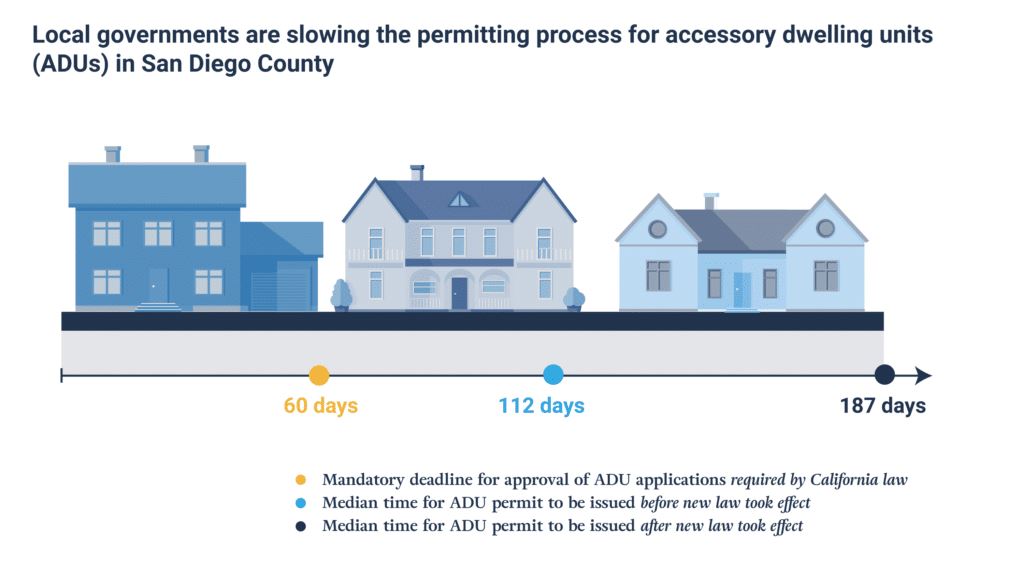

Pacific Legal Foundation obtained public records from San Diego and Riverside Counties (two of the most populous counties in the state) to determine whether local governments are abiding by the new 60-day permit-approval period, which took effect in January 2020.

Unfortunately for California residents, local governments are failing miserably to abide by the new state law.

San Diego County took a median of 187 days to issue an ADU or Junior ADU building permit after January 2020. Permits issued prior to the new law took a median of 112 days to be issued. Only 52% of permits issued prior to the new law fell within the previously required 120-day mark.

Currently, only 5% of permits issued by the county met the state’s 60-day deadline. Many times, the permitting process is held up by excessive fees or approvals needed from other departments within the county. As of July 21, 2021, there are 587 pending applications, of which 90 were submitted prior to 2020. If these permits were issued today, the median wait time would be 255 days after the application was submitted.

The government, and society in general, needs to recognize how dire the housing crisis is for the citizens. We’re going to have continued upward pressure on home prices and rents, and building ADUs is one of the best ways to alleviate the problem. It doesn’t matter if the resistance by local governments is conscious or sub-conscious, the ADU-approval process needs to improve radically to implement the will of the people, and slow down prices.

Shiller has been too conservative on his predictions because he’s an ivory-tower guy. If he were to talk to potential home sellers, he’d find that there aren’t many – if any – who have to move so badly that they would sell for “substantially lower” prices. The next phase after the frenzy will be the stagnant/plateau stage where the demand thins out and sellers wait for that perfect nuclear family with 2.2 kids to come along some day.

Nobel prize-winning economist Robert Shiller is worried a bubble is forming in some of the market’s hottest trades. He’s notably concerned about housing, stocks and cryptocurrencies, where he sees a “Wild West” mentality among investors.

“We have a lot of upward momentum now. So, waiting a year probably won’t bring house prices down,” Shiller said.

According to Shiller, current home price action is also reminiscent of 2003, two years before the slide began. He notes the dip happened gradually and ultimately crashed around the 2008 financial crisis.

“If you go out three or five years, I could imagine they’d [prices] be substantially lower than they are now, and maybe that’s a good thing,” he added. “Not from the standpoint of a homeowner, but it’s from the standpoint of a prospective homeowner. It’s a good thing. If we have more houses, we’re better off.”

Mortgage rates have settled down nicely, and are back in the high-2s for those home buyers who don’t mind paying a half-point or so (those quoted above are with zero points paid).

Not sure that it matters. Not sure that anything matters any more.

I had a great conversation with a top Compass agent today discussing the market conditions.

Specifically, what do you tell buyers?

Thankfully, the market is so hot that we have more sales to rely on. Even with the prices going up, at least there are a few recent sales nearby that help to substantiate the trend.

Is adding 1% per month to pricing enough to keep up with the actual? 1.5%?

Or how about 2.0% per month in the quality mid-range markets, both local and national?

With the rollout of vaccines against COVID-19, 70% of homeowners in a recent Zillow survey say they would feel mostly or completely comfortable moving to a new home when vaccines are widely distributed — and 78% of homeowners who say widespread vaccine distribution would impact their decision to move say such distribution would makes them more likely to move.

“We expect that the vaccine rollout will likely boost inventory, as sellers become increasingly willing to move despite COVID-19 — resulting in greater numbers of new listings beginning this spring,” says Chris Glynn, principal economist at Zillow. “That injection of inventory could give buyers more options and breathing room in a competitive market. The vaccine, however, will also likely add to already-strong demand, given that most sellers will become buyers as they trade in for a home that better suits their new needs.”

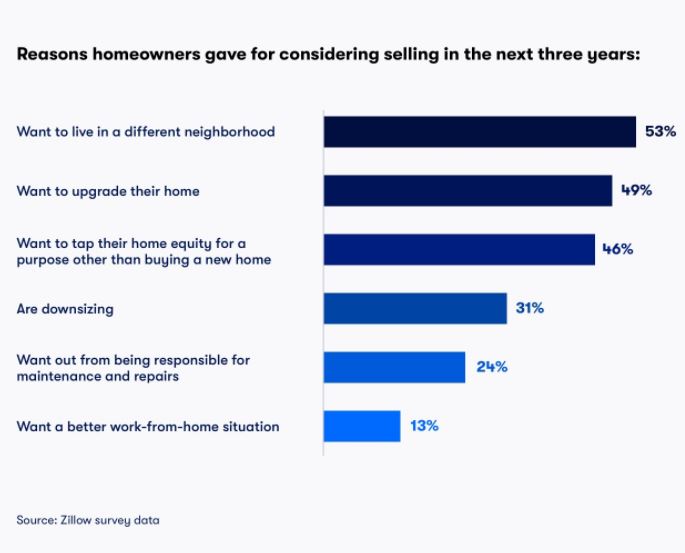

Zillow research shows that 63% of sellers are also buyers. And, as buyers, they have specific reasons for selling. A recent Zillow survey shows that homeowners who are thinking of selling in the next three years have a variety of reasons for doing so.

Additionally, 26% want to live closer to family, 24% wanted out from being responsible for yard work, 14% say their family or household is getting larger and 13% say they can no longer afford their home.

Nearly 40% of homeowners who are considering selling within three years (39%) say they think they’ll get a better price if they wait. They’re not necessarily wrong — although waiting comes with tradeoffs, according to Zillow economist Jeff Tucker.

“Potential sellers are likely correct that home prices have yet to reach their peak,’’ Tucker said, “but in the long run prices tend to rise, so there’s no clear ‘right time’ to sell.”

The catch, he said, is that waiting to sell may raise the cost of trading up to their next home if mortgage interest rates rise.