We saw this happen in Bressi Ranch when Jenae and Company went on their 100% financing spree. Her victims weren’t deadbeats – instead, they had good credit scores and other assets, and they were just duped into the get-rich-quick scheme. When it didn’t pan out, they dumped everything.

The grim tale of America’s “subprime mortgage crisis” delivers one of those stinging moral slaps that Americans seem to favor in their histories. Poor people were reckless and stupid, banks got greedy. Layer in some Wall Street dark arts, and there you have it: a global financial crisis.

Dark arts notwithstanding, that’s not what really happened, though.

Mounting evidence suggests that the notion that the 2007 crash happened because people with shoddy credit borrowed to buy houses they couldn’t afford is just plain wrong. The latest comes in a new NBER working paper arguing that it was wealthy or middle-class house-flipping speculators who blew up the bubble to cataclysmic proportions, and then wrecked local housing markets when they defaulted en masse.

Analyzing a huge dataset of anonymous credit scores from Equifax, a credit reporting bureau, the economists—Stefania Albanesi of the University of Pittsburgh, the University of Geneva’s Giacomo De Giorgi, and Jaromir Nosal of Boston College—found that the biggest growth of mortgage debt during the housing boom came from those with credit scores in the middle and top of the credit score distribution—and that these borrowers accounted for a disproportionate share of defaults.

As for those with low credit scores—the “subprime” borrowers who supposedly caused the crisis—their borrowing stayed virtually constant throughout the boom. And while it’s true that these types of borrowers usually default at relatively higher rates, they didn’tafter the 2007 housing collapse. The lowest quartile in the credit score distribution accounted for 70% of foreclosures during the boom years, falling to just 35% during the crisis.

So why were relatively wealthier folks borrowing so much?

Recall that back then the mantra was that housing prices would keep rising forever. Since owning a home is one of the best ways to build wealth in America, most of those with sterling credit already did. Low rates encouraged some of them to parlay their credit pedigree and growing existing home value into mortgages for additional homes. Some of these were long-term purchases (e.g. vacation homes, homes held for rental income). But as a Federal Reserve Bank of New York report from 2011 reveals (pdf, p.26), an increasing share bought with the aim to “flip” the home a few months or years later for a tidy profit.

As she was getting on in years and her resources dwindled, Virginia Rayford took out a special kind of mortgage in 2008 that she hoped would help her stay in her three-bedroom Washington rowhouse for the rest of her life.

Rayford, 92, took advantage of a federally insured loan called a reverse mortgage that allows cash-strapped seniors to borrow against the equity in their houses that has built up over decades.

But the risks of the financial arrangement are stark — and today the frail widow finds herself facing foreclosure.

Under the terms of the loan, Rayford can defer paying back her mortgage debt that totals about $416,000 until she dies, sells or moves out. She is, however, responsible for keeping up with other charges — namely, the taxes and insurance on the property.

The loan servicer, Nationstar Mortgage, says Rayford owes $6,004 in unpaid taxes and insurance. If she cannot come up with it, she stands to lose her home in Washington’s Petworth neighborhood.

“I’ve cried a million nights wondering about where I am going to be,’’ Rayford said.

In what has to be one of the most bizarre developments in real estate this year, the ivory-tower folks at the Fed, of all people, dreamed up a creative new loan that would not require a down payment. Then they used the dreaded COFI term from neg-am mortgage days! No word on when these might be available, if ever:

Abstract: The 30-year fixed-rate fully amortizing mortgage (or “traditional fixed-rate mortgage”) was a substantial innovation when first developed during the Great Depression. However, it has three major flaws. First, because homeowner equity accumulates slowly during the first decade, homeowners are essentially renting their homes from lenders. With so little equity accumulation, many lenders require large down payments. Second, in each monthly mortgage payment, homeowners substantially compensate capital markets investors for the ability to prepay. The homeowner might have better uses for this money. Third, refinancing mortgages is often very costly.

We propose a new fixed-rate mortgage, called the Fixed-Payment-COFI mortgage (or “Fixed-COFI mortgage”), that resolves these three flaws.

This mortgage has fixed monthly payments equal to payments for traditional fixed-rate mortgages and no down payment. Also, unlike traditional fixed-rate mortgages, Fixed-COFI mortgages do not bundle mortgage financing with compensation paid to capital markets investors for bearing prepayment risks; instead, this money is directed toward purchasing the home. The Fixed-COFI mortgage exploits the often-present prepayment-risk wedge between the fixed-rate mortgage rate and the estimated cost of funds index (COFI) mortgage rate.

Committing to a savings program based on the difference between fixed-rate mortgage payments and payments based on COFI plus a margin, the homeowner uses this wedge to accumulate home equity quickly. In addition, the Fixed-COFI mortgage is a highly profitable asset for many mortgage lenders. Fixed-COFI mortgages may help some renters gain access to homeownership. These renters may be, for example, paying rents as high as comparable mortgage payments in high-cost metropolitan areas but do not have enough savings for a down payment. The Fixed-COFI mortgage may help such renters, among others, purchase homes.

Keywords: COFI, Cost of funds, Financial institutions, Fixed-rate mortgage, Homeownership, Interest rates, Mortgages and credit

JtR: This sounds like the reverse of a neg-am mortgage, or a positive-amortizing loan where borrowers have a fixed payment as a ceiling, and then when rates float down, the difference is applied to the principal. But how much potential is there for your rate to drop when we’re at all-time lows? Maybe they are preparing a loan option for the day that rates rise substantially?

The impact of losing the mortgage-interest deduction has been blown out of proportion by NAR lobbyists. Let’s tinker with it now when rates are low and see if lower taxes could spur additional demand.

There may be rumblings about lowering the cap on mortgage interest rate deductions, but it would have a “rather small effect” on the housing market, Nobel Prize-winning economist Robert Shiller told CNBC on Wednesday.

The popular deduction is “limited to a small percent of taxpayers. It’s just not that big an effect compared to the big things,” the Yale economics professor said in an interview with “Power Lunch.”

“What’s really driving the real estate market is our sense of where we’re going and the uncertainty at the time with the new administration in Washington and all this talk.”

For example, things like the deadly white supremacist rally in Charlottesville, Virginia, slows down people’s willingness to make a big financial transaction, noted Shiller, who co-founded the Case-Shiller index.

The mortgage interest deduction enables homeowners to deduct the interest paid on their home loans from their income taxes. It is currently capped at loans up to $1 million for married couples filing jointly. The cap is $500,000 for those filing separately.

Industry sources have told CNBC that reducing the deduction is on the negotiating table as Republicans work to hammer out a tax reform package.

However, most homeowners don’t claim the deduction and instead use the standard deduction, Shiller said. Therefore, he believes lowering the cap would have more of a psychological effect on home prices than a calculated one.

“This is part of American culture. It goes back to the American dream,” he said. “It stands for something. It stands for ‘the government is behind the homeowner.’ It’s a political thing.”

Freddie Mac announced Friday it is making buying a home a better experience for lender and homebuyers – by cutting the appraiser out of the process.

The company is now offering a new product which will cut the appraisal process out of qualified home purchases and refinances. This could save borrowers an estimated $500 in fees and could reduce closing times by as much as 10 days.

The new Automated Collateral Evaluation assesses the need for a traditional appraisal by using proprietary models and utilizing data from multiple listing services and public records as well as the historical home values in order to determine collateral risks.

“By leveraging big data and advanced analytics, as well as 40+ years of historical data, we’re cutting costs and speeding up the closing process for borrowers,” said David Lowman, Freddie Mac executive vice president of single-family business.

“At the same time, we’re providing immediate collateral representation and warranty relief to lenders,” Lowman said. “This is just one example of how we are reimagining the mortgage process to create a better experience for consumers and lenders.”

Lenders can determine if a property is eligible for ACE by submitting the data through Freddie’s loan product advisor. This will then assess credit, capacity and collateral to determine the quality of the loan. Lenders will receive the risk assessment feedback in real time.

ACE will be available for home purchases beginning on September 1, 2017.

Earlier this summer, the company announced it began using this product on qualified refis beginning June 19, 2017.

“When we launched loan advisor suite in July 2016, we set out to give our customers certainty, usability, reliability and efficiency,” said Andy Higginbotham, senior vice president of strategic delivery and operations for Freddie Mac’s single-family business. “ACE is our most recent capability to deliver on that vision.”

Fannie Mae also updated its policy on appraisals this year, and clarified its “existing policy that allows an unlicensed or uncertified appraiser, or an appraiser trainee to complete the property inspection. When the unlicensed or uncertified appraiser or appraiser trainee completes the property inspection, the supervisory appraiser is not required to also inspect the property.”

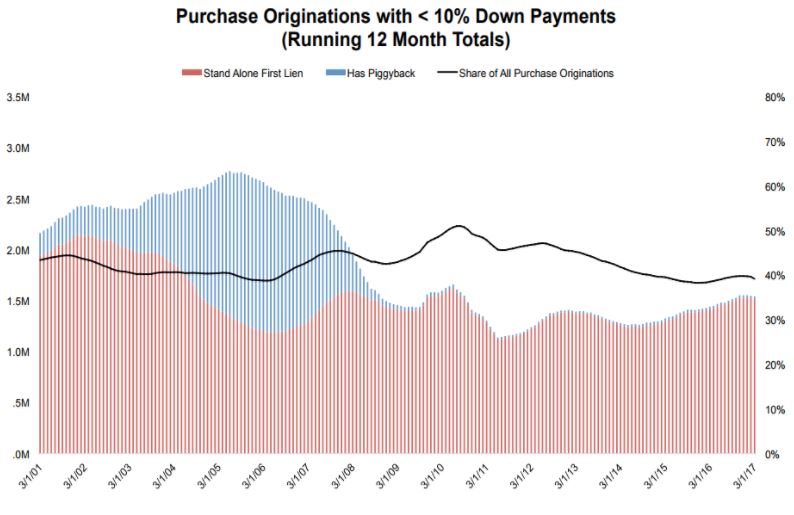

It’s hard to lower the down payment on a jumbo loan so any effect on the coastal regions is probably minimal, but this suggests that the stronger buyers are giving way or running out:

This month, in light of much commentary and speculation on the re-emergence of purchase loans with loan-to-value (LTV) ratios of 97 percent or higher, Black Knight looked at low-down-payment purchase lending trends, gaining some early insight into the performance of these products. As Black Knight Data & Analytics Executive Vice President Ben Graboske explained, in general, low-down-payment purchases are on the rise, but this does not necessarily mean a return to the practices – and risks – of the past.

“Over the past 12 months, approximately 1.5 million borrowers have purchased homes using less-than-10-percent down payments,” said Graboske. “That is close to a seven-year high in low-down-payment purchase volumes. The increase is primarily a function of the overall growth in purchase lending, but, after nearly four consecutive years of declines, low-down-payment loans have ticked upwards in market share over the past 18 months as well. In fact, they now account for nearly 40 percent of all purchase lending.

The bulk of the growth has not been among the various three-percent-or-less down payment programs that have been reintroduced in the last few years, but rather in five-to-nine- percent down payment mortgages. This segment grew at twice the rate of the overall purchase market in late 2016, whereas lending with down payments of less than five percent grew at about the market average.

The Wall Street Journal published this article about the mortgage-interest deduction having little – or no – impact on the decisions made by homebuyers:

Of course, the N.A.R., who is beholden to our lobbyists, refuses to consider any changes. The N.A.R. spent $64,821,111 last year on lobbying – we should quit paying them and spend that money on a rocking real estate portal that benefits all realtors!

Instead, our beleaguered president shuffled up to the podium one more time to vomit the usual beliefs, whether true or not:

The mortgage interest deduction, backed by the influential nationwide lobbying of real-estate agents and home builders warning against precipitous price drops, has survived decades of attacks and is extremely unlikely to vanish this year.

William Brown, president of the National Association of Realtors, said that removing incentives for homeownership, including the mortgage interest deduction, would be a mistake.

“Studies comparing our housing market to that of a foreign country offer an apples-to-oranges scenario that often isn’t constructive,” Mr. Brown said in a statement. “What we know for sure is that home values would suffer if the mortgage interest deduction disappeared, potentially putting homeowners under water.”

Curbing the deduction would give cash buyers an advantage, said Robert Dietz, chief economist at the National Association of Home Builders.

President Donald Trump has promised to protect the mortgage interest deduction. But even under the plans from Mr. Trump and congressional Republicans, the deduction could lose some of its punch.

With mortgage rates so low, the actual benefit isn’t what it used to be. In addition, wouldn’t rising rents and getting rich quick be bigger motivators than the MID? Have you noticed that you never hear banks arguing for the MID?

Mortgage rates fell convincingly today, though not all lenders adjusted rates sheets in proportion to the gains seen in bond markets (which underlie rate movement). Those gains came early, with this morning’s economic data coming in much weaker than expected. Markets were especially sensitive to the Consumer Price Index (an inflation report) which showed core annual inflation at 1.7% versus a median forecast of 1.9%.

Core annual inflation under 2.0% is a hot topic–especially today–considering that’s one of the Fed’s main goals. This afternoon’s Fed Announcement did acknowledge the recent drop in inflation, but continued to suggest it was being held down by temporary factors. The Fed also officially unveiled its framework for decreasing the amount of bonds its buying (though it didn’t announce a start to the program yet).

Bottom line: Fed bond buying is one of the reasons rates are as low as they are. Markets know the Fed will eventually enact this plan and they’ve accounted for that to the best of their ability. But as the Fed actually goes through the steps toward enacting the plan, it causes some upward pressure for rates. That was the case this afternoon, but bond markets were nonetheless able to hold on to a majority of improvement seen this morning. As such, the day ended with most lenders offering their lowest rates in exactly 8 months (a few days following the presidential election).

Those with less skin in the game are typically the people who have the most trouble in a down market. Apparently, the potential profit must be so large that the investors overlook that – or figure there is little chance the government will let the market go down again?

Several years after her divorce, Tricia DeWaal was still living in the 3,200-square-foot home where she’d raised her children. When her youngest moved out, DeWaal knew it was time to downsize.

“For what I wanted, I had a 20% down payment, but that would pretty much clean me out in terms of cash,” DeWaal told MarketWatch. “I wanted to have some backup.”

After lots of online research, DeWaal came across a company called Unison, which had an intriguing sales pitch. The company’s home-buyer program offers buyers money for a down payment in exchange for a share of equity in the home, to be paid back when the owner sells.

DeWaal had what she called a “very positive experience.” “It’s definitely a good thing for somebody who’s trying to afford a certain amount that they can’t quite get to,” she said.

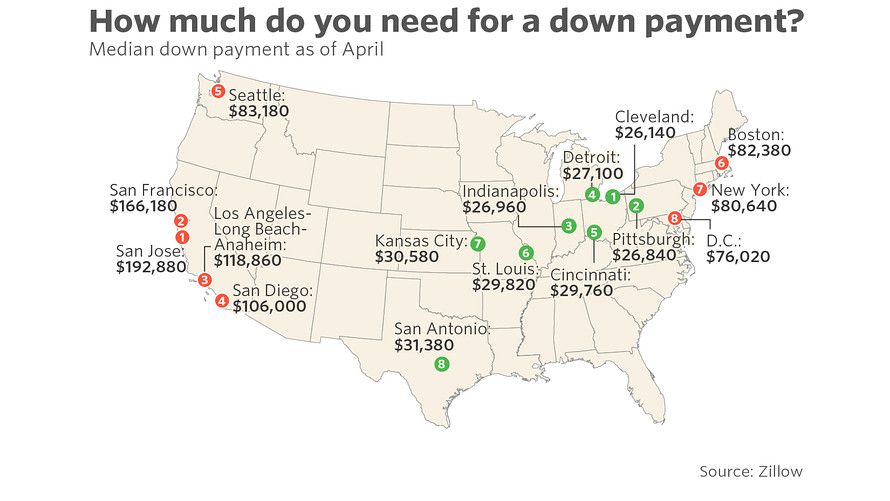

Homeownership’s biggest barrier to entry, the down payment, looms larger and larger all across the country. Student debt payments and high rents are formidable barriers to saving, and, while there are plenty of ways to buy a home with less than 20% down, all require some form of mortgage insurance, making them more expensive.

For a long time, nonprofits have tried to help home buyers up and over the hurdle. But in today’s tight market and constrained lending environment, fintech companies are seeing an opportunity as well, particularly in the hottest housing markets, where 20% down can mean six figures.

Unison and a competitor, OWN Home Finance, which is set to launch a similar product later this year, got started years ago with a slightly different business model: allowing homeowners with high levels of accrued equity a means of tapping into that money.

Here’s how Unison’s model works: The company contributes up to 50% of the down payment, or 10% of the total cost of the home, and, then, when the owner sells, Unison takes a share of the profit, usually 35% — or a share of the loss, also usually 35%.

For many housing market observers, the idea makes a lot of sense.

“I love to see the experiment,” Brett Theodos, a senior research associate at the Urban Institute, told MarketWatch. “It’s really intriguing as home prices appreciate and incomes don’t. It feels like a missing rung in the ladder between renting and owning. We have so many investment vehicles that you can get into for small amounts of money, but homeownership is very much an all-or-nothing proposition.”

Still, with programs like these, according to Theodos and other experts, the devil is in the details.