Reverse Mortgages

A great introduction by the reverse-mortgage guy Dean Jones (who can be reached at 760-458-2755). Basically with FHA you can borrow $300,000 to $400,000 depending on your age, and with his non-FHA portfolio loan it’s a little more:

A great introduction by the reverse-mortgage guy Dean Jones (who can be reached at 760-458-2755). Basically with FHA you can borrow $300,000 to $400,000 depending on your age, and with his non-FHA portfolio loan it’s a little more:

Let’s get back to it! Thanks to SM for sending in the official FHFA news release about the conforming-loan limits being raised for 2020. The new limit in San Diego is $701,500.

This interactive map shows how America’s high real estate prices are isolated to just a few counties.

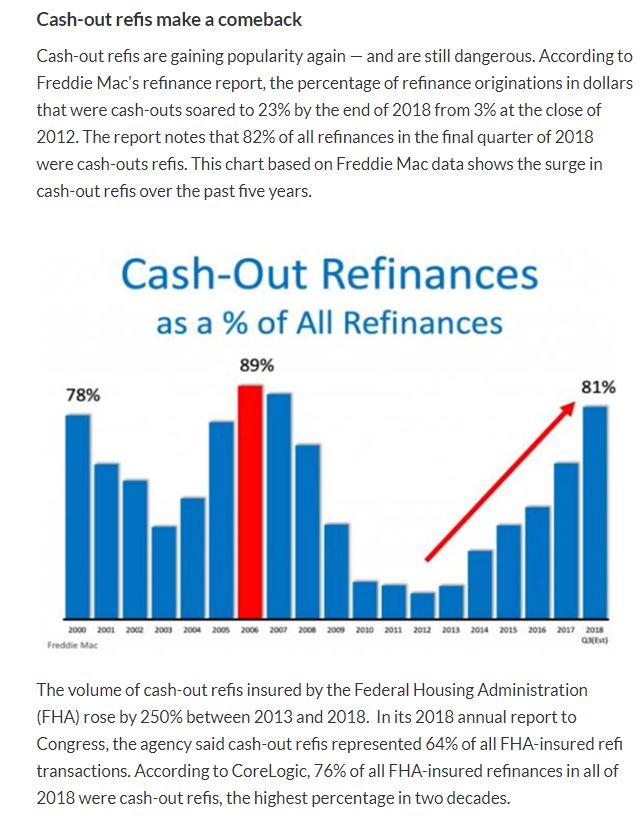

Low mortgage rates and large down payments are how buyers today are able to afford these lofty prices. Wondering where the big money comes from? Some of it could be from cash-out refinances:

The article has a couple of other zingers too – excerpts:

In recent years, wealthy homeowners have gotten into the cash-out refi game in a big way. A CoreLogic report in January 2019 found 230 active giant refinanced mortgages between $10 million and $20 million — most originated since 2013. Almost half of these loans were identified as cash-out refis. The average amount of cash pulled out was $6.6 million. Last year, the average had risen to $8.3 million.

Almost 10 million cash-out refis were originated during the wildest bubble years of 2004–07. While a significant number of them have been foreclosed, most still have not. As I noted in a previous column, mortgage servicers nationwide have been extremely reluctant to foreclose on long-term deadbeats since 2012.

Another column earlier this year laid out the enormous problem of modified mortgages that have re-defaulted one or more times. Close to two-thirds of all sub-prime bubble era mortgages had already been modified by 2015. The re-default disaster was so great that by mid-2010 there were more subprime modified mortgages re-defaulting than there were delinquent loans being foreclosed and liquidated by mortgage servicers.

The author is probably the biggest doomer on the beat. He called me once and insisted that I agree with him on his gloomy predictions, and when I wouldn’t, he hung up on me. But his articles here are a good reminder – whatever happened to those loan modifications?

Link to Full ArticleMore evidence of how are sales and pricing have been flat this year, in spite of lower rates:

NSDCC 3rd Quarter Sales

| Year | |||

| 2013 | |||

| 2014 | |||

| 2015 | |||

| 2016 | |||

| 2017 | |||

| 2018 | |||

| 2019 |

Rates have bumped up a quarter, and any action today by the Fed won’t change them much:

Sales, pricing, rates – all stagnant and just waiting around for buyers to find the right house – or price!

If you ever thought of firing off a lowball offer, November would be the month.

Did you know that mortgages sold to FHA, VA, Fannie and Freddie are allowed to exceed to the traditional 43% DTI (debt-to-income) ratio? The rule that allows it is known as the QM Patch, which expires in 2021. But bankers are fighting to keep the exemption from the 43% DTI ratio in place, and are playing the race card to make their point:

Four of the largest mortgage lenders in the country are leading a coalition that is calling on the Consumer Financial Protection Bureau to make to changes to the Ability to Repay/Qualified Mortgage rule.

Wells Fargo, Bank of America, Quicken Loans, and Caliber Home Loans joined with the Mortgage Bankers Association, the American Bankers Association, the National Fair Housing Alliance, and others to send a letter to the CFPB, asking the bureau to eliminate the 43% DTI cap on “prime and near-prime loans.”

“Elimination of the DTI requirement for prime and near-prime loans would preserve access to sustainable credit for the new generation of first-time homebuyers in a safe and sustainable way and in accordance with the fundamental ATR requirements,” the group writes.

“This change is especially important for reaching historically underserved borrowers, including low- to moderate-income households, and communities of color.”

Link to ArticleBecause the FHA reverse mortgages (HECM) have loan limits, are expensive, and got harder to obtain, the private reverse-mortgage market is growing. These can be used to buy a home too, and have no payments! Maybe the realtor disrupters will get into the reverse-mortgage business instead?

Borrowers of proprietary reverse mortgages are increasingly becoming more closely aligned with the typical profile of a Home Equity Conversion Mortgage (HECM) borrower, through two very identifiable attributes: loan amounts that are in-line with those of a more traditional HECM, and the use of a loan’s proceeds to consolidate and pay off existing debt of other types. This is according to data about borrowers of proprietary products from Reverse Mortgage Funding (RMF) in a webinar hosted last week by RMD.

“We’re getting a lot of borrowers who are not necessarily the ‘jumbo’ market over that max claim limit of a HECM,” said Craig Barnes, head of training and education at RMF in discussing the company’s Equity Elite proprietary reverse mortgage. “We’re doing a lot of loans for much less than that.”

While most proprietary reverse mortgages have maximum loan amounts of up to $4 million – including RMF’s Equity Elite – Barnes shared that some of the greater flexibility granted by proprietary products are attracting more borrowers that would previously have only been served by a traditional HECM.

“[Our typical borrower is] age 77, they have a home valued at $1.5 million. So, as I said, it’s not a super jumbo product,” Barnes describes. “With the change in max claims last year, really you have to get well above $1 million or so depending on a borrower’s age in order to maximize the HECM anyway. We just had one yesterday that was for $400,000.”

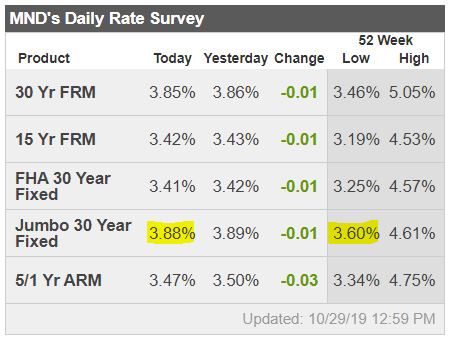

Hat tip to Matthew for a great piece on mortgage rates:

Mortgage rates have risen rather abruptly from their long term lows 2 weeks ago and are now at the highest levels in more than a month. Fortunately, the average lender is still easily able to quote rates in the high 3% range, which is still a significant savings for anyone who bought or refi’d in 2018 and even the first part of 2019.

That’s great and all, but what have rates done for us lately?

More importantly, what are rates going to do in the future?

Unlike forecasting the weather, the more of an expert someone is in the mortgage world, their ability to predict the direction of rates doesn’t meaningfully diverge from the layperson’s best guess. What we do know is that tomorrow’s Fed announcement is a big potential source of volatility, but NOT for the reasons most laypersons may assume!

I’m often asked if the Fed rate cut/hike will have an effect on mortgage rates. I’m also often asked to reiterate the correct answer to that question which is almost always “NO!”

The Fed only meets to potentially change rates 8 times a year. The bond market that underlies mortgage rates, however, can change 8 times in less than a second. Markets have LONG since priced in the Fed’s likely course of action (which is currently a high probability for a rate cut). If the Fed surprises markets and doesn’t cut rates, it will definitely cause some movement in financial markets, but there’s no telling where mortgage rates would be at the end of the day.

Part of the reason for that is the market’s bigger focus on the Fed’s updated forecasts. In other words, the (probable) rate cut is old news and has already been accounted for in today’s mortgage rate landscape. But if the Fed’s forecasts show deceleration in the pace of expected rate cuts versus the June forecasts, rates could rise.

A lot has happened since June, however, so it’s possible the forecasts will call for even lower rates over the next 3 years. Even if that happens, there’s still no telling what the reaction would be in longer-term rates like mortgages. After all, more rate cuts in 2019/2020 could act to keep the economic expansion going, and that’s bad for rates, all other things being equal.

The bottom line is that the Fed announcement is a multifaceted event that can move markets in different ways for different reasons, expected or otherwise. Investors burn the midnight oil trying to get ahead of the market reaction and surprises are still the rule. The safest bet is to be prepared for a reaction in either direction as opposed to crossing fingers for rates to move lower.

Loan Originator Perspective

Bonds continued to regain some of last week’s brutal losses today, and my pricing improved slightly. We’ll take whatever gains we can get prior to tomorrow’s FOMC statement. I don’t see us regaining our recent multi-year low rates anytime soon, so folks yearning for rates in low 3’s need to temper their expectations. Nothing wrong with locking here. – Ted Rood, Senior Originator

Did you hear that rates bumped up 1/4% in the last week?

It doesn’t take much!

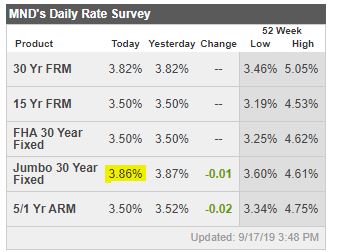

Doug Duncan, Fannie Mae chief economist, discusses if the rise in mortgage rates could help the housing market (causing those buyers on the margin to jump in quickly):

http://www.mortgagenewsdaily.com/video/archive/2019/9/16.aspx#921700

Aisling Swindell was paying so much for rent last year—$2,100 per month to live in a studio in Downtown LA—she figured she might as well buy a place.

“The house I ended up buying was $440,000, which is insane, right?” says Swindell, who works for an online fashion company.

That price tag, which is $178,000 below the median in LA County, sounds unbelievable, especially for what she bought: 870 square feet in the city, plus a little yard, lots of natural light, some stylish updates, and charming, 1930s-era details, like wainscoting and solid wood doors.

But while she’s no longer a renter, she still doesn’t, technically, own a house.

Her $440,000 bought her a share of a larger property: a triplex on an 8,344-square-foot lot in Jefferson Park. Her right to occupy the unit, and her responsibility for maintaining it, are spelled out in a contract with her neighbors, who live in the triplex and, with her, are its joint owners.

Read full article here:

https://la.curbed.com/2019/8/8/20751845/tenancy-in-common-los-angeles-rental-girl

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Are you thinking this would be a great way to sell your multi-unit building in San Diego?

I can help you with that!

Buyers can get mortgages up to $850,000 with a 10% down payment.

Contact me today at (858) 997-3801 or klingerealty@gmail.com.

Now we’re talking! Thanks Richard.

A bank in Denmark is offering borrowers mortgages at a negative interest rate, effectively paying its customers to borrow money for a house purchase.

Jyske Bank, Denmark’s third-largest bank, said this week that customers would now be able to take out a 10-year fixed-rate mortgage with an interest rate of -0.5%, meaning customers will pay back less than the amount they borrowed.

To put the -0.5% rate in simple terms: If you bought a house for $1 million and paid off your mortgage in full in 10 years, you would pay the bank back only $995,000.

It should be noted that even with a negative interest rate, banks often charge fees linked to the borrowing, which means homeowners could still pay back more.

According to The Local, Nordea Bank, Scandinavia’s biggest lender, said it would offer a 20-year fixed-rate mortgage with 0% interest. Bloomberg reported that some Danish lenders were offering 30-year mortgages at a 0.5% rate.

“It’s never been cheaper to borrow,” said Lise Nytoft Bergmann, the chief analyst at Nordea’s home finance unit in Denmark. It may seem counterintuitive for banks to lend out their money at such low rates – but there is a rationale behind it.

Financial markets are in a volatile, uncertain spot right now. Factors include the US-China trade war, Brexit, and a generalized economic slowdown across the world – and particularly in Europe.

Many investors fear a substantial crash in the near future. As such, some banks are willing to lend money at negative rates, accepting a small loss rather than risking a bigger loss by lending money at higher rates that customers cannot meet.

“It’s an uncomfortable thought that there are investors who are willing to lend money for 30 years and get just 0.5% in return,” Bergmann said.

“It shows how scared investors are of the current situation in the financial markets, and that they expect it to take a very long time before things improve.”

https://amp.businessinsider.com/danish-bank-offers-mortgages-at-negative-interest-rates-2019-8

Are you looking for an experienced agent to help you buy or sell a home?

Contact Jim the Realtor!

CA DRE #01527365, CA DRE #00873197