by Jim the Realtor | Aug 5, 2019 | Jim's Take on the Market, Mortgage News, Tax Reform, The Future, Tips, Advice & Links |

Maybe having a mortgage is going out of fashion now that the affluent have taken over real estate? Or do we just need to Get Good Help with filing taxes? (30%-40% of Americans prepare their own taxes)

The mortgage-interest deduction, a beloved tax break bound tightly to the American dream of homeownership, once seemed politically invincible. Then it nearly vanished in middle-class neighborhoods across the country, and it appears that hardly anyone noticed.

In places like Plainfield, a southwestern outpost in the area known locally as Chicagoland, the housing market is humming. The people selling and buying homes do not seem to care much that President Trump’s signature tax overhaul effectively, although indirectly, vaporized a longtime source of government support for homeowners and housing prices.

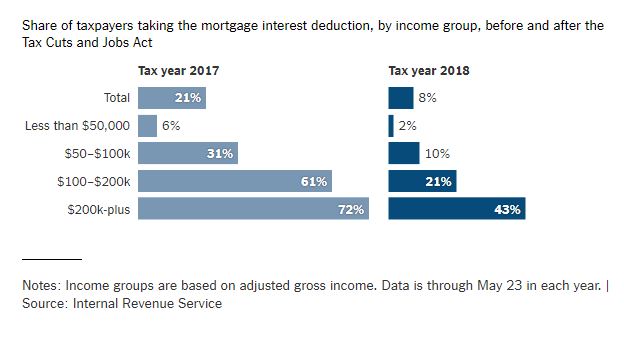

The 2017 law nearly doubled the standard deduction — to $24,000 for a couple filing jointly — on federal income taxes, giving millions of households an incentive to stop claiming itemized deductions.

As a result, far fewer families — and, in particular, far fewer middle-class families — are claiming the itemized deduction for mortgage interest. In 2018, about one in five taxpayers claimed the deduction, Internal Revenue Service statistics show. This year, that number fell to less than one in 10. For families earning less than $100,000, the decline was even more stark.

The benefit, as it remains, is largely for high earners, and more limited than it once was: The 2017 law capped the maximum value of new mortgage debt eligible for the deduction at $750,000, down from $1 million. There has been no audible public outcry, prompting some people in Washington to propose scrapping the tax break entirely.

For decades, the mortgage-interest deduction has been alternately hailed as a linchpin of support for homeownership (by the real estate industry) and reviled as a symbol of tax policy gone awry (by economists). What pretty much everyone agreed on, though, was that it was politically untouchable.

Nearly 30 million tax filers wrote off a collective $273 billion in mortgage interest in 2018. Repealing the deduction, the conventional wisdom presumed, would effectively mean raising taxes on millions of middle-class families spread across every congressional district. And if anyone were tempted to try, an army of real estate brokers, home builders and developers — and their lobbyists — were ready to rush to the deduction’s defense.

Now, critics of the deduction feel emboldened.

“The rejoinder was always, ‘Oh, but you’d never be able to get rid of the mortgage-interest deduction,’ but I certainly wouldn’t say never now,” said William G. Gale, an economist at the Brookings Institution and a former adviser to President George H.W. Bush. “It used to be that this was a middle-class birthright or something like that, but it’s kind of hard to argue that when only 8 percent of households are taking the deduction.”

Link to Full NYT Article

by Jim the Realtor | Jun 28, 2019 | Ethics, Jim's Take on the Market, Local Government, Market Buzz, Mortgage News |

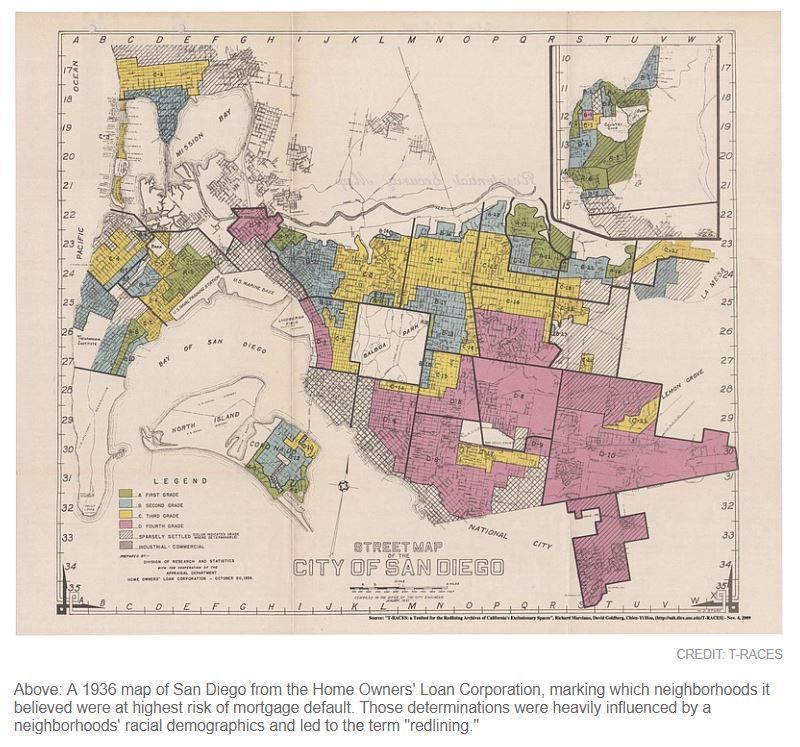

The history of housing discrimination is getting a lot of attention these days, and rightfully so. If you, or someone you know, wants to contribute, KPBS is looking for stories:

KPBS is doing an investigation into the legacy of “redlining” in San Diego.

This is the historic practice of excluding minorities from certain neighborhoods through regulations on mortgages, leases and home purchases. We’re looking into the impact this practice has had on the economic prosperity of different neighborhoods in San Diego.

Some families in San Diego may have benefitted from this history, through no fault of their own. Others may have been hurt by it.

If you or your family has any connection to this history, or if you know someone who does, please reply to this email or send an email to sources@kpbs.org with “Redlining” in the subject line.

Thank you for sharing your knowledge and becoming a trusted KPBS source!

There was actually a red zone in La Jolla around the Taco Stand on Pearl!

by Jim the Realtor | Jun 10, 2019 | Jim's Take on the Market, Mortgage News, Mortgage Qualifying

The latest easing of FHA underwriting, which usually means trouble – but don’t fear, they have ‘levers’:

Link to Article

Excerpts:

According to the FHA’s report for its fiscal second quarter (which covers Jan. 1 to March 31, 2019), the average credit score for an FHA borrower fell to 665 in the second quarter. That’s the lowest level since 2008, and is “well below” the FHA lending peak credit score of 703, which happened in 2011.

According to the FHA report, the share of 680–850 credit scores continues to decline among FHA borrowers, while lending to borrowers with credit scores below 640 continues to rise.

The FHA report shows that in 2011, nearly 60% of borrowers had credit scores above 680. Now, only 34% of FHA borrowers have credit scores above 680. Meanwhile, the share of FHA lending to borrowers with credit scores below 640 has increased to nearly 30%.

“This increase shows a much riskier population of mortgages being endorsed by FHA,” the report states. “Performance of these mortgages will be closely monitored to determine when policy changes should be implemented.”

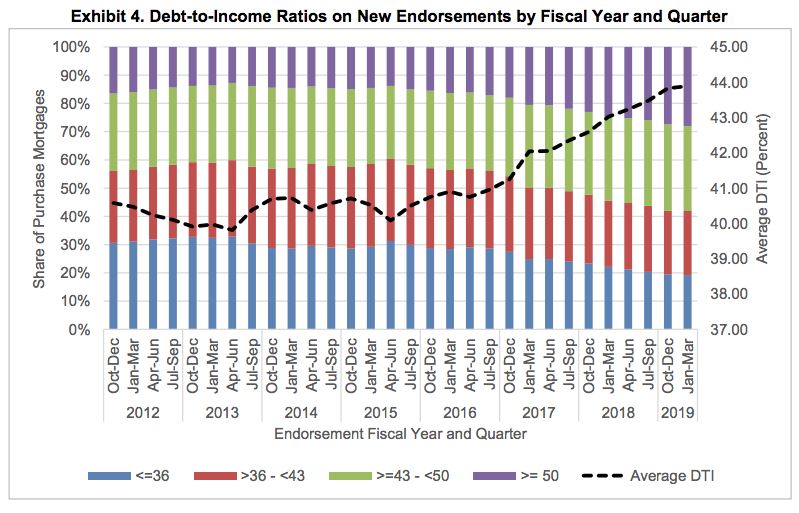

Beyond that, FHA loans have also seen a sharp increase among loans with high debt-to-income ratios, meaning borrowers are taking on more debt compared to their income level.

According to the FHA report, in 2018, nearly 25% of all FHA purchase mortgages had a DTI ratio above 50%. And that number has been rising for several years, a trend that FHA noted as concerning last year.

But despite noting that concern, the percentage of borrowers with DTIs above 50% continued increasing in the second quarter, climbing to 28% of all FHA purchase loans. According to the FHA, that’s the highest percentage of high-DTI loans in a single quarter since “at least the year 2000.”

The FHA notes in its report that this increase shows that its loans are getting riskier.

“This is a risk to the MMIF that the FHA is attempting to manage and mitigate through various policy levers,” the FHA said.

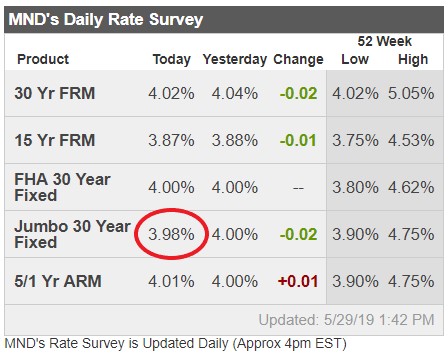

by Jim the Realtor | May 29, 2019 | Jim's Take on the Market, Market Buzz, Mortgage News |

If you are thinking about selling your house this year, call me tonight!

Rates are idyllic, and so is the weather which makes for a great combo!

Mortgage rates fell again today, just barely inching to the lowest levels since early 2018. Keep in mind, that factoid is based on an average of multiple lenders. Some of them aren’t quite back to the low rates seen at the end of March. Others had crossed that line several days ago. Either way, the actual NOTE RATE at the top of the average rate quote would be the same then and now. The EFFECTIVE RATE would be just slightly lower due to a small advantage in upfront lender costs.

Relative to market sentiment at the beginning of May, the last 3 weeks have been unexpected. In other words, there was no obvious reason to expect or fear the sort of slide in stocks and yields that we’ve seen since then. But of course, that’s just the sort of thing financial markets like to do! If there’s one overarching reason for the move, it’s the trade war between the US and China. Just when it seems the issue is put to bed, more drama unfolds. In general, trade war drama damages the economic outlook and a weaker economy is generally good for rates.

http://www.mortgagenewsdaily.com/consumer_rates/911637.aspx

by Jim the Realtor | Mar 18, 2019 | Jim's Take on the Market, Mortgage News

Those who pay their bills on time will cringe at how people can work the system successfully. Hat tip to SM who sent in this story told by a mortgage rep in Orange County:

My client had both a first and second mortgage on his Southern California home. He fell on hard times back around the Great Recession days. He filed for Chapter 7 bankruptcy in 2011.

Meanwhile, he got back on his feet income wise and credit wise. He made timely payments on the first trust deed, but never paid one penny of his remaining $250,000 second trust deed balance in eight years.

He contacted me about refinancing both his first and second loans into a single new loan. He also had negotiated a $140,000 reduction of the second. So, $250,000 owed turned into a $110,000 second mortgage payoff.

A very sharp underwriter looked more closely at the circumstances of this file. She was able to approve my client on a new Fannie Mae fixed-rate loan with a whopping $545 lower house payment because Fannie’s loan had an interest rate that was 1.875 percent lower than the non-prime loan we were seeking. Hallelujah!

It used to be that mortgage underwriting guidelines were absolutely against any borrower who was perceived as somehow stiffing the lender. In this instance, non-payment and a reduced payoff.

“I’m pleased to see a lightening of the guidelines,” said Susan Ashton, sales manager at Plaza Home Mortgage. “It’s really a positive thing.”

So, let’s dig a little deeper.

While bankruptcy discharge protects borrowers from having to reimburse lenders for missed house payments, it doesn’t protect them from foreclosure, according to Newport Beach bankruptcy attorney Michael Nicastro. Hence, borrowers typically continue to make their required house payments.

Mortgage lenders cannot demand payment on unpaid debts. So, post-bankruptcy, lenders do not report borrower late payments or delinquencies to credit bureaus.

Often the second mortgages are underwater — meaning the value of the house is less than the sum of the first, second, and accrued interest, etc. So, there is no point in foreclosing.

Those lenders typically sell the non-performing seconds for pennies on the dollar to what is known as “scratch-and-dent” investors. These scratch-and-dent investors hope to collect when the property value comes back.

Nicastro points out that the lender can send to the borrower a 1099-C (Cancellation of Debt), reporting the unpaid balance as income to the IRS.

“Check with your CPA,” Nicastro said. “If debt is canceled in bankruptcy, it’s possible that there is no taxable impact.”

Link to Article

by Jim the Realtor | Mar 9, 2019 | Jim's Take on the Market, Mortgage News, Open House, View, Why You Should List With Jim |

Wow – look at those jumbo rates with no points!

It would be a great day to buy the Best View in Carlsbad!

We’ll be open 12-3pm Saturday AND Sunday.

https://www.zillow.com/homedetails/4275-Clearview-Dr-Carlsbad-CA-92008/16649973_zpid/

by Jim the Realtor | Mar 7, 2019 | Jim's Take on the Market, Market Buzz, Mortgage News |

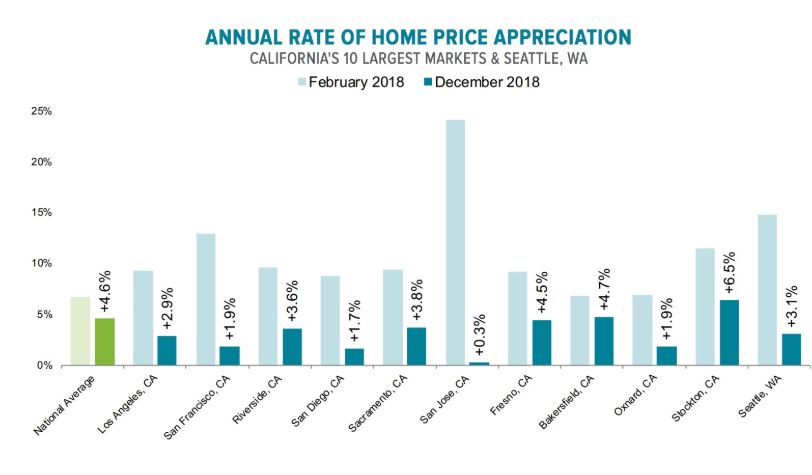

Appreciation is slowing down, and though it looks like San Diego slammed the brakes on between February and December last year, it’s nothing compared to San Jose where sellers went through the windshield, figuratively.

The year-over-year increase in our December Case-Shiller Index was +2.3%, and with Black Knight’s at 1.7%, let’s average and predict 2% appreciation for San Diego in 2019. It means 1/2% per quarter, which sounds pretty flat.

Earlier this week CoreLogic reported that the annual rate of appreciation in January, 4.2 percent, was exactly two-thirds the rate in January 2018. The Black Knight Mortgage Monitor essentially confirms that deceleration, reporting price increases dropping from 6.8 percent last February to 4.6 percent at year end.

Ben Graboske, president of Black Knight’s Data & Analytics division, explained that while home prices are still up year-over-year in all 50 states and the nation’s 100 largest markets, slowing is noticeable nationwide and – combined with recent interest rate reductions – is helping to improve the overall affordability outlook.

“At the end of December, home prices at the national level had fallen 0.3 percent from November for their fourth consecutive monthly decline,” he said. “As a result, the average home has lost more than $2,400 in value since the summer of 2018. And while home prices are still up on an annual basis, the slowdown continues nationwide and, importantly, is not being driven by seasonal effects. December marked the 10th straight month of slowing annual home price appreciation.”

He added, “With more than 50 percent of areas reporting, early numbers for January suggest we’re likely to see more of the same. That said, it’s important to keep in mind that annual growth is still outpacing the 25-year average of 3.9 percent – although the gap is closing quickly. Also, it’s yet to be seen what impact the recent pullback in interest rates may have on the national home price growth rate.

The slowdown has been especially apparent in the West. While some interior states are still seeing large gains – Nevada, Idaho, and Utah saw the greatest increases in the nation with Nevada still in the double digits – large metro areas on the coast have seen appreciation rates plummet.

Black Knight looked at the 10 largest markets in California and at Seattle and found that eight of them had seen their appreciation rate cut in half over the previous 10 months and by 70 percent in five of them. While prices in Washington State as a whole are still increasing by 5.7 percent, Seattle’s several year double digit run has evaporated. The annual rate is now 3.1 percent.

http://www.mortgagenewsdaily.com/03062019_black_knight_mortgage_monitor.asp

by Jim the Realtor | Feb 15, 2019 | Jim's Take on the Market, Mortgage News, Realtor |

Reader SM sent in this story on a mortgage company shutting down – and this one had a Carlsbad office:

https://www.ocregister.com/2019/02/14/provident-savings-bank-to-shutter-mortgage-banking-arm-cut-133-jobs/

Provident Savings Bank, the largest community bank in Riverside County, is discontinuing its mortgage banking operation, the company said in a statement.

The decision, announced by the bank’s board of directors Feb. 4, was based on a lack of profitability given the current financial environment. The operations are scheduled to cease on or before June 30.

Layoffs of 133 employees, of which 83 are in Riverside, were posted this week on the California WARN Act website, which requires layoffs to be publically reported. The others were at satellite offices in Brea, San Bernardino, Glendora, Carlsbad, Placer County and Northern California.

This one was even bigger:

https://www.housingwire.com/articles/48196-homestreet-bank-moves-to-sell-off-almost-entire-mortgage-business

HomeStreet announced Friday that it is planning to sell off its entire retail mortgage operation, which includes 72 home loan centers in five states, as well as nearly all of the mortgage servicing rights associated with loans originated in those retail outlets.

According to HomeStreet’s website, the company has 72 home loan centers: 37 in Washington, 16 in California, six in Hawaii, five in Idaho, and eight in Oregon.

According to the bank, it is making this move due to the “persistent challenges facing the mortgage banking industry.” The bank cites “the increasing interest rate environment,” which has reduced the demand for refinances, and higher home prices that have decreased the affordability of homes.

The mortgage business thrives on refinances in the ultra-low rate environment, but once rates rise, those refis dry up in a hurry.

A long-time local lender told me this week that two years ago there were 8,000 licensed mortgage originators in San Diego County, and today it’s 4,200!

We speculated that many of them became agents – another industry that is overdue for constriction. There are over 15,000 realtors in San Diego County, and last month we sold 1,770 houses, condos, and mobile homes countywide.

by Jim the Realtor | Feb 3, 2019 | Jim's Take on the Market, Mortgage News, Mortgage Qualifying

Everyone who is financing a home purchase should strongly consider the standard 30-year fixed-rate mortgage.

Though I recommend you move every 6 to 12 months (it’s good for business) these days most people are in it for the long-term. Even if you knew it wasn’t going to be a lifetime house, consider keeping it as a rental when you move.

But for those who have very strong income, or know they have an inheritance coming, a business or property to sell, or know their lucky Lottery numbers are going to pay off sooner or later, you may want to consider today’s version of exotic financing.

You should only take an alternative to the 30-year fixed rate if you had a solid plan to pay it off early. Don’t get an ARM thinking you’ll refinance someday, because it’s likely you’ll never get around to it – the fixed rate loan will have a higher payment, and you’ll shrug it off.

Here’s a choice today for mortgages up to $1,500,000:

3.875% fixed rate at 1.25 points, or

4.375% interest-only for ten years, no points.

Let’s say you want to finance $1,500,000:

The 30-year fixed option is $7,054 per month, and will cost $18,750 up front.

The ten-year ARM is $5,469 per month for ten years, with no points.

A benefit of the regular 30-year fixed-rate mortgage is the principal reduction every month – it’s a forced savings plan. After ten years, you will only owe $1,137,917, instead of the full $1,500,000 with the interest-only loan.

The ARM will feel like a fixed-rate loan with no payment change for ten years – which could lull you to sleep, and come back to haunt you 8-9 years from now.

Don’t take the 10-year deal just to get a lower payment. Take it because you know you have the ability to pay it off in the next ten years.

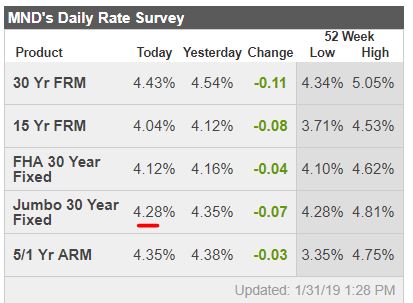

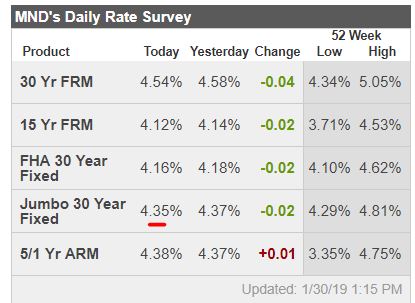

by Jim the Realtor | Jan 30, 2019 | Interest Rates/Loan Limits, Jim's Take on the Market, Mortgage News

Rates with no points

It sounds like mortgage rates will be rangebound for the foreseeable future, which is good for buyers – but not necessarily for sellers. Without the threat of rates going higher, buyers will be even more patient:

From MND:

It’s true that markets were already expecting a dovish Fed announcement. This created an asymmetric risk that the Fed would only be as friendly as they needed to be and that rates would have been positioned too low for such a thing. As it happened, however, the Fed was noticeably friendlier than most anyone guessed.

They dropped their verbiage pertaining to additional rate hikes. This effectively begins an era where rates will remain at current levels until economic data or other considerations motivate a change. Big news indeed!

They also dropped the reference to economic risks being balanced. The only way to be any friendlier to bonds would have been to say that economic risks had tilted to the downside (which can already be inferred from this change).

They also said they were prepared to adjust the balance sheet normalization policy if needed (i.e. they could start buying MBS again). Unsurprisingly, MBS liked this news and improved at a faster clip than 10yr Treasuries. Part of the 10yr’s problem was the big advantage the Fed’s announcement provided for shorter maturity Treasuries. In other words, traders were buying Treasuries, but most of the love went to the 2-5yr sector.

In the bigger picture, this is just another decently-sized green day for 10yr Treasuries, but reading between the lines, there’s a bit more to like. For MBS, it was easily the best day since January 4th. Not only that, but there’s a chance we look back at this as the day the Fed confirmed the end of the rising rate environment of the past 2 years. Granted, the past 2.5 months already did quite a bit in that regard, but it’s going to take a bit more time and stability to get comfortable with that idea.

Link to Article

Nice improvement today, and lowest in last 12 months – Jan 31st: