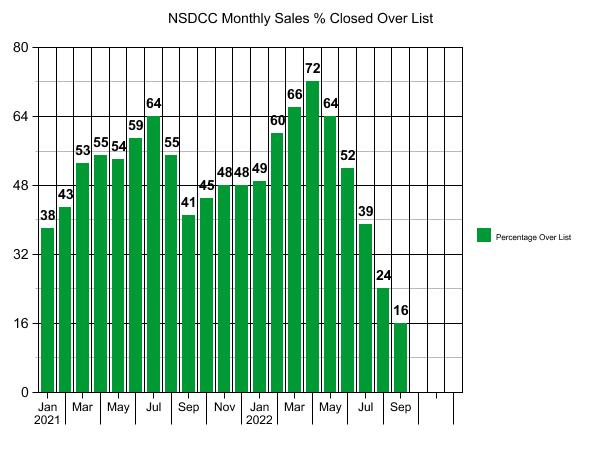

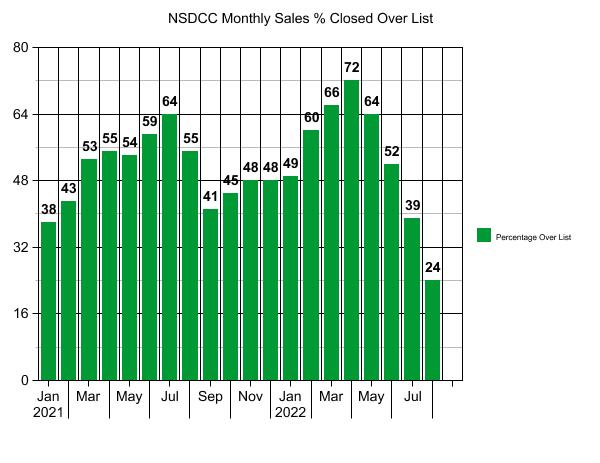

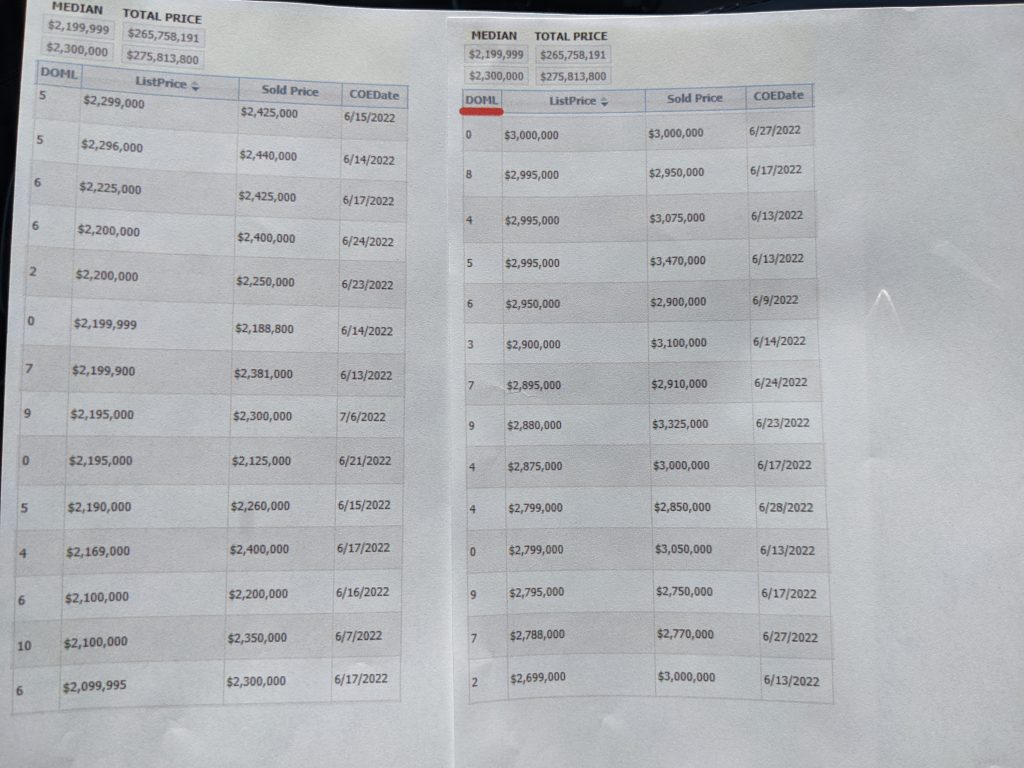

The number of December sales has been hanging right at 100 and ten closed above list, or 10%!

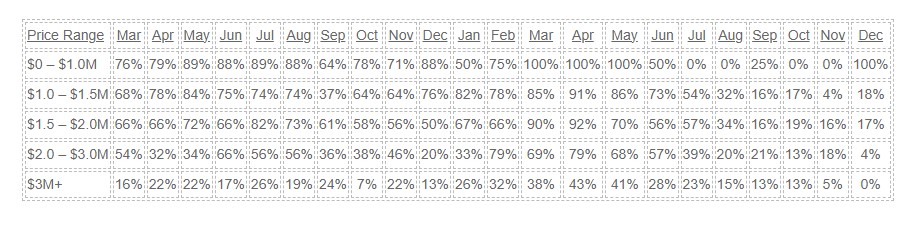

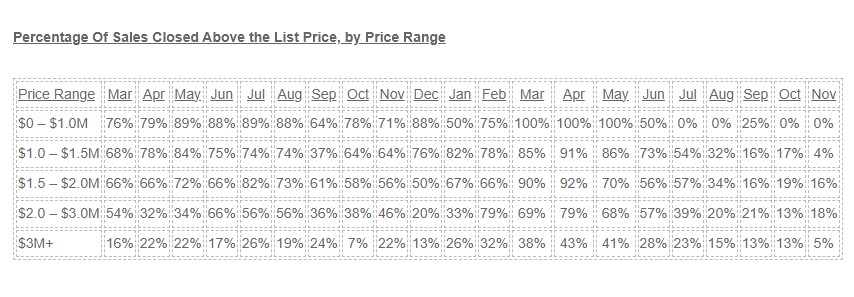

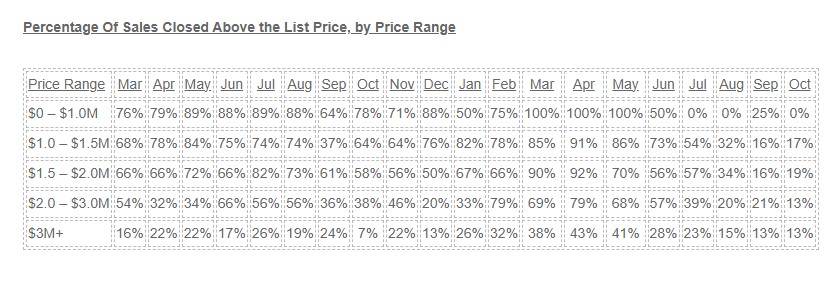

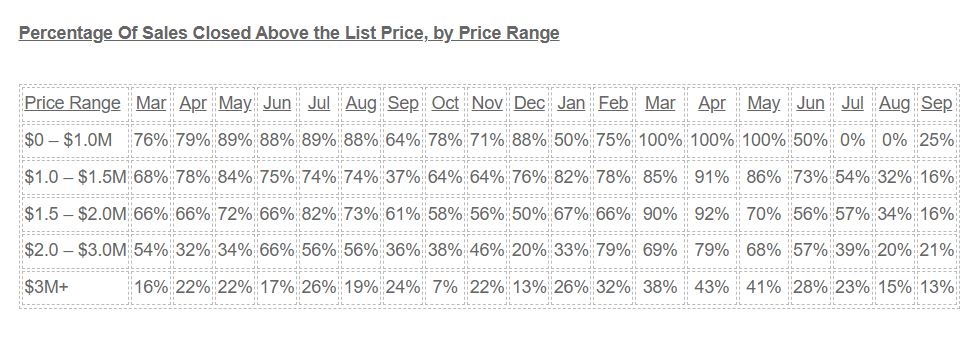

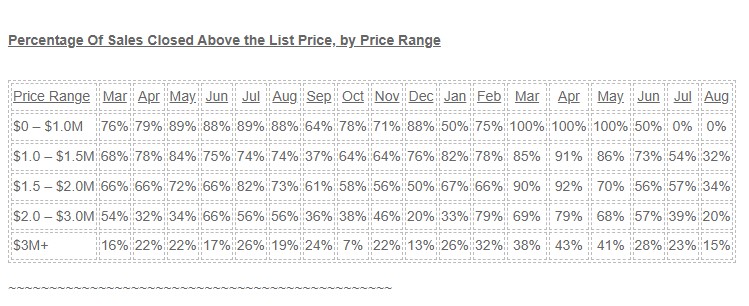

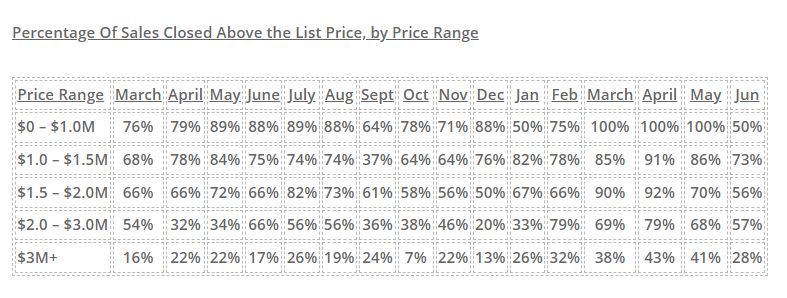

Percentage Of Sales Closed Above the List Price, by Price Range

If the over-list sales start to increase this spring and get above 20%, then the frenzy feelings are slipping back into the equation. Hopefully they will be accompanied by more than 100 sales, because if that’s all we have during the selling season, there should be real dogfights over the creampuffs.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

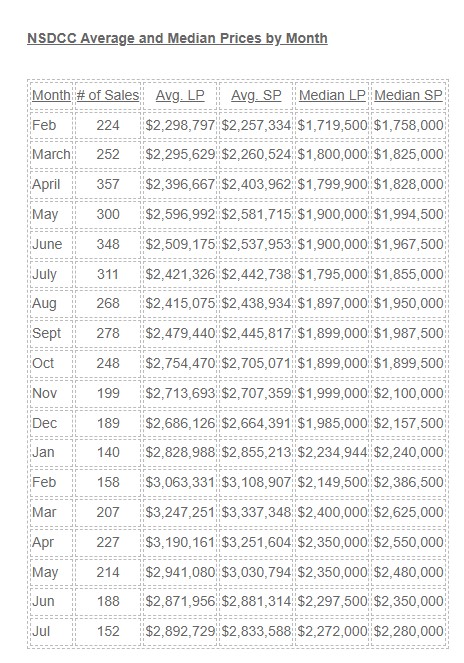

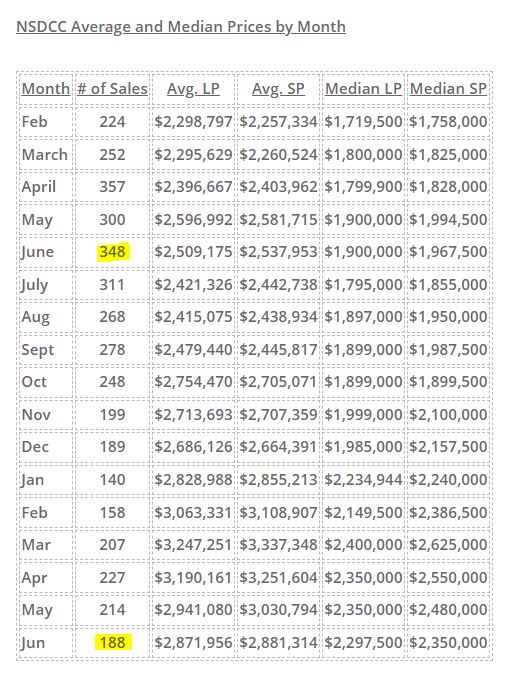

NSDCC Average and Median Prices by Month

Month

# of Sales

Avg. LP

Avg. SP

Median LP

Median SP

Feb

224

$2,298,797

$2,257,334

$1,719,500

$1,758,000

March

252

$2,295,629

$2,260,524

$1,800,000

$1,825,000

April

357

$2,396,667

$2,403,962

$1,799,900

$1,828,000

May

300

$2,596,992

$2,581,715

$1,900,000

$1,994,500

June

348

$2,509,175

$2,537,953

$1,900,000

$1,967,500

July

311

$2,421,326

$2,442,738

$1,795,000

$1,855,000

Aug

268

$2,415,075

$2,438,934

$1,897,000

$1,950,000

Sept

278

$2,479,440

$2,445,817

$1,899,000

$1,987,500

Oct

248

$2,754,470

$2,705,071

$1,899,000

$1,899,500

Nov

199

$2,713,693

$2,707,359

$1,999,000

$2,100,000

Dec

189

$2,686,126

$2,664,391

$1,985,000

$2,157,500

Jan

140

$2,828,988

$2,855,213

$2,234,944

$2,240,000

Feb

158

$3,063,331

$3,108,907

$2,149,500

$2,386,500

Mar

207

$3,247,251

$3,337,348

$2,400,000

$2,625,000

Apr

227

$3,190,161

$3,251,604

$2,350,000

$2,550,000

May

215

$2,943,657

$3,032,977

$2,350,000

$2,500,000

Jun

190

$2,864,089

$2,872,690

$2,297,500

$2,350,000

Jul

155

$2,889,612

$2,832,080

$2,299,900

$2,300,000

Aug

164

$2,933,243

$2,830,855

$2,200,000

$2,150,000

Sep

135

$2,650,642

$2,560,314

$2,149,000

$2,040,000

Oct

124

$3,090,320

$2,971,211

$2,272,500

$2,212,500

Nov

115

$2,581,790

$2,459,974

$1,950,000

$1,875,000

Dec

100

$2,859,960

$2,675,549

$2,097,500

$1,892,500

In the months when the average and median sales prices increased, it didn’t mean your home’s value went up – it just means that the set of homes were a little bigger and nicer than other months.

But if you want to make comparisons, then these latest averages and medians are similar to October, 2021.

Only 12% of the houses sold last month actually closed over their list price, which sounds normal.

There were 51 of the 115 of the sales (44%) that closed for $100,000+ BELOW their last list price.

The count of 51 broke down to 17 of 19 sales over $3,000,000, and 34 of 96 sales under $3,000,000 – where knocking off $100,000+ off the list price is fairly significant. Either realtors aren’t that great about their pricing, or they wander into lowball territory and get their head tore off.

The median days-on-market was 28 days, and the average was 41 days.

About half wandered into lowball territory, and about half sold for $100,000+ below their list price – there is a direct connection. People need to figure out how to sell the house in the first couple of weeks of being on the market, or face the same consequences in 2023.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

NSDCC Average and Median Prices by Month

Month

# of Sales

Avg. LP

Avg. SP

Median LP

Median SP

Feb

224

$2,298,797

$2,257,334

$1,719,500

$1,758,000

March

252

$2,295,629

$2,260,524

$1,800,000

$1,825,000

April

357

$2,396,667

$2,403,962

$1,799,900

$1,828,000

May

300

$2,596,992

$2,581,715

$1,900,000

$1,994,500

June

348

$2,509,175

$2,537,953

$1,900,000

$1,967,500

July

311

$2,421,326

$2,442,738

$1,795,000

$1,855,000

Aug

268

$2,415,075

$2,438,934

$1,897,000

$1,950,000

Sept

278

$2,479,440

$2,445,817

$1,899,000

$1,987,500

Oct

248

$2,754,470

$2,705,071

$1,899,000

$1,899,500

Nov

199

$2,713,693

$2,707,359

$1,999,000

$2,100,000

Dec

189

$2,686,126

$2,664,391

$1,985,000

$2,157,500

Jan

140

$2,828,988

$2,855,213

$2,234,944

$2,240,000

Feb

158

$3,063,331

$3,108,907

$2,149,500

$2,386,500

Mar

207

$3,247,251

$3,337,348

$2,400,000

$2,625,000

Apr

227

$3,190,161

$3,251,604

$2,350,000

$2,550,000

May

215

$2,943,657

$3,032,977

$2,350,000

$2,500,000

Jun

190

$2,864,089

$2,872,690

$2,297,500

$2,350,000

Jul

155

$2,889,612

$2,832,080

$2,299,900

$2,300,000

Aug

164

$2,933,243

$2,830,855

$2,200,000

$2,150,000

Sep

135

$2,650,642

$2,560,314

$2,149,000

$2,040,000

Oct

124

$3,090,320

$2,971,211

$2,272,500

$2,212,500

Nov

115

$2,581,790

$2,459,974

$1,950,000

$1,875,000

In October, when the average and median sales price spiked, it didn’t mean your home’s value went up – the homes sold that month had a median square footage that was 12% higher than in September. Similarly, the group of homes that sold in November had a median sf that was 8% smaller than in October.

But if you do want to make a big deal of these sales prices, they are similar to those in July, 2021.

It means the set of homes that closed escrow in October happen to produce higher numbers because they were larger (October median sf was +12%) and more attractive than the group in September.

BOTH THE AVERAGE AND MEDIAN SALES PRICES ARE -23% SINCE MARCH.

We saw that the difference needed to fully compensate for the higher rates is -30%. We’re almost there, and the full effect should be built in by springtime!

Please note that I didn’t say home prices are down 23%.

The median sales price is 23% lower than it was six months ago.

The over-bidding is winding down to more manageable levels as just 24% of August buyers were willing to pay over the list price. As usual, the $1,000,000 to $2,000,000 range was the most active, where inventory is low and the number of quality homes for sale even lower:

The number of sales in August were higher than they were in July, but still well under recent history:

NSDCC August Sales

2018: 275

2019: 263

2020: 351

2021: 268

2020: 161

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

NSDCC Average and Median Prices by Month

Month

# of Sales

Avg. LP

Avg. SP

Median LP

Median SP

Feb

224

$2,298,797

$2,257,334

$1,719,500

$1,758,000

March

252

$2,295,629

$2,260,524

$1,800,000

$1,825,000

April

357

$2,396,667

$2,403,962

$1,799,900

$1,828,000

May

300

$2,596,992

$2,581,715

$1,900,000

$1,994,500

June

348

$2,509,175

$2,537,953

$1,900,000

$1,967,500

July

311

$2,421,326

$2,442,738

$1,795,000

$1,855,000

Aug

268

$2,415,075

$2,438,934

$1,897,000

$1,950,000

Sept

278

$2,479,440

$2,445,817

$1,899,000

$1,987,500

Oct

248

$2,754,470

$2,705,071

$1,899,000

$1,899,500

Nov

199

$2,713,693

$2,707,359

$1,999,000

$2,100,000

Dec

189

$2,686,126

$2,664,391

$1,985,000

$2,157,500

Jan

140

$2,828,988

$2,855,213

$2,234,944

$2,240,000

Feb

158

$3,063,331

$3,108,907

$2,149,500

$2,386,500

Mar

207

$3,247,251

$3,337,348

$2,400,000

$2,625,000

Apr

227

$3,190,161

$3,251,604

$2,350,000

$2,550,000

May

214

$2,941,080

$3,030,794

$2,350,000

$2,480,000

Jun

188

$2,871,956

$2,881,314

$2,297,500

$2,350,000

Jul

152

$2,892,729

$2,833,588

$2,272,000

$2,280,000

Aug

161

$2,953,967

$2,849,332

$2,200,000

$2,150,000

This is much more normal – the average and median sales prices are under their list prices!

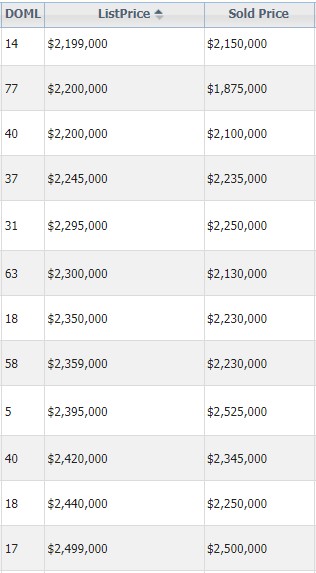

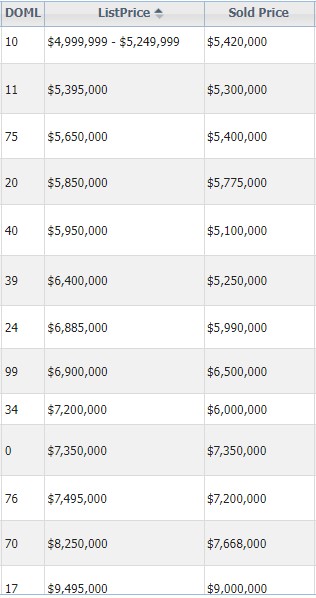

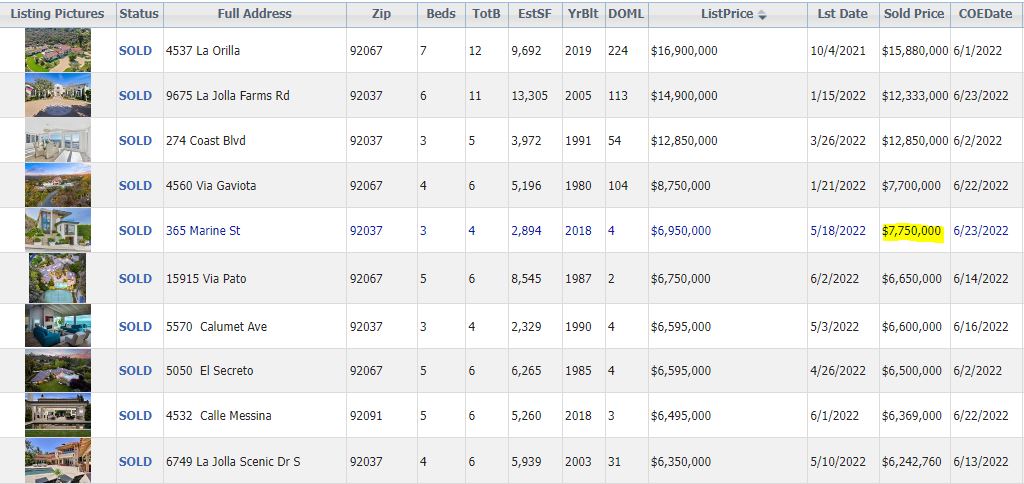

Want proof that Jay Powell has tamed the housing frenzy, and reversed the trend of buyers having to pay well over the list price to win a house? Here are examples of the list and sold prices of August home sales between La Jolla and Carlsbad – note the relationship to the days-on-market (DOML):

So far, we’ve had 154 August closings reported, which means we should get up to 175 or so by the time every sale is inputted.

I’ll do the final count later, but of the 154 sales, there were 23% that sold over their list price. But it is much more reasonable and sustainable if buyers only have to pay $25,000 to $50,000 over the list price for the creampuffs, rather than $400,000 to $800,000!

Sellers shouldn’t be bummed either, because their huge gains are priced in now.

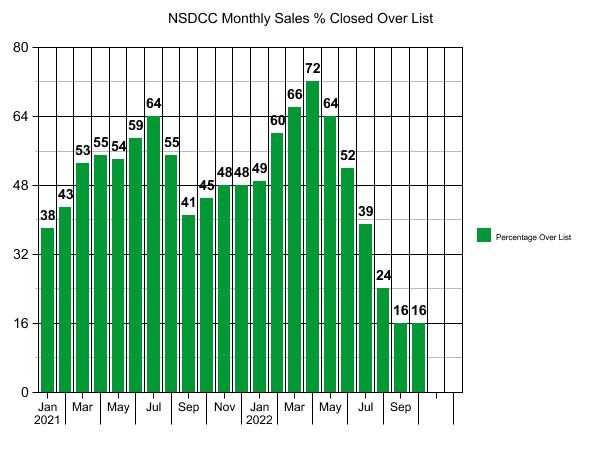

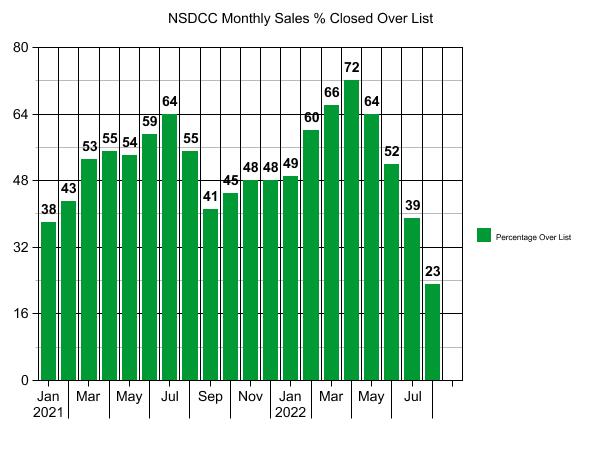

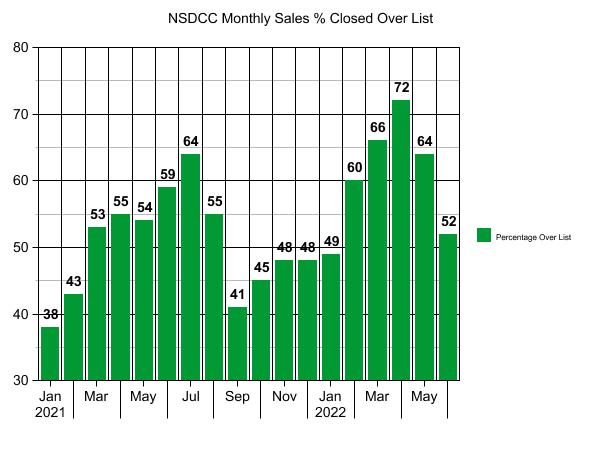

The graph above shows how the 2021 off-season wasn’t off by much, with nearly half of the Nov-Jan sales closing over their list price. We probably won’t see that happen this year!

On the street, it feels like the off-season is already here, which is fine. The seasonality has been topsy-turvy ever since the pandemic started, so we can handle a longer off-season this year. The outcome will be determined by what the listing agents are telling their sellers.

Are they saying that this is the start of a long downward slide, and sellers should hit the panic button and dump on price to get out while they can? If so, shame on them. If 39% of the buyers who closed in July were still paying over the list price, then it suggests that what we are experiencing is an inventory problem – there aren’t many superior houses for sale at decent prices, and the gap between them and inferior houses hasn’t adjusted enough yet.

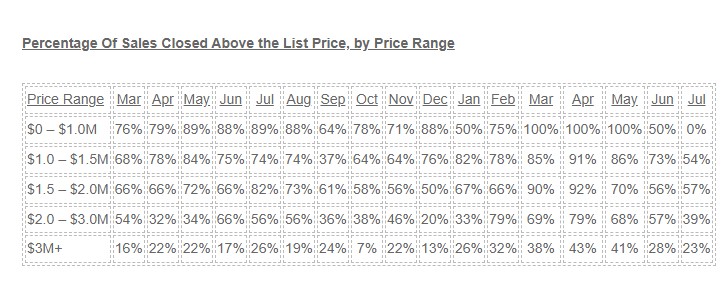

Here is the breakdown by price range:

There was only one sale under $1,000,000, and it was a mobile home. Most of the homes sold between $1,000,000 and $2,000,000 closed for more than their list prices, and the sales above $2 million were still competitive. The group of salable homes is smaller than before, but the great ones are still being bid up.

The average and median sales prices are closer to the list prices now, suggesting that those who do bid over the list price aren’t going over by much:

For an industry that has never figured out how to properly handle a bidding war, it is a miracle that this many homes are still selling over list. This was our big chance to incorporate a true auction format, but it will pass us by, unfortunately.

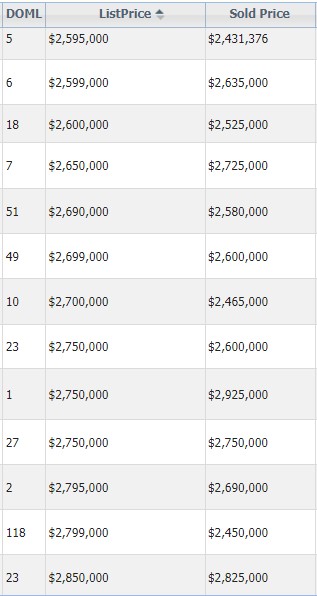

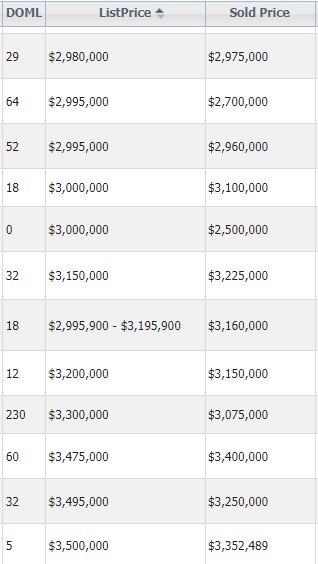

Here is a good sampling of the NSDCC pricing decisions made in May (mortgage rates started going up the first of April). The days-on-market are on the left.

Days on Market: All 28 found their buyer quickly – only one took as long as ten days!

Paid Over List: 21 of 28 paid over the list price (75%).

Of the 21 who paid over the list price, the average amount paid over list was $185,761. Literally 11 out of 21 paid at least $200,000 over list – and these 28 sales are the mid-range group!

Paying over the list price must have some addictive qualities!

Either that, or the superior homes are still attracting a lot of attention. Well into the higher-rate environment, more than half of the June buyers paid over the list price!

Here is the breakdown by price range:

The average and median sales prices have been drifting downward, but both are still above the list prices:

The year-over-year sales are going to look terrible because 2021 was an incredible frenzy. The NSDCC June sales in the three previous years were 274, 282, and 299, so the 188 is only 34% below that average.

My La Jolla sale was the fifth-highest sales price in June, and sold for $1,150,000 more than the oceanfront house on Calumet. My $800,000 over list was #1 – it was the most over list of all the June sales!

We are having fewer sales between Carlsbad and La Jolla, but about the same percentage are closing over the list price as we’ve seen in the previous months of 2022:

NSDCC Detached-Home Sales, June (Month-to-Date)

Number of Sales: 104

Number of Sales Closed Over List: 68 (65%)

Average List Price of Over Lists: $2,298,732

Average Sales Price of Over Lists: $2,448,509

SP:LP = 107%

Median List Price of Over Lists: $2,100,000

Median Sales Price of Over Lists: $2,267,500

SP:LP = 108%

Can we say that the list pricing has come down much? Not really.

The median days-on market of those that closed over list was 8 days, so pretty much all of the buyers were into the higher mortgage-rate era when they made their decision.

I know it’s tempting for waiting buyers to think it’s going to get better, later – but so far, all that’s happened is fewer sales.