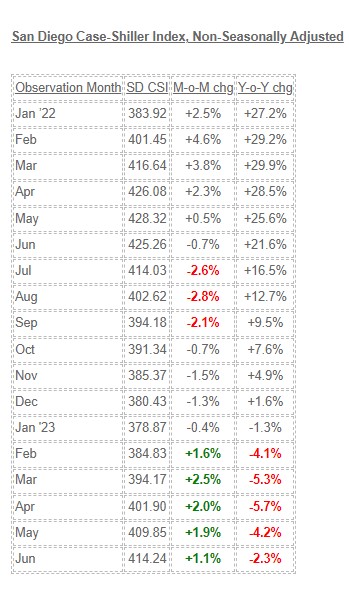

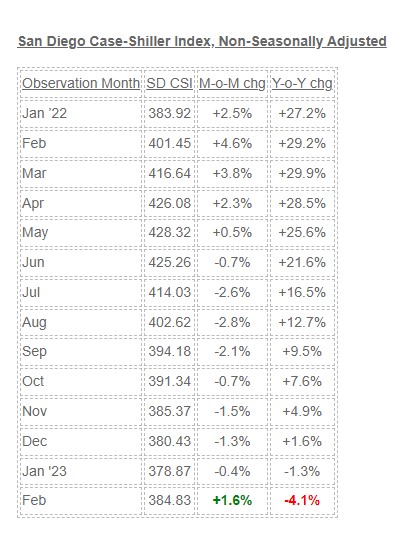

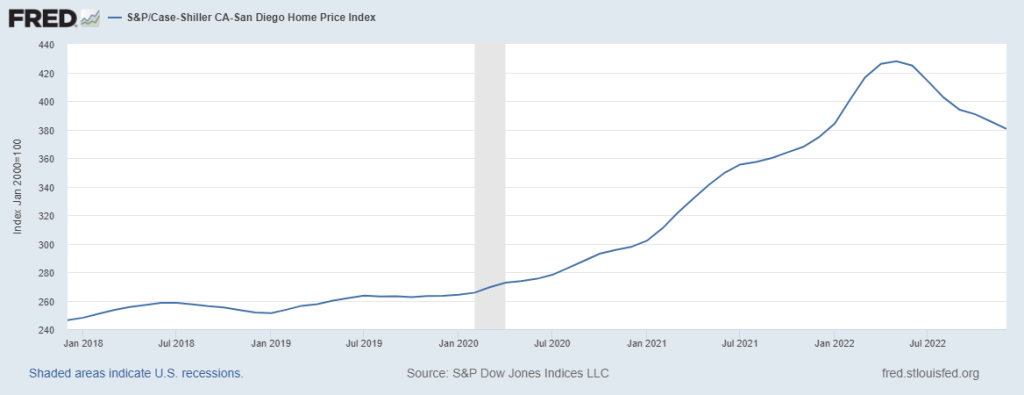

Higher mortgage rates caused the San Diego Case-Shiller index to take a tumble last summer. The decline moderated towards the end of the year and bottomed in January.

Since then, it went up 9.3%, which is pretty good appreciation for five months!

July and August will be hot too, but we are overdue for a break. It should mellow out for the rest of 2023.

Be prepared for a fast start in 2024. The market should be at full speed in February, which is contrary to the wait-and-see approach I expected as the frenzy was winding down. The frenzy conditions are still around – I sold my listing in Oceanside for $200,000 over list!

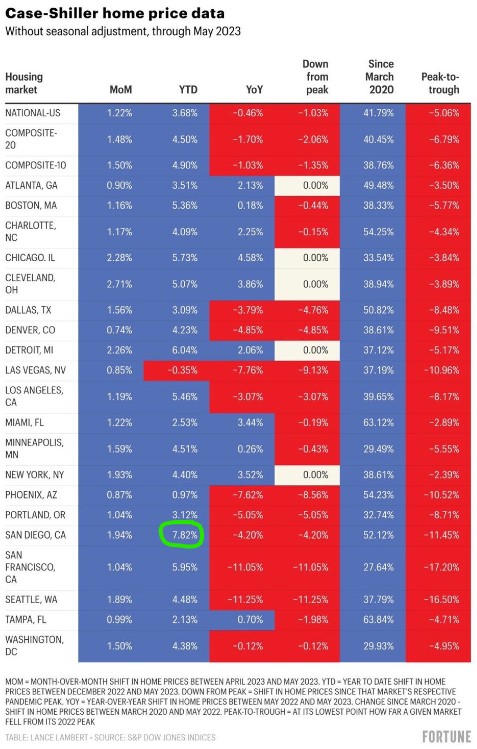

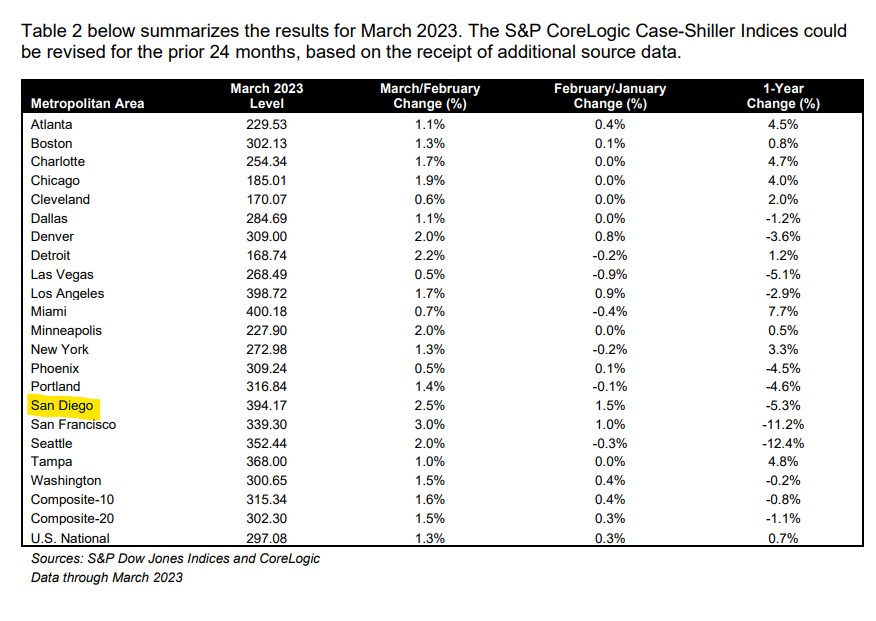

The Case-Shiller Index has risen more this year in San Diego than in any other metro area!

Could we end up being the most expensive metro in the country some day? It could happen, and it would be a return to the top spot, according to Channel 8 – check the first 30 seconds here:

Even though we’ve had healthy gains in 2023, the YoY declines makes it look like we’re going backwards because the index was rising so quickly last year. Hard to imagine any more MoM gains of 3.8% or 4.6%!

April’s index is about the same as it was in February AND August, 2022.

Going forward, it should settle in to a range of 390-420 for the next couple of years.

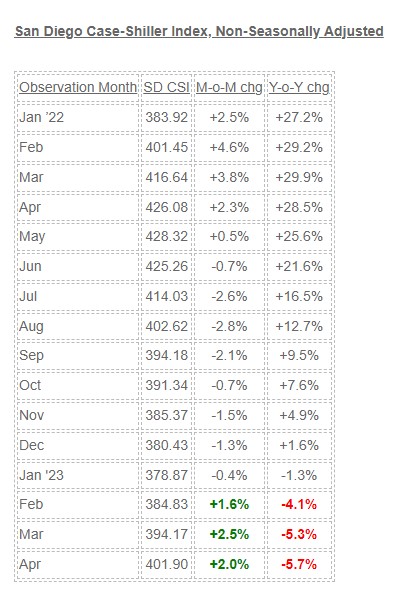

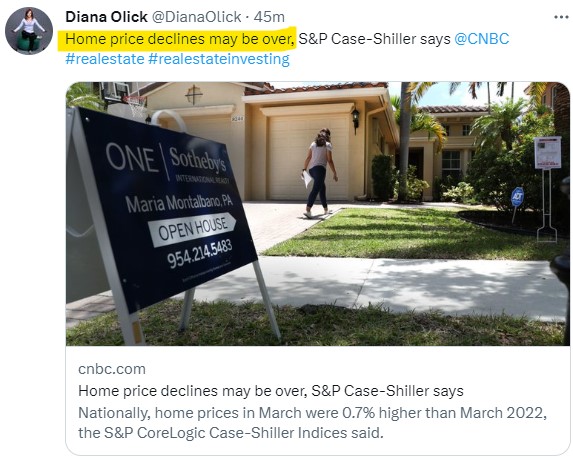

However, the view from the ivory tower is that we’ve survived the downturn and we’re fine now. Because the Case-Shiller Index is so dated, he already knows that the next 2-3 months will be positive:

“If I were trying to make a case that the decline in home prices that began in June 2022 had definitively ended in January 2023, April’s data would bolster my argument. Whether we see further support for that view in coming months will depend on the how well the market navigates the challenges posed by current mortgage rates and the continuing possibility of economic weakness.”

My guess is that the second half of 2023 will go back to Plateau City, like it did in 2019:

Our YoY change is more negative this month because in early-2022 it was flying – the local Case-Shiller Index went up 11% between January and April last year!

We had the second-highest MoM gain in the country:

Here’s another guy who ignores the seasonal trends and instead just declares that price declines are over:

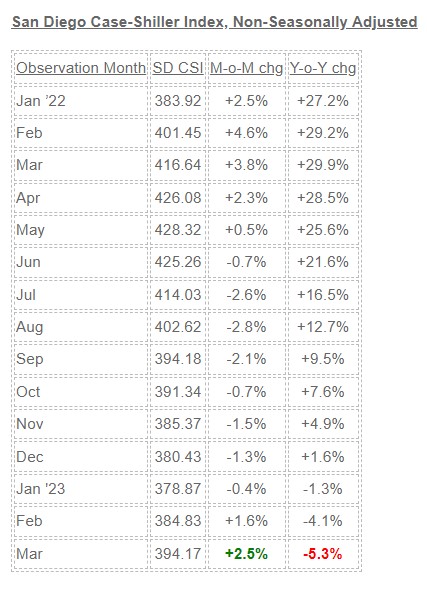

“The modest increases in home prices we saw a month ago accelerated in March 2023,” said Craig J. Lazzara, managing director at S&P DJI in a release.

“Two months of increasing prices do not a definitive recovery make, but March’s results suggest that the decline in home prices that began in June 2022 may have come to an end.”

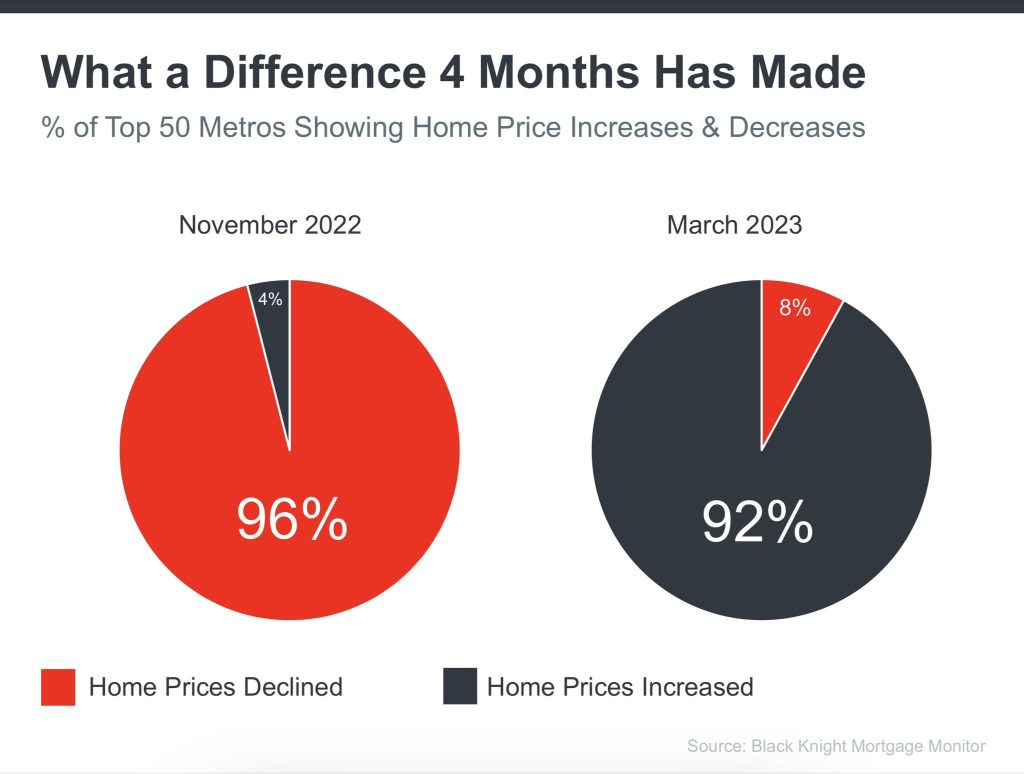

In spite of higher rates, the spring selling season has delivered, though the second half of 2023 is TBD. Thanks Steve Harney and Ryan Lundquist for the graphics!

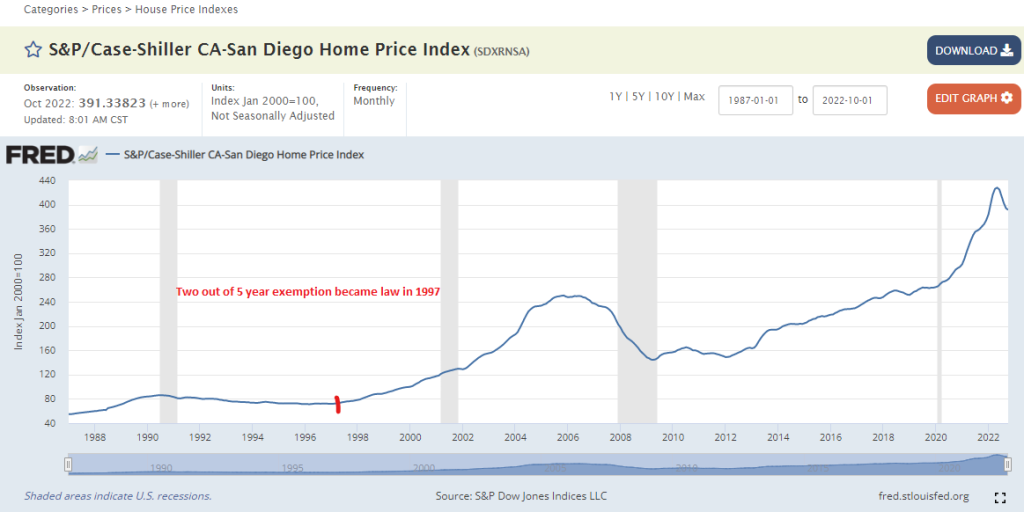

For those who like to look back fondly at ancient history and reminisce about what used to be, I present to you the local Case-Shiller Index. About the time that the market starts to sputter in mid-to-late summer, we will be getting the spring data that will look red hot.

“The results released today pre-date the disruptions in the commercial banking industry which began in early March. Although forecasts are mixed, so far the Federal Reserve seems focused on its inflation-reduction targets, which suggests that interest rates may remain elevated, at least in the near-term. Mortgage financing and the prospect of economic weakness are therefore likely to remain a headwind for housing prices for at least the next several months.”

San Diego County’s median home price rose 5.3 percent in March — reversing nine months of declines — to $790,000, according to CoreLogic data released today. The region’s median, the point at which half the homes sold for more and half for less, is still down 1.3 percent annually. Rising mortgage rates had softened the red-hot market in recent months. Yet real estate agents said competition over limited supply, and realization that rates weren’t decreasing, pushed buyers to make a move.

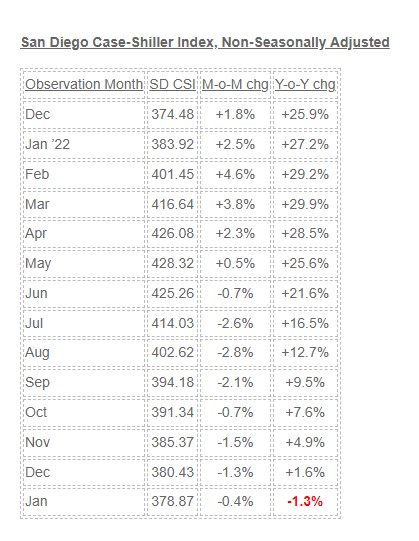

Here we go – the first negative year-over-year reading!

The index will probably stay negative for another one or two readings, then level off and maybe rise during the spring – but we won’t know until summer due to the lag in reporting.

Any gain during the spring selling season will likely be given back in the second half of the year as seasonality creeps back in – even though the consensus will be that the higher rates and recession finally crushed real estate by 2024.

This is funny how the reporter got it right about there being too few homes for sale. But then the quote from the expert that followed made no mention of inventory. Most of the country is blind to what’s really going on because the doom, real or imagined, is ingrained daily by the psuedo-experts – which causes potential sellers to wait it out:

Prices were lower year over year in San Francisco (-7.6%), Seattle (-5.1%), Portland, Oregon (-0.5%) and San Diego (-1.4%). They were flat in Phoenix.

Miami, Tampa and Atlanta again saw the hottest annual price gains of the top 20 cities. Miami prices were up 13.8%, Tampa prices up 10.5%, and Atlanta prices rose 8.4%. All 20 cities, however, reported lower prices in the year ending January 2023 versus the year ending December 2022.

Homebuyers may be seeing more flexible sellers this spring, but there are still too few homes available for sale. Mortgage lending may also tighten in light of pressure on the banking system.

“More expensive, less available borrowing, especially with an unclear economic outlook, is likely to continue to limit buyer demand. Though home sales are expected to rebound in line with seasonal trends, this spring’s sales pace is expected to remain lower than last year, as uncertainty and high costs limit activity,” said Hannah Jones, economic data analyst for Realtor.com.

The local index is 11% lower than its peak in May.

The beauty about this market is that buyers don’t have to fight with the decision to buy now or wait. Because the inventory of quality homes is so thin, having to wait is baked in.

How often do buyers see a home for sale that interests them? Once a month, maybe?

The higher rates go, the more sellers will think it’s a bad time to sell – causing FEWER homes for sale.

It’s a big game of chicken, and you have to wonder if every buyer will get the memo to hold out. If renegade buyers keep paying retail for the premium properties, it spoils the whole idea of prices dropping.

Will higher rates cause better pricing on the homes you are willing to buy?

Don’t ask Jay Powell, because he doesn’t know. He said:

We are well aware that mortgage rates have moved up a lot. And you are seeing a changing housing market. We are watching it to see what will happen.

How much will it really affect residential investment? Not really sure.

How much will it affect housing prices? Not really sure.

Today’s local Case-Shiller reading for November is the fifth in a row that reflects the much-higher mortgage rates. The index has dropped 9% since May – don’t be surprised if in the future we see a similar trend of enthusiasm in springtime, and doldrums in the off-season:

San Diego Non-Seasonally-Adjusted CSI changes

Observation Month

SD CSI

M-o-M chg

Y-o-Y chg

Jan ’21

301.72

+1.4%

+14.3%

Feb

310.62

+2.9%

+17.1%

Mar

320.81

+3.3%

+19.1%

Apr

331.47

+3.3%

+21.6%

May

341.05

+2.9%

+24.7%

Jun

349.78

+2.6%

+27.2%

Jul

355.33

+1.6%

+27.8%

Aug

357.11

+0.5%

+26.2%

Sep

359.88

+0.8%

+24.9%

Oct

363.80

+1.1%

+24.2%

Nov

367.62

+1.1%

+24.3%

Dec

374.48

+1.8%

+25.9%

Jan ’22

383.92

+2.5%

+27.2%

Feb

401.45

+4.6%

+29.2%

Mar

416.64

+3.8%

+29.9%

Apr

426.08

+2.3%

+28.5%

May

428.32

+0.5%

+25.6%

Jun

425.26

-0.7%

+21.6%

Jul

414.03

-2.6%

+16.5%

Aug

402.62

-2.8%

+12.7%

Sep

394.18

-2.1%

+9.5%

Oct

391.34

-0.7%

+7.6%

Nov

385.37

-1.5%

+4.9%

If the index keeps dropping over the next few months (likely), it should mean that it will get down to the late-2021 numbers. Will that be enough to impress buyers that prices are reasonable now? Or will they just go out and buy because it’s springtime?

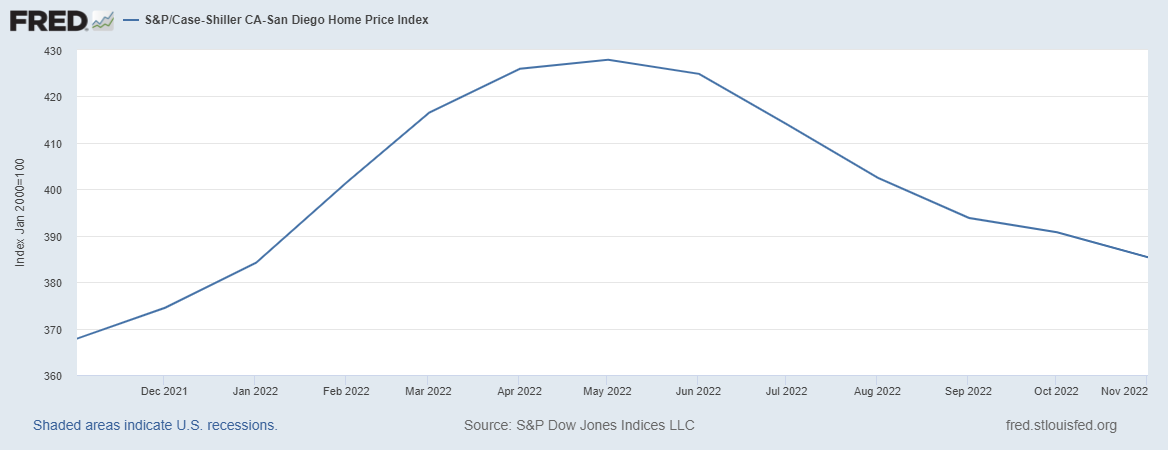

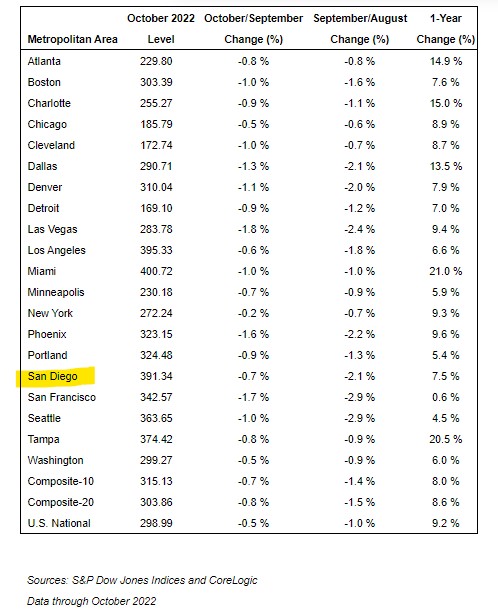

The local index peaked in May, so today’s local Case-Shiller reading for October is the fourth in a row that reflects the much-higher mortgage rates:

San Diego Non-Seasonally-Adjusted CSI changes

Observation Month

SD CSI

M-o-M chg

Y-o-Y chg

Jan ’21

301.72

+1.4%

+14.3%

Feb

310.62

+2.9%

+17.1%

Mar

320.81

+3.3%

+19.1%

Apr

331.47

+3.3%

+21.6%

May

341.05

+2.9%

+24.7%

Jun

349.78

+2.6%

+27.2%

Jul

355.33

+1.6%

+27.8%

Aug

357.11

+0.5%

+26.2%

Sep

359.88

+0.8%

+24.9%

Oct

363.80

+1.1%

+24.2%

Nov

367.62

+1.1%

+24.3%

Dec

374.48

+1.8%

+25.9%

Jan ’22

383.92

+2.5%

+27.2%

Feb

401.45

+4.6%

+29.2%

Mar

416.64

+3.8%

+29.9%

Apr

426.08

+2.3%

+28.5%

May

428.32

+0.5%

+25.6%

Jun

425.26

-0.7%

+21.6%

Jul

414.03

-2.6%

+16.5%

Aug

402.62

-2.8%

+12.7%

Sep

394.18

-2.1%

+9.5%

Oct

391.34

-0.7%

+7.6%

It looks like we may have seen the worst of it?

If so, and the monthly declines are tempered over the next couple of readings, it should mean that the index will be in the 380-390 range as we roll into the spring selling season – or about where it was a year ago.

It sure seems to be going better than most people thought it would!