How the mainstream media is reporting today’s Case-Shiller numbers:

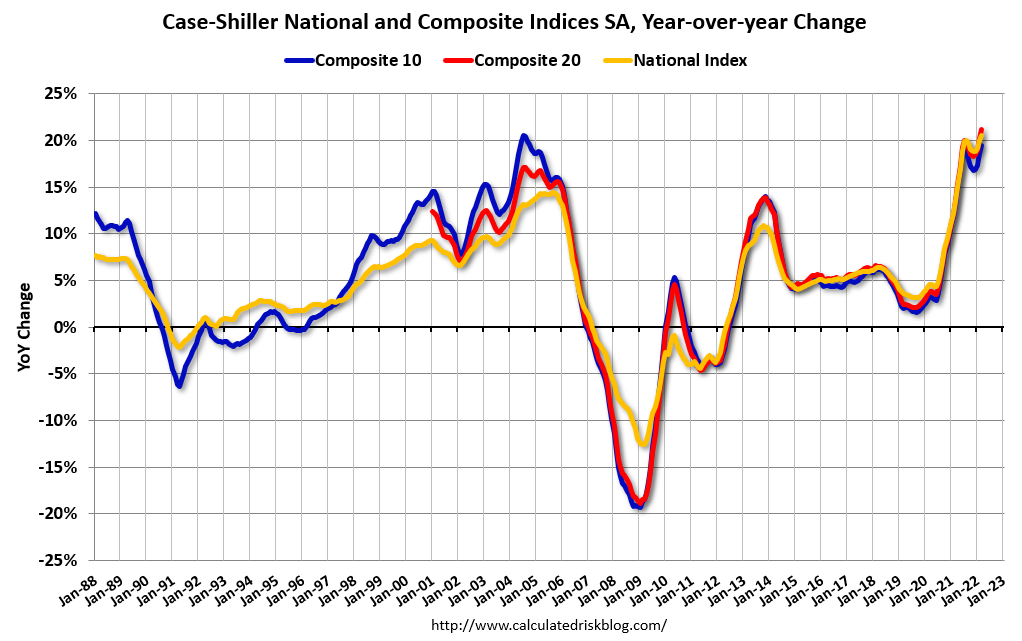

U.S. single-family home prices slowed further in September as higher mortgage rates eroded demand.

Monthly house prices fell in July for the first time since late 2018.

The housing market has been hammered by aggressive Federal Reserve interest rate hikes that are aimed at curbing high inflation by dampening demand in the economy.

How it could/should be reported:

Higher rates are causing buyers AND sellers to wait-and-see.

Inventory is expected to be lower than ever in 2023.

Realtors aren’t offering viable solutions.

A guy on twitter said that the real story is that YoY appreciation is still positive, which should make the vast majority of American homeowners happy. But I commented on how the NAR is publishing articles now that ignore/omit the downturn. I think that those of us who are in the business of assisting consumers with their real estate decisions should give accurate advice on how to cope with the current market conditions.

San Diego Non-Seasonally-Adjusted CSI changes

Observation Month

SD CSI

M-o-M chg

Y-o-Y chg

Jan ’21

301.72

+1.4%

+14.3%

Feb

310.62

+2.9%

+17.1%

Mar

320.81

+3.3%

+19.1%

Apr

331.47

+3.3%

+21.6%

May

341.05

+2.9%

+24.7%

Jun

349.78

+2.6%

+27.2%

Jul

355.33

+1.6%

+27.8%

Aug

357.11

+0.5%

+26.2%

Sep

359.88

+0.8%

+24.9%

Oct

363.80

+1.1%

+24.2%

Nov

367.62

+1.1%

+24.3%

Dec

374.48

+1.8%

+25.9%

Jan ’22

383.92

+2.5%

+27.2%

Feb

401.45

+4.6%

+29.2%

Mar

416.64

+3.8%

+29.9%

Apr

426.08

+2.3%

+28.5%

May

428.32

+0.5%

+25.6%

Jun

425.26

-0.7%

+21.6%

Jul

414.03

-2.6%

+16.5%

Aug

402.62

-2.8%

+12.7%

Sep

394.18

-2.1%

+9.5%

While current homeowners might be relieved to see the big pop in appreciation over time, if they are thinking of moving, they should recalibrate everything they think they know about selling homes.

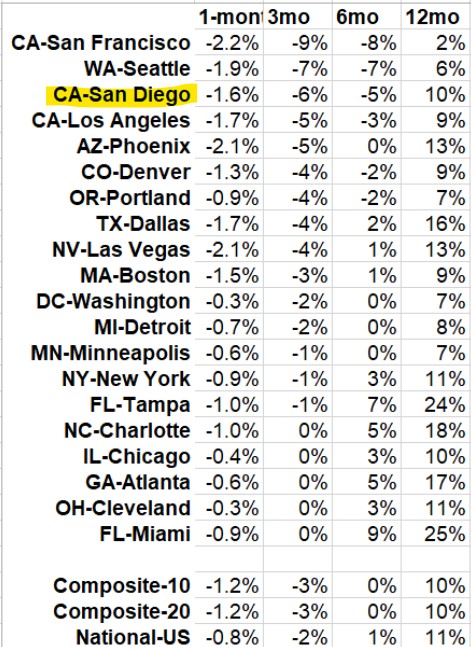

“The forceful deceleration in U.S. housing prices that we noted a month ago continued in our report for August 2022,” says Craig J. Lazzara, Managing Director at S&P DJI. “For example, the National Composite Index rose by 13.0% for the 12 months ended in August, down from its 15.6% year-over-year growth in July. The -2.6% difference between those two monthly rates of change is the largest deceleration in the history of the index (with July’s deceleration now ranking as the second largest). We see similar patterns in our 10-City Composite (up 12.1% in August vs. 14.9% in July) and our 20-City Composite (up 13.1% in August vs. 16.0% in July). Further, price gains decelerated in every one of our 20 cities. These data show clearly that the growth rate of housing prices peaked in the spring of 2022 and has been declining ever since.

“Month-over-month comparisons are consistent with these observations. All three composites declined in July, as did prices in every one of our 20 cities. On a month-over-month basis, the biggest declines occurred on the west coast, with San Francisco (-4.3%), Seattle (-3.9%), and San Diego (-2.8%) falling the most.

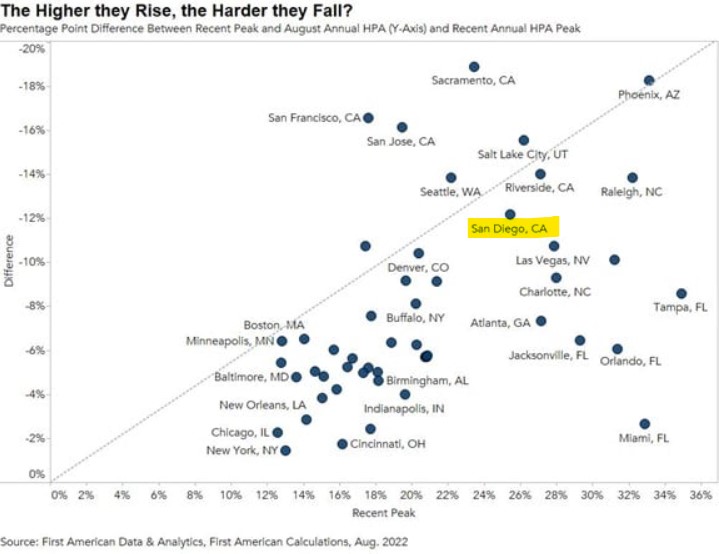

The local Case-Shiller index is due tomorrow, and expectations are for a 2% drop from June. First American has their own repeat-sales index which is already showing a 12% decline in San Diego pricing (above).

While the -12% over six months is probably a surprise to people who think pricing is downward sticky, it’s different this time. In the past, the home-equity positions were much smaller, and many sellers had hold out just to have enough for a steak dinner at closing.

None of today’s sellers need to hold out. All of them could sell today for what the market will bear, if they could just get out of their own way. Yes, it’s true that they may have plans for all the money and need to sell for their price, and those sellers should just wait it out.

This could be over before you know it.

Is there a specific marker for home buyers to know when it’s time to buy? Or is it just when prices go down?

Is the -12% enough to get the attention of the highly-motivated buyers – those who don’t own a house yet?

Or will they just look up in March/April and say, “Close enough!”

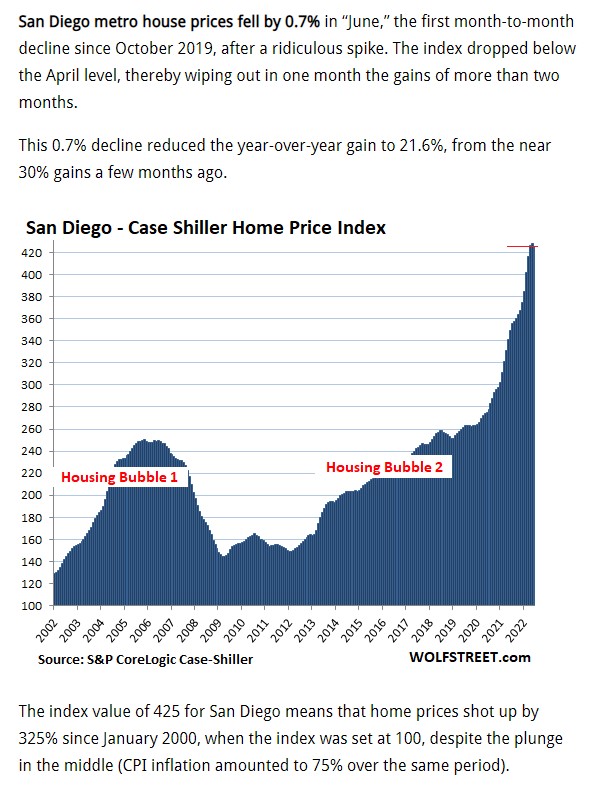

Everyone is throwing around the ‘deceleration’ word like it means something. But the only number that matters is the month-over-month change, which went DOWN for the first time since October 2019 – but it only went down that one month. The local index dropped 2.8% between July, 2018 and January, 2019, and we’ll probably see more than that this year.

Homes still won’t be affordable for most, and there won’t be many for sale as the Big Standoff of 2023 sets up.

San Diego Non-Seasonally-Adjusted CSI changes

Observation Month

SD CSI

M-o-M chg

Y-o-Y chg

Jan ’20

264.04

+0.2%

+5.1%

Feb

265.34

+0.5%

+4.6%

Mar

269.63

+1.6%

+5.2%

Apr

272.48

+1.1%

+5.8%

May

273.51

+0.4%

+5.2%

Jun

274.91

+0.5%

+5.0%

Jul

278.00

+1.1%

+5.4%

Aug

283.06

+1.8%

+7.6%

Sep

288.11

+1.8%

+9.4%

Oct

292.85

+1.6%

+11.5%

Nov

295.64

+1.0%

+12.3%

Dec

297.52

+0.6%

+13.0%

Jan ’21

301.72

+1.4%

+14.3%

Feb

310.62

+2.9%

+17.1%

Mar

320.81

+3.3%

+19.1%

Apr

331.47

+3.3%

+21.6%

May

341.05

+2.9%

+24.7%

Jun

349.78

+2.6%

+27.2%

Jul

355.33

+1.6%

+27.8%

Aug

357.11

+0.5%

+26.2%

Sep

359.88

+0.8%

+24.9%

Oct

363.80

+1.1%

+24.2%

Nov

367.62

+1.1%

+24.3%

Dec

374.48

+1.8%

+25.9%

Jan ’22

383.92

+2.5%

+27.2%

Feb

401.45

+4.6%

+29.2%

Mar

416.64

+3.8%

+29.9%

Apr

426.08

+2.3%

+28.5%

May

428.32

+0.5%

+25.6%

Jun

425.26

-0.7%

+21.6%

“It’s important to bear in mind that deceleration and decline are two entirely different things, and that prices are still rising at a robust clip,” wrote Craig Lazzara, managing director at S&P Dow Jones Indices in a release. “June’s growth rates for all three composites are at or above the 95th percentile of historical experience. For the first six months of 2022, in fact, the National Composite is up 10.6%.”

In the last 35 years, only four complete years have witnessed increases that large, he added.

Another report last week showed home prices declined 0.77% from June to July. It was the first monthly fall in nearly three years, according to Black Knight, a mortgage software, data and analytics firm.

While the drop may seem small, it is the largest single-month decline in prices since January 2011. It is also the second-worst July performance dating back to 1991, behind the 0.9% decline in July 2010, during the Great Recession.

Home prices are softening due to rising mortgage rates, making an already expensive housing market even more so. Sales of both new and existing homes have been dropping for several months, leading some economists to call a housing recession.

“We’ve noted previously that mortgage financing has become more expensive as the Federal Reserve ratchets up interest rates, a process that continued as our June data were gathered. As the macroeconomic environment continues to be challenging, home prices may well continue to decelerate,” said Lazzara.

Last month I guessed we’ll be 400+ at the end of the year, or about the same as February. If our local Case-Shiller Index drops 0.5% per month for the next seven readings, we’d still be in positive territory for 2022. We haven’t had a negative MoM reading since December, 2018.

San Diego Non-Seasonally-Adjusted CSI changes

Observation Month

SD CSI

M-o-M chg

Y-o-Y chg

Jan ’20

264.04

+0.2%

+5.1%

Feb

265.34

+0.5%

+4.6%

Mar

269.63

+1.6%

+5.2%

Apr

272.48

+1.1%

+5.8%

May

273.51

+0.4%

+5.2%

Jun

274.91

+0.5%

+5.0%

Jul

278.00

+1.1%

+5.4%

Aug

283.06

+1.8%

+7.6%

Sep

288.11

+1.8%

+9.4%

Oct

292.85

+1.6%

+11.5%

Nov

295.64

+1.0%

+12.3%

Dec

297.52

+0.6%

+13.0%

Jan ’21

301.72

+1.4%

+14.3%

Feb

310.62

+2.9%

+17.1%

Mar

320.81

+3.3%

+19.1%

Apr

331.47

+3.3%

+21.6%

May

341.05

+2.9%

+24.7%

Jun

349.78

+2.6%

+27.2%

Jul

355.33

+1.6%

+27.8%

Aug

357.11

+0.5%

+26.2%

Sep

359.88

+0.8%

+24.9%

Oct

363.80

+1.1%

+24.2%

Nov

367.62

+1.1%

+24.3%

Dec

374.48

+1.8%

+25.9%

Jan ’22

383.92

+2.5%

+27.2%

Feb

401.45

+4.6%

+29.2%

Mar

416.64

+3.8%

+29.9%

Apr

426.08

+2.3%

+28.5%

May

428.32

+0.5%

+25.6%

Housing data for May 2022 continued strong, as price gains decelerated slightly from very high levels,” says Craig J. Lazzara, Managing Director at S&P DJI. “The National Composite Index rose by 19.7% for the 12 months ended May, down from April’s 20.6% year-over-year gain. We see a similar pattern in the 10-City Composite (up 19.0% in May vs. 19.6% in April) and in the 20-City Composite (+20.5% vs. +21.2%). Despite this deceleration, growth rates are still extremely robust, with all three composites at or above the 98th percentile historically.

My guess is we’ll be 400+ at the end of the year, or about the same as February. A flat-pricing environment is the easiest of all the choices for buyers and sellers – just sell for the same amount as the last guy.

San Diego Non-Seasonally-Adjusted CSI changes

Observation Month

SD CSI

M-o-M chg

Y-o-Y chg

Jan ’20

264.04

+0.2%

+5.1%

Feb

265.34

+0.5%

+4.6%

Mar

269.63

+1.6%

+5.2%

Apr

272.48

+1.1%

+5.8%

May

273.51

+0.4%

+5.2%

Jun

274.91

+0.5%

+5.0%

Jul

278.00

+1.1%

+5.4%

Aug

283.06

+1.8%

+7.6%

Sep

288.11

+1.8%

+9.4%

Oct

292.85

+1.6%

+11.5%

Nov

295.64

+1.0%

+12.3%

Dec

297.52

+0.6%

+13.0%

Jan ’21

301.72

+1.4%

+14.3%

Feb

310.62

+2.9%

+17.1%

Mar

320.81

+3.3%

+19.1%

Apr

331.47

+3.3%

+21.6%

May

341.05

+2.9%

+24.7%

Jun

349.78

+2.6%

+27.2%

Jul

355.33

+1.6%

+27.8%

Aug

357.11

+0.5%

+26.2%

Sep

359.88

+0.8%

+24.9%

Oct

363.80

+1.1%

+24.2%

Nov

367.62

+1.1%

+24.3%

Dec

374.48

+1.8%

+25.9%

Jan ’22

383.92

+2.5%

+27.2%

Feb

401.45

+4.6%

+29.2%

Mar

416.64

+3.8%

+29.9%

Apr

426.08

+2.3%

+28.5%

Home price increases slowed ever so slightly in April, but it is the first potential sign of a cooling in prices.

Prices rose 20.4% nationally in April compared with the same month a year ago, according to the S&P CoreLogic Case-Shiller Index. In March, home prices grew 20.6%. The last slight deceleration was in November of last year.

The 10-city composite annual increase was 19.7%, up from 19.5% in March. The 20-city composite posted a 21.2% annual gain, up from 21.1% in the previous month.

In a change from the last five months, when most of the 20 cities saw month-to-month price gains, only nine cities saw prices rise faster in April than they had done in March. Cities in the South continued to see the strongest monthly gains, including Charlotte, North Carolina; Tampa, Florida; Atlanta, Dallas and Miami.

“April 2022 showed initial (although inconsistent) signs of a deceleration in the growth rate of U.S. home prices,” Craig Lazzara, managing director at S&P DJI, wrote in a release. “We continue to observe very broad strength in the housing market, as all 20 cities notched double-digit price increases for the 12 months ended in April. April’s price increase ranked in the top quintile of historical experience for every city, and in the top decile for 19 of them.”

Tampa, Miami and Phoenix continued to lead the pack with the strongest price gains. Tampa home prices were up, with a stunning 35.8% year-over-year price increase, followed by Miami, with a 33.3% increase, and Phoenix, with a 31.3% increase. Nine of the 20 cities reported higher price increases in the year ending April 2022 versus the year ending March 2022.

Cities with the smallest gains, although still in double digits, were Minneapolis, Washington and Chicago.

Not only are these price gains for April, but the index is a three-month moving average. The average rate on the 30-year fixed mortgage just crossed the 5% mark in April after rising from around 3% in January. By June it had crossed 6%.

“We noted last month that mortgage financing has become more expensive as the Federal Reserve ratchets up interest rates, a process that had only just begun when April data were gathered,” said Lazzara. “A more challenging macroeconomic environment may not support extraordinary home price growth for much longer.”

The housing market is already cooling, with slower sales and reports of price drops among some sellers. The supply of homes for sale has also increased steadily, as more listings come on the market and homes already on it sit longer. Active inventory last week was 21% higher than it was the same week one year ago, according to Realtor.com.

“For buyers and sellers, the road ahead will require more flexibility in pricing, brushing up on negotiation skills, and acknowledging that market conditions today are different than even six months ago,” said George Ratiu, senior economist at Realtor.com.

Mortgage rates didn’t get into the fives until early April, and up until then, the frenzied-out buyers were grabbing something at any price. The June index will show the full effect, which we’ll get at the end of August.

San Diego Non-Seasonally-Adjusted CSI changes

Observation Month

SD CSI

M-o-M chg

Y-o-Y chg

Jan ’20

264.04

+0.2%

+5.1%

Feb

265.34

+0.5%

+4.6%

Mar

269.63

+1.6%

+5.2%

Apr

272.48

+1.1%

+5.8%

May

273.51

+0.4%

+5.2%

Jun

274.91

+0.5%

+5.0%

Jul

278.00

+1.1%

+5.4%

Aug

283.06

+1.8%

+7.6%

Sep

288.11

+1.8%

+9.4%

Oct

292.85

+1.6%

+11.5%

Nov

295.64

+1.0%

+12.3%

Dec

297.52

+0.6%

+13.0%

Jan ’21

301.72

+1.4%

+14.3%

Feb

310.62

+2.9%

+17.1%

Mar

320.81

+3.3%

+19.1%

Apr

331.47

+3.3%

+21.6%

May

341.05

+2.9%

+24.7%

Jun

349.78

+2.6%

+27.2%

Jul

355.33

+1.6%

+27.8%

Aug

357.11

+0.5%

+26.2%

Sep

359.88

+0.8%

+24.9%

Oct

363.80

+1.1%

+24.2%

Nov

367.62

+1.1%

+24.3%

Dec

374.48

+1.8%

+25.9%

Jan ’22

383.92

+2.5%

+27.2%

Feb

401.45

+4.6%

+29.2%

Mar

416.64

+3.8%

+29.9%

“Those of us who have been anticipating a deceleration in the growth rate of U.S. home prices will have to wait at least a month longer,” says Craig Lazzara, managing director at S&P DJI. “All 20 cities saw double-digit price increases for the 12 months ended in March, and price growth in 17 cities accelerated relative to February’s report.”

The expectation is that prices will begin to ease, since home sales have been falling now for several months. Demand, however, is still high, and real estate agents report that they are still seeing multiple offers for homes that are priced well. More supply is also coming on the market, as sellers worry they will miss out on the last days of the hot market.

“Mortgages are becoming more expensive as the Federal Reserve has begun to ratchet up interest rates, suggesting that the macroeconomic environment may not support extraordinary home price growth for much longer. Although one can safely predict that price gains will begin to decelerate, the timing of the deceleration is a more difficult call,” added Lazzara.

In recent weeks, the housing market has shifted, said Danielle Hale, chief economist for Realtor.com. “As buyer confidence sags and weighs down demand, real estate markets will re-balance, eventually tilting away from the heavy advantage that recent home sellers have enjoyed.”

(The San Diego seasonally-adjusted index was 416.51)

The February month-over-month increase was the highest ever, but it feels like ancient history:

San Diego Non-Seasonally-Adjusted CSI changes

Observation Month

SD CSI

M-o-M chg

Y-o-Y chg

Jan ’20

264.04

+0.2%

+5.1%

Feb

265.34

+0.5%

+4.6%

Mar

269.63

+1.6%

+5.2%

Apr

272.48

+1.1%

+5.8%

May

273.51

+0.4%

+5.2%

Jun

274.91

+0.5%

+5.0%

Jul

278.00

+1.1%

+5.4%

Aug

283.06

+1.8%

+7.6%

Sep

288.11

+1.8%

+9.4%

Oct

292.85

+1.6%

+11.5%

Nov

295.64

+1.0%

+12.3%

Dec

297.52

+0.6%

+13.0%

Jan ’21

301.72

+1.4%

+14.3%

Feb

310.62

+2.9%

+17.1%

Mar

320.81

+3.3%

+19.1%

Apr

331.47

+3.3%

+21.6%

May

341.05

+2.9%

+24.7%

Jun

349.78

+2.6%

+27.2%

Jul

355.33

+1.6%

+27.8%

Aug

357.11

+0.5%

+26.2%

Sep

359.88

+0.8%

+24.9%

Oct

363.80

+1.1%

+24.2%

Nov

367.62

+1.1%

+24.3%

Dec

374.48

+1.8%

+25.9%

Jan ’22

383.92

+2.5%

+27.2%

Feb

401.45

+4.6%

+29.2%

“U.S. home prices continued to advance at a very rapid pace in February,” says Craig J. Lazzara, Managing Director at S&P DJI. “The National Composite Index recorded a gain of 19.8% for the 12 months ended February 2022; the 10- and 20-City Composites rose 18.6% and 20.2%, respectively. All three composites reflect an acceleration of price growth relative to January’s level.

“The macroeconomic environment is evolving rapidly and may not support extraordinary home price growth for much longer. The post-COVID resumption of general economic activity has stoked inflation, and the Federal Reserve has begun to increase interest rates in response. We may soon begin to see the impact of increasing mortgage rates on home prices.”

(The San Diego seasonally-adjusted index was 404.45)

The prognosticators said prices would soften in 2022, but instead they have ‘reaccelerated’. Now the guessers are expecting the higher mortgage rates to slow down the runaway train – see below.

San Diego Non-Seasonally-Adjusted CSI changes

Observation Month

SD CSI

M-o-M chg

Y-o-Y chg

Jan ’20

264.04

+0.2%

+5.1%

Feb

265.34

+0.5%

+4.6%

Mar

269.63

+1.6%

+5.2%

Apr

272.48

+1.1%

+5.8%

May

273.51

+0.4%

+5.2%

Jun

274.91

+0.5%

+5.0%

Jul

278.00

+1.1%

+5.4%

Aug

283.06

+1.8%

+7.6%

Sep

288.11

+1.8%

+9.4%

Oct

292.85

+1.6%

+11.5%

Nov

295.64

+1.0%

+12.3%

Dec

297.52

+0.6%

+13.0%

Jan ’21

301.72

+1.4%

+14.3%

Feb

310.62

+2.9%

+17.1%

Mar

320.81

+3.3%

+19.1%

Apr

331.47

+3.3%

+21.6%

May

341.05

+2.9%

+24.7%

Jun

349.78

+2.6%

+27.2%

Jul

355.33

+1.6%

+27.8%

Aug

357.11

+0.5%

+26.2%

Sep

359.88

+0.8%

+24.9%

Oct

363.80

+1.1%

+24.2%

Nov

367.62

+1.1%

+24.3%

Dec

374.48

+1.8%

+25.9%

Jan ’22

383.92

+2.5%

+27.2%

Our 383.92 is the non-adjusted; the seasonally adjusted index was 389.19 in January! From cnbc:

After cooling off ever so slightly toward the end of last year, home price gains reaccelerated in January.

Home prices nationally rose 19.2% year-over-year in January, up from 18.9% in December, according to the S%P CoreLogic Case-Shiller Index. The 10-city Composite annual increase was 17.5%, up from 17.1% in the previous month. The 20-city composite rose 19.1%, up from 18.6% in December.

Phoenix, Tampa and Miami saw the biggest annual gains at 32.6%, 30.8% and 28.1%, respectively. Sixteen of the 20 cities reported higher price increases in the year ending January 2022 versus the year ending December 2021.

Washington, D.C., Minneapolis and Chicago saw the smallest annual gain, although they were all still up double digits from a year ago.

Tight supply and strong demand appear to be outweighing rising mortgage rates, which would usually take some of the heat out of housing.

While the index is a three-month running average, mortgage rates began to climb in January. The average rate on the 30-year fixed ended 2021 at around 3.25% and ended January at 3.68% according to Mortgage News Daily. It is now flirting with 5%.

“The macroeconomic environment is evolving rapidly. Declining COVID cases and a resumption of general economic activity has stoked inflation, and the Federal Reserve has begun to increase interest rates in response. We may soon begin to see the impact of increasing mortgage rates on home prices,” said Craig Lazzara, managing director at S&P Dow Jones Indices.

Higher mortgage rates have already started to affect sales in the first months of the year. Pending home sales, which measure signed contracts on existing homes, have now fallen for four straight months, according to the National Association of Realtors.

“The monthly payment for a median-priced home has jumped 30% in the past year, far outpacing even fast-rising consumer prices, up almost 8% from a year ago,” said George Ratiu, senior economist at Realtor.com in a release. “While the small number of homes-for-sale will keep upward pressure on prices as we move through the Spring buying season, I expect conditions to undergo noticeable adjustments in the months ahead.”

It’s early, and the final February sales count will probably wind up around 165-170, which is in line with years prior to 2021. However, the pricing is nuts – and related to the number of homes for sale!

Year

February Listings

# of Sales

Median List Price

Median Sales Price

Median DOM

2017

395

172

$1,299,900

$1,270,000

51

2018

358

162

$1,290,000

$1,275,000

13

2019

361

174

$1,275,000

$1,275,000

33

2020

360

184

$1,434,000

$1,376,500

29

2021

313

224

$1,719,500

$1,758,000

14

2022

193

156

$2,149,500

$2,386,500

9

LAST MONTH, THE MEDIAN SALES PRICE WAS 11% HIGHER THAN THE MEDIAN LIST PRICE!