Q. The seller told me that when he bought the property seven years ago there were drainage, soils and foundation issues. He said he has fixed everything and there have been no issues or problems during his ownership. He said because he fixed everything there is nothing to disclose to a buyer. Is that correct?

A. No. Past defects, even if repaired by the seller or others, are to be disclosed. Not only that the seller should provide all relevant information regarding the repairs to any prospective buyer but also any improvements or modifications. The information would include but not limited to the person(s) who performed the repairs (i) the property owner (ii) a licensed contractor (iii) an unlicensed tradesman (iv)all paperwork related to the repairs/improvements/modifications to the property.

In addition, the new “Flipper Law (AB 968)” which will become law July 1, 2024, means a seller of a residential one-to-four property who accepts an offer within 18 months from the date when title was transferred must make the following disclosures: 1) The seller must disclose repairs and renovations when performed by a contractor with whom the seller entered into contract; 2) the name of each contractor and their contact information; and 3) any permits obtained (or if not obtained, the contact information of the third party who can provide the permits). It happens regularly that sellers do improvements without obtaining proper permits, so double-check at the city or county to verify.

Hopefully the hubbub about realtors’ pay will cause consumers to investigate agents more thoroughly, which I’ve been encouraging for a while. Here’s one of my blog posts from 2009 – check the comment section too:

by Jim the Realtor | Jul 24, 2009 | Thinking of Buying? | 34 comments

Most buyers struggle to find a quality realtor to assist them in buying a house, and it’s the realtors’ fault. The national, state, and local associations are so adamant about protecting the new agents and giving everyone an equal chance, that they provide no help whatsoever to the general public.

Their message? When trying to find good help, you’re on your own.

So how do you get what you need?

Everyone tells you to ask around, get referrals from friends, go to open houses, go with a big company, go with a small company, new agent, old agent, kickbacks, etc., that it probably doesn’t matter where you get a realtor, what matters is how to evaluate them.

Here are my things to look for when evaluating a realtor’s ability to help you buy a house:

1. ASK ABOUT THEIR RECENT TRACK RECORD OF SALES – Let’s cut to the chase, shall we?

Has the agent been able to successfully guide others to the finish line this year? The best answer is 1-2 closings per month, if you want an agent who delivers personal service. Any agent who sells four or more per month is slamming people into houses, and those at zero, well let’s face it, they don’t have anything of value to add to the equation. Get a testimonial from a past client, and/or at look at the sales they’ve done and judge them to see if they were good deals. (I’ve assisted 10 buyers with closing their sale this year).

These current market conditions are unlike any seen before. If your agent has been closing some buyer transactions this year, they must have something of value to share. Here’s what to look for:

2. ASK THEM, “WHAT/WHERE ARE TODAY’S HOT BUYS? How they answer that will tell you just about everything you need to know. If they give you a smart-aleck answer, they probably aren’t the right agent for you, only because they aren’t in the game. If they can name one, at least they are looking at properties, and those are agents who can provide value – ideally your buyer’s agent is previewing property every day, in person.

3. THEY SHOULD ASK YOU QUALIFYING QUESTIONS – If they jump in the car without asking questions, their time must not be too value to them, and this isn’t a business where wasting a lot of your time makes for good quality realtors.

4. THEY SHOULD KNOW ABOUT FINANCING – I guess it’s alright if they just hook you up with their lender to get pre-qualified, but if they can ask/answer the qualifying questions themselves, it might help when it comes time to structure an offer.

5. HAVE THEM SHOW YOU SOME HOUSES – Go in their car, and if they don’t need a map to get around, you’ve found an experienced veteran. It’s not guaranteed that they can help, nor is it required, but it’s a good indicator. If they are pointing out specific sales/listings along the way (theirs or others), then they know the comps too, which is another great indicator.

6. EVALUATING THE PROPERTY’S CONDITION – They don’t have to be a general contractor, but they should be able to educate you about the property’s condition. If all they do is point out that “This is the living room”, they’re not going to have much to offer in terms of added value, unless you don’t know what a living room is.

7. HAVE A VENDOR’S LIST – Successful agents know professionals to call to fix stuff – the more thorough the list, the more problems they have encountered.

8. DO THEY CHARGE FOR THEIR SERVICE? – Ask about “transaction fees”, “processing fees”, or “compliance fees”. These are junk fees used to pad their bottom line, and are not required.

9. DO THEY INSIST ON HAVING YOU SIGN A BUYER-BROKER AGREEMENT? – Pass on those, unless you got married after having one conversation too.

10. “FORECLOSURE SPECIALIST” – Be very leery – we are all foreclosure specialists now. Any agent who tries to make it sound like they have some special “foreclosure ability” is blowing smoke, unless they are listing REOs and not putting them on the open market. If they don’t mind breaching their fiduciary duty to their bank-seller, they’ll sell you down the river in a heartbeat.

11. SHORT SALES – I personally see 2-3 short sales every day that have already found their buyer before MLS input, and it is VERY frustrating. These agents don’t care about their own reputation amongst their peers, and that alone should make you wonder.

12. OFF-THE-GRID – Ask about what agents can do to find properties that aren’t on the regular websites. Any positive response would be a good indicator, and any examples of closing one would be even better.

If they can get through those questions and you still like them, you found a good agent!

NEW AGENTS – A new agent’s zeal and availability can really help buyers who don’t have the time or willingness to search for properties themselves. Want somebody to do the legwork for you? Put a new, hungry agent on it, but there may be some struggle clinching the deal if there are competing offers.

OUT-OF-COUNTY AGENTS – You’ll be doing all the work yourself, so your own proficiency in being a realtor needs to be up to par.

RELATIVES – Many deals crash and burn, and hearts are broken over houses. Want a relative to help you? Make sure that you’ll accept never wanting to talk to them if they cost you the right house, at the right price.

“GREAT TIME TO BUY” – If you hear that catchy phrase, just walk away.

The inventory of quality homes at good prices is EXTREMELY LOW, causing the buying experience to be full of frustration and disappointment. You can look for weeks or months without seeing anything attractive, so I don’t know why any agent would call that a great time.

REALTOR TEAMS – No problem, but don’t interview the big dog and then get passed off to the assistant without asking the same questions. You want to be clear about who is helping you, and what you can count on. In my case, I may have Richard or another KR realtor help me on occasion, but I’m still the main person in charge, and am responsible for your success.

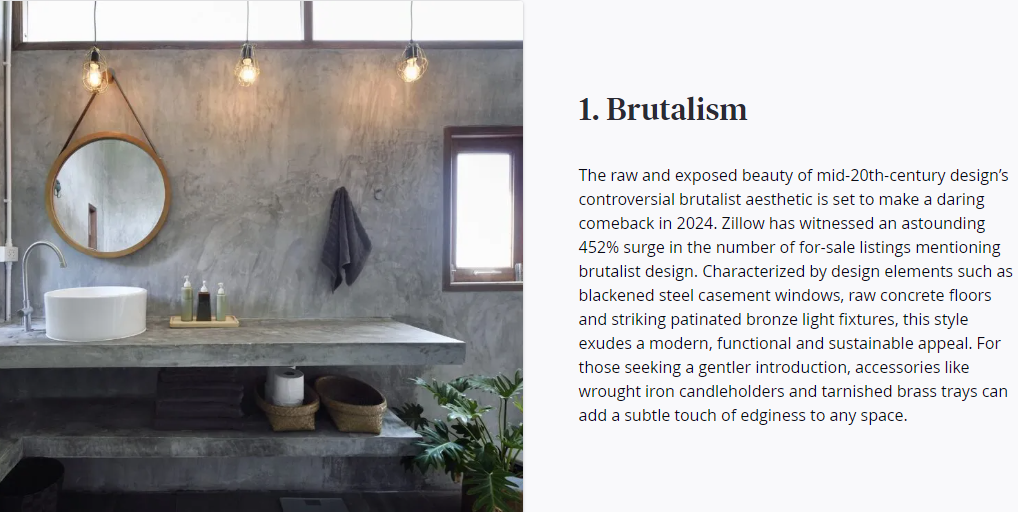

You can get ahead of the curve on the hottest new home design trends by checking out our predictions of which features and design elements will be trending in 2024.

We looked at nearly 300 home features and design styles mentioned in for-sale listing descriptions on Zillow and then identified the keywords showing up more frequently than they did a year ago. From post-pandemic pastimes to nostalgic designs from decades past, Zillow identified the emerging trends of 2024:

Houses are getting bigger overall, but that doesn’t mean a larger house is right for you.

“Fit is super important, and people get complacent and they don’t think about if their home is still fitting them,” says Marni Jameson Carey, a home and lifestyle expert, author of “Downsizing the Family Home: What to Save, What to Let Go,” and president of Power to the Patients, a nonprofit organization.

Here are four signs your home may be bigger than you need or can handle.

There are rooms you haven’t spent time in for weeks.

You haven’t furnished the whole house.

The property taxes are too much for you.

Most of the stuff belongs to people who’ve moved away.

And here are four things you can do about it:

Reach out to a professional.

Stay in a short-term rental for a while.

Consider all your needs.

Don’t just downsize your home.

There Are Rooms You Haven’t Spent Time in for Weeks

A four-bedroom McMansion may have once been perfect for a house full of teenagers and hosting extended family for the holidays, but now all but your own bedroom is a guest room and you no longer host Thanksgiving for the family.

“You’re overheating spaces that don’t need to be heated at all because you’re not using them,” says Eric Stewart, CEO and associate broker of the Eric Stewart Group of Long & Foster Real Estate in the District of Columbia metro area. “I think it’s the slow realization that the house owns you more than you own the house.”

You Haven’t Furnished the Whole House

Whether you don’t need a room or can’t afford to put furniture in it yet, the fact that your furniture choices can’t match the house you bought may be a sign it’s not the right real estate fit.

“Plastic chairs on a patio on an $800,000 house, and you go, ‘What happened here?’” Carey says.

If you’ve lived in the house more than a few months and you’ve left entire rooms bare, ask if you’re ever going to take full advantage of the total square footage you own. If you see it as unlikely, consider “right-sizing” your property to fit with your lifestyle as well as your wallet.

The Property Taxes Are Too Much for You

You can deduct your state and local property taxes up to $10,000 from your itemized federal tax filing, but for many homeowners that still means they’ve got a few thousand dollars to pay without annual relief.

If the limit on property deductions isn’t enough and means you’re financially strapped, you should rethink the home you own. Consider whether the location outweighs your ability to pay other expenses, and look at alternative cities or neighborhoods that might be able to provide the life you desire without the excessive costs currently tied to it.

Most of the Stuff Belongs to People Who’ve Moved Away

A classic empty nester problem is having all your kids’ belongings spanning from birth to college – and even beyond – with no real use for any of it. Trying to get your adult children to decide between keeping their macaroni art from first grade at their own house and letting you toss it can be tough for both sides, but keep in mind that your home shouldn’t be used as a storage unit.

Carey says, when given a certain amount of space, most people will naturally fill it up with belongings. In the case of empty nesters, that space is often filled with memorabilia that ultimately does not provide enough sentimental value to anyone to be kept. Put your foot down and have your kids come by to clean up and take what they would like to keep.

Even if you’d like to stay in your home in the long run, it’s important to regain control of the property when others stop living there. The worst-case scenario is realizing you need a smaller house or need to move to where you can get more care but feel overwhelmed by the task of clearing out the house. “Don’t be there as a default – be there by choice,” Carey says.

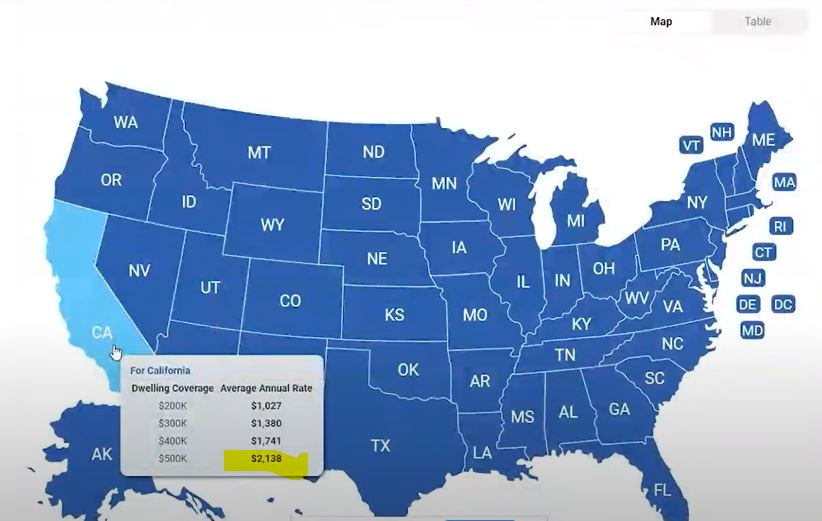

Currently buyers are having to pay 2x or 3x the previous bill for homeowners insurance, due to the lack of options because the big insurance companies have stopped writing policies in California. Some are blaming climate change, and guys like Carl Demaio are blaming Biden, but with a little digging it looks like the insurance-companies requests to raise premiums have been stalled for years. California’s average home insurance rate is $1,225 per year for $250,000 in dwelling coverage is about 14% lower than the US average, according to Bankrate. The thought of insurance premiums being 30% higher sure sounds better than 2x or 3x!

Full story from the LAT:

After a summer that saw many of California’s top home insurers pull back from the state market, Insurance Commissioner Ricardo Lara announced Thursday that he struck a deal with the insurance industry to encourage new coverage in the state.

Insurers, Lara said, agreed to return to the high-risk fire zones in the state in exchange for a number of concessions that will make it easier, in theory, for them to get higher rate increases through the state regulator more quickly. The announcement comes the week after negotiations in Sacramento over a legislative response to the home insurance market fell apart.

Gov. Gavin Newsom also issued an executive order on Thursday afternoon commanding the insurance commissioner to “take prompt regulatory action to strengthen and stabilize California’s marketplace” and consider whether emergency action could be necessary.

The changes are slated to go into effect by the end of 2024, but the hope is that insurers will return to writing new homeowners policies in California sooner. Leading insurers such as State Farm, USAA and Allstate all have requests for rate increases pending with the state insurance department, and are requesting hikes of 28.1 percent, 30.6 percent and 39.6 percent, respectively.

If approved, each company would be allowed to raise its total premiums in the state by that amount, but the rate increase can be distributed differently among homeowners: a cabin in the woods might see a 200 percent jump while a home in San Francisco could see little to no change.

Many who own a two-story home wonder if there is a reasonably-priced elevator they can install once their knees start to give out. This is the best value I’ve seen, though I still recommend moving instead!

Many Americans will save thousands of dollars on home renovations when new rebates for a range of energy-efficient upgrades kick in later this year.

Buyers will receive the rebates as part of a $9 billion federal program passed by Congress in last summer’s Inflation Reduction Act. Household savings can range from hundreds of dollars for single items such as an electric cooktop or dryer to $8,000 for a heat pump or cutting home energy use by 35% or more. Those planning such projects may want to hold off until the program begins.

The size of the rebates will vary based on your household income and where you live, since the program will be administered separately by each state.

States will announce the particulars in coming months, based on guidelines issued by the Energy Department in July. These rebates can also be stacked on top of existing tax credits and utility offers for heat pumps, solar and EVs, said Kara Saul-Rinaldi, a clean-energy policy strategist in Washington, D.C. The new rebate programs and enhanced tax credits are good through 2032.

Tax credits for greening your house are available now. Tax savings for a home energy audit: up to $150.

Install rooftop solar and add battery storage to create your own power plant. Tax savings: 30% of the cost of the system. Add insulation and/or more energy-efficient windows and doors. Tax savings: up to $1,200. Replace an old air conditioner and a gas furnace with an electric heat pump that does double duty, heating and cooling. Tax savings: up to $2,000. Drive an electric vehicle and install a home charging station. Tax savings: Up to $7,500 for a new vehicle, up to $4,000 for a used vehicle, and up to $1,000 for the charger. Income limits apply.

Every coastal home has termite damage, and every seller would be smart to identify the cost before selling. There is usually a wide varance in costs quoted – we use our qualified vendors who don’t charge a premium rate and let our volume work for you. Here the cost was $8,345 for wood repair all around and fumigation:

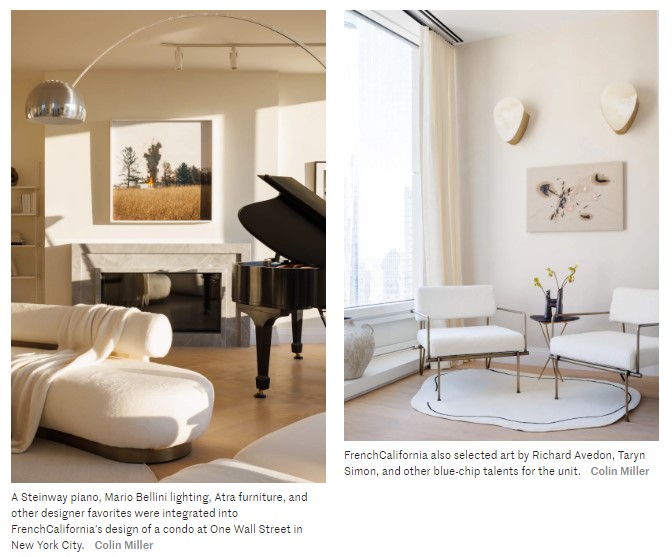

The thought of buying a home that is truly move-in ready would be a natural fit for today’s home buyers. Our staging company is willing to sell everything they use to decorate our listings!

Developers frequently stage properties, giving potential buyers insight into what living there might actually be like. But these days, the trend is toward selling residences fully furnished, right down to the Frette sheets and Lavazza espresso maker. For well-heeled clients, these “instant homes” offer the ultimate in convenience, with the added caché of a big-name designer.