For people who have been considering selling, it might not be necessary to wait. One benefit of Americans being home all day is that they are online all day long. ALL DAY.

I’m online while I’m typing this. My screen time on my iPhone is up to embarrassingly high numbers. I’m literally averaging 14 hours a DAY on my phone.

Eventually, we will all find a way to a real estate site, or at least search homes on Instagram. It’s inevitable, kind of like those cookies in your pantry are going to get eaten by the time you’re done reading this article.

The most unconventional aspect of this new age real estate industry is the fact that touring homes is currently impossible, as it should be. I’ve taken a hard stance for ALL OF US to STAY HOME for almost a month. Ironically, people are staying home – as they should be.

Prospective buyers will most likely remain hesitant to buy before they can physically tour a home but we can all pivot and redefine the way we work.

The minute that people are legally allowed to take a physical tour, the market is going to boom. It’s like when the new iPhone comes out. We want and expect lines out the door, just no tents, please.

People will be lined up at the doors of those homes they have obsessed over for months.

In the meantime, real estate professionals are utilizing virtual tours to keep buyers excited, and it is working, and relationships are getting back to the core — the heart.

We are entering what is usually the busiest season of real estate, that usually lasts through the end of the summer. I am confident that the busy season will last through the fall, and possibly through the winter.

Momentum is building, so there is no need to fear putting your home on the market.

Now is our chance to build and maintain confidence in the real estate market, because as soon as our world begins to shift back into normalcy, the market will be at its height.

We’ve all heard this a million times over, but right now, it’s more true than ever — home is where the heart is. You may not love where you currently are, but we know you love who you’re currently with. Get online, shop for your new forever place, and get excited about something that’s going to be there when this nightmare ends.

In the meantime, stay home, technology has us covered.

Interview with Ryan Serhant about the market and what to do:

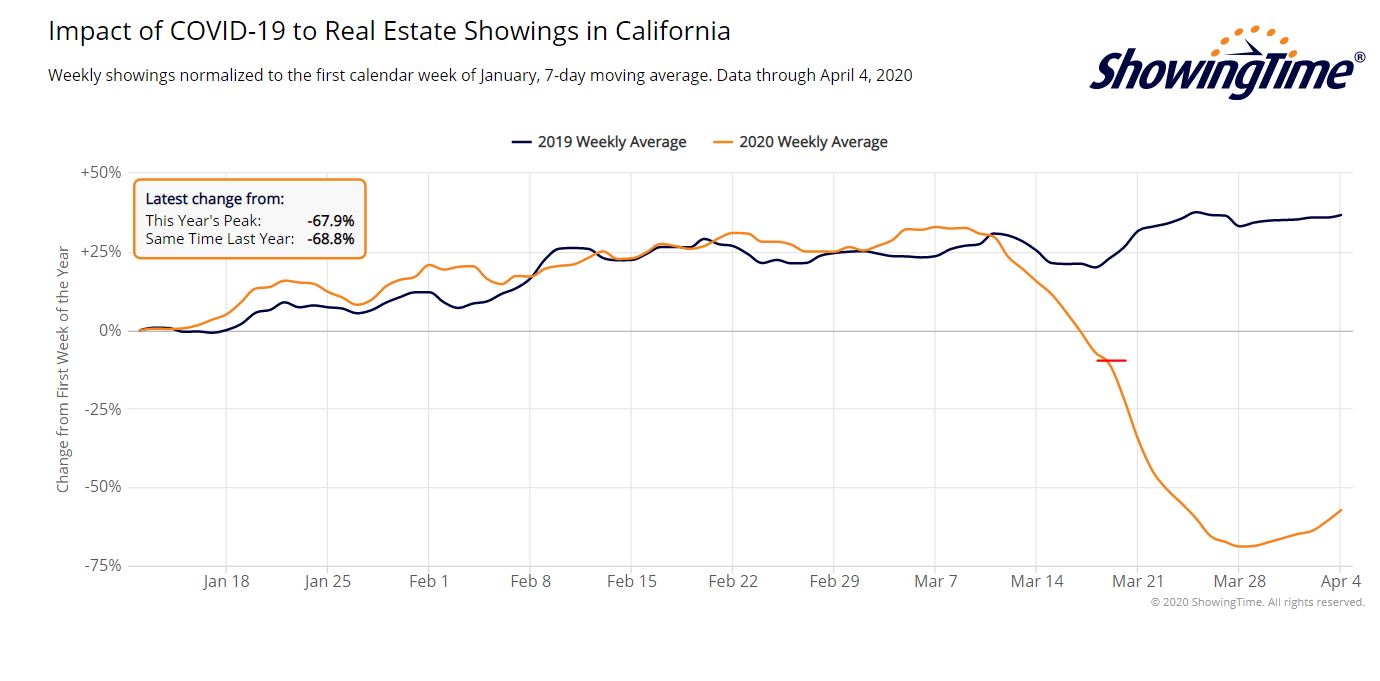

The governor’s stay-at-home order was issued on March 19th (red line), but showings had already been dropping steadily. Realtors were changed to essential workers on March 28th, but it doesn’t look like agents rushed back to work. The weekly average improved from -68.9% on the 28th to -57.3% yesterday. At least it’s heading in the right direction – we’d like to avoid a complete meltdown if possible.

On average it probably takes at least 2-3 showings minimum to procure a sale. Some homes sell after the first showing, and other take many more visits so averaging 2-3 before finding a buyer is optimistic – but in this era only the highly-motivated buyers are looking in person.

As an essential worker on the street, let me bring you today’s freeway report for those who stay at home. As usual these days, I did not interact with one human being on my trip:

“Wealth is the vector.” That’s what sociologist Tressie McMillan Cottom tweeted last week, in reference to the spread of COVID-19 across both the globe and the United States.

Wealth is not the cause of every concentrated outbreak dotting the United States. But it’s the common denominator of so much of its spread outside of major urban areas. It’s the reason why so many of the coronavirus hot spots in the Mountain West — Sun Valley, Idaho; Gunnison County, Colorado; Summit County, Utah; Gallatin County, Montana — overlap with winter playgrounds for the wealthy. The virus travels via people, and the people who travel the most, both domestically and internationally, are rich people.

A party in the tony bedroom community of Westport, Connecticut, all the way back on March 5, became what one epidemiologist referred to as a “super-spreading event,” with infected attendees dispersing throughout Connecticut and New England, and one party-goer falling ill on a plane ride back to South Africa. In Idaho’s Blaine County, home to Sun Valley, more than half of the residential properties are second homes or rental properties, and more than 30,000 people fly into the regional airport during ski season alone. As of March 31st, 187 people in the county of 22,000 have tested positive, including local emergency room physician Brent Russell. Two people have died. The town’s small hospital has two ICU beds and a single ventilator.

“People come here from all over the world,” Russell told the Idaho Statesman. “Especially this time of year. When I’m in the ER, I get people from New York, Washington D.C., San Francisco, Seattle. Every week there’s people from those places. Most likely someone from an urban area or multiple people from urban areas came here and they just set it off.”

All over the United States, people are fleeing urban areas with high infection rates for the perceived safety and natural beauty of rural areas. Some of them own second homes in those areas; others are paying upwards of $10,000 a month, depending on the area, for temporary housing. The common denominator among those populations is, again, wealth — either their own or their families’. They can flee the city because their jobs can be done remotely, or they don’t work at all. They either had a vacation house already, or they can afford to fork over what amounts to a second rent, or second mortgage.

Not everyone leaving a big city because of the pandemic is heading for a vacation home; many people with mobile jobs are relocating to stay with family in suburban and rural hometowns. And many of the rural places that will eventually be hardest hit by the coronavirus are not upscale ski and beach towns, but small and often poor communities that have no tourist economy — or any of the infrastructure that comes with it. The resort areas seeing an influx of potentially virus-carrying city dwellers now are a kind of canary in the coal mine: a preview of how desperately overwhelmed rural areas across the country will be by the coronavirus, whenever it arrives.

From the coast of Maine to the North Shore of Lake Superior, hundreds of thousands of people have either already arrived or are scrambling to find vacant rentals. Some are taking precautions when they leave their primary dwellings, fully isolating themselves for 14 days or more in their new, temporary towns, as the White House has recommended for anyone leaving New York City. But many, presumably, are not.

“The worst part is that these second-home owners are coming up and acting like isolation is a vacation,” said Jen, 39, who lives in the northwest Colorado Rockies.

Millions of borrowers may be unable to pay their mortgages as the coronavirus continues to crush the U.S. economy. But there is a government back-up plan. The CARES Act just signed into law allows borrowers to skip payments for up to a year and then have those payments tacked on to the end of their loans.

There’s one hitch: the $2 trillion stimulus package states that borrowers need not provide any proof of financial hardship. They can simply say they can’t pay.

In an interview Wednesday, the chief regulator of mortgage giants Fannie Mae and Freddie Mac, FHFA Director Mark Calabria, begged borrowers to be honest.

“We’re operating on the honor system. We are asking and we’re putting together a script for servicers. This is supposed to be limited to if you’ve lost your job, you’ve lost income. Please, if you haven’t lost your job, continue paying. If you can pay your mortgage please do so because we really need to focus on the people who can’t.”

There will be some accountability: borrowers will have to provide documentation when they set up their repayment plans. Lying then would be considered fraud, a spokesperson for the FHFA said.

Calabria estimated that up to 2 million borrowers could be applying for loan forbearance by May and said that mortgage servicers, as well as Fannie and Freddie, could handle that if it was just for a few months. After that, there could be problems.

“If this goes beyond two or three months and we start to get worse than that, then that’s going to be a lot of strain, and certainly we’re going to start to see some firms get into a lot of liquidity trouble,” he added.

While the mortgage market was much healthier going into this crisis than it was going into the subprime mortgage crisis, there is still one very vulnerable area: FHA loans. These are low down payment loans to borrowers with lower credit scores, and they are insured by the federal government.

“The truth is that subprime really didn’t as much go away as it went into FHA, so you have a lot of FHA borrowers who I think are vulnerable. The real question is the duration of this,” Calabria said.

“If this is something that goes on for six months or more, then I think you’re going to continue to see a lot of stress, and I would really emphasize the place to look right now is the FHA market, with the credit quality of their borrowers,” he said. “They’re really going to be the first canary in the coal mine in terms of what the broader implications are going to be.”

Lenders won’t report late payments to credit bureaus! Hat tip to Susie:

SACRAMENTO – Governor Gavin Newsom today announced that financial institutions will provide major financial relief for millions of Californians suffering financially as a result of the COVID-19 outbreak.

“Millions of California families will be able to take a sigh of relief,” said Governor Newsom. “These new financial protections will provide relief to California families and serve as a model for the rest of the nation. I thank each of the financial institutions that will provide this relief to millions of Californians who have been hurt financially from COVID-19.”

Governor Newsom secured support from Citigroup, JPMorgan Chase, U.S. Bank, and Wells Fargo and nearly 200 state-chartered banks, credit unions, and servicers to protect homeowners and consumers.

Under the Governor’s proposal, Californians who are struggling with the COVID-19 crisis may be eligible for the following relief upon contacting their financial institution:

90-Day Grace Period for Mortgage Payments

Financial institutions will offer, consistent with applicable guidelines, mortgage payment forbearances of up to 90 days to borrowers economically impacted by COVID-19. In addition, those institutions will:

Provide borrowers a streamlined process to request a forbearance for COVID-19-related reasons, supported with available documentation;

Confirm approval of and terms of forbearance program; and

Provide borrowers the opportunity to request additional relief, as practicable, upon continued showing of hardship due to COVID-19.

No Negative Credit Impacts Resulting from Relief

Financial institutions will not report derogatory tradelines (e.g., late payments) to credit reporting agencies, consistent with applicable guidelines, for borrowers taking advantage of COVID-19-related relief.

Moratorium on Initiating Foreclosure Sales or Evictions

For at least 60 days, financial institutions will not initiate foreclosure sales or evictions, consistent with applicable guidelines.

Relief from Fees and Charges

For at least 90 days, financial institutions will waive or refund at least the following for customers who have requested assistance:

Mortgage-related late fees; and

Other fees, including early CD withdrawals (subject to applicable federal regulations).