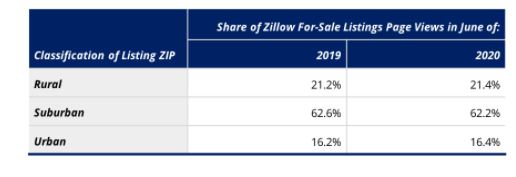

The chart above shows the June page views, which was probably the peak hysteria for those who were considering a drastic change. I think the heightened activity and sales could have just been from all the people who had been thinking about a move over the last 2-3 years, and they finally got on their horse. If we end up with about the same number of sales as last year, which looks probable, then sales were merely redistributed from April/May to late summer. Maybe a few more people left for the suburbs, but this report makes it look like it’s not a mass exodus.

From Zillow:

Are people fleeing the cities for greener suburban pastures?

Some faint signals may have emerged in certain places, but by and large, the data show that suburban housing markets have not strengthened at a disproportionately rapid pace compared to urban markets. Both region types appear to be hot sellers’ markets right now – while many suburban areas have seen strong improvement in housing activity in recent months, so, too, have many urban areas.

Zillow’s Economic Research team analyzed a variety of Zillow data points in order to illustrate this trend. Data related to for-sale listings are generally the best indicator of real-time housing market activity, and in all but a few cases, suburban markets and urban markets have seen similar changes in activity in recent months: about the same share of homes selling above their list price, similar changes in the typical time homes spend on the market before an offer is accepted, and recent improvements in newly pending sales have been about the same across each region type.

Other indicators also help drive home this conclusion. Changes in annual home value growth rates from just before the pandemic to now have been about the same for urban and suburban markets. In some regions where there is a divergence, the discrepancy can be explained by trends that were unfolding before the pandemic. Page view data also show that suburban home listings have not grown in relative popularity in the past few months. For-sale suburban homes attract more than three times as much of Zillow’s traffic as urban listings do, but that was the case last year as well. Interest in detached single-family homes (or similar) has not seen a marked increase in the past year, either.

For every tech platform that sets out to disrupt real estate, there’s a story of slow evolution to working with brokers and agents. And while companies like Zillow, Opendoor, and Offerpad have brought about minor changes to the home buying process, they always end up morphing into our traditional system. Why is it that these so-called disruptors just can’t change the way we do real estate?

In this episode of Industry Relations, Rob and Greg are exploring why would-be disruptors have such a hard time changing real estate. Greg walks us through his five-stages-of-grief analogy around how tech platforms always end up working with brokers and agents, and Rob compares real estate with the auto industry, reflecting on how little buying processes have changed despite advancements in technology.

Rob and Greg go on to introduce the idea that the human connection is what prevents tech disruptors from succeeding in our industry, speculating that agent teams have been the biggest disruptor in real estate in recent years. Listen in for insight on how human knowledge and connection factor into making tech platforms successful and learn why the human need for approval is not disruptable.

At least this was based on a survey, rather than ivory-tower speculation:

Where people choose to live has traditionally been tied to where they work, a dynamic that through the past decade spurred extreme home value growth and an affordability crisis in coastal job centers. But the post-pandemic recovery could mitigate or even produce the opposite effect and drive a boom in secondary cities and exurbs, prompted not by a fear of density but by a seismic shift toward remote work.

Now that more than half of employed Americans (56%) have had the opportunity to work from home, a vast majority want to continue, at least occasionally. A new survey from Zillow, conducted by The Harris Poll, finds 75 percent of Americans working from home due to COVID-19 say they would prefer to continue that at least half the time, if given the option, after the pandemic subsides.

Two-thirds of employees working from home due to COVID-19 (66%) would be at least somewhat likely to consider moving if they had the flexibility to work from home as often as they want. Only 24 percent of Americans overall say they thought about moving as a result of spending more time at home due to social distancing recommendations.

Many employed Americans are trying to square the desire to work remotely with the functionality and size of their existing homes. Among employees who would be likely to consider moving, If given the flexibility to work from home when they want, nearly one-third say they would consider moving in order to live in a home with a dedicated office space (31%), to live in a larger home (30%), and to live in a home with more rooms (29%).

A Zillow analysis finds 46 percent of current households have a spare bedroom that could be used as an office. But that percentage drops off by more than 10 points in dense, expensive metros such as Los Angeles, New York, San Jose, San Francisco and San Diego, where far fewer homes have spare rooms.

When it comes time to move, home shoppers who can work remotely may seek out more space — both indoor and outdoor — farther outside city limits, where they can find larger homes within their budget.

“Moving away from the central core has traditionally offered affordability at the cost of your time and gas money. Relaxing those costs by working remotely could mean more households choose those larger homes farther out, easing price pressure on urban and inner suburban areas,” said Zillow senior principal economist, Skylar Olsen. “However, that means they’d also be moving farther from a wider variety of restaurants, shops, yoga studios and art galleries. Given the value many place on access to such amenities, we’re not talking about the rise of the rural homesteader on a large scale. Future growth under broader remote work would still favor suburban communities or secondary cities that offer those amenities along with more spacious homes and larger lots.”

Zillow Premier Agents from Silicon Valley to Manhattan say anecdotally, they’re seeing the early beginnings of a shift.

“We are seeing more buyers looking to leave the city,” said Bic DeCaro, a member of Zillow’s Agent Advisory Board serving Washington, D.C., and Northern Virginia. “Buyers, who just a few months ago were looking for walkability, are now looking for extra land to go along with more square footage.”

Keith Taylor Andrews, a small business owner in Denver, started home shopping on Zillow the week Colorado issued a stay-home order. The first-time homebuyer is now under contract on a house in Fayetteville, Arkansas that he plans to use as his home office.

“We learned from COVID-19 that we could operate our business remotely,” said Andrews, who has 40 employees working from home. “Arkansas is a good place to move, it’s economical and there are far fewer people. It feels like a breath of fresh air to get out of the city.”

More of the same talk in this interview on how this crisis doesn’t compare to the last one, with a guess that October, 2020 will be the best month to buy:

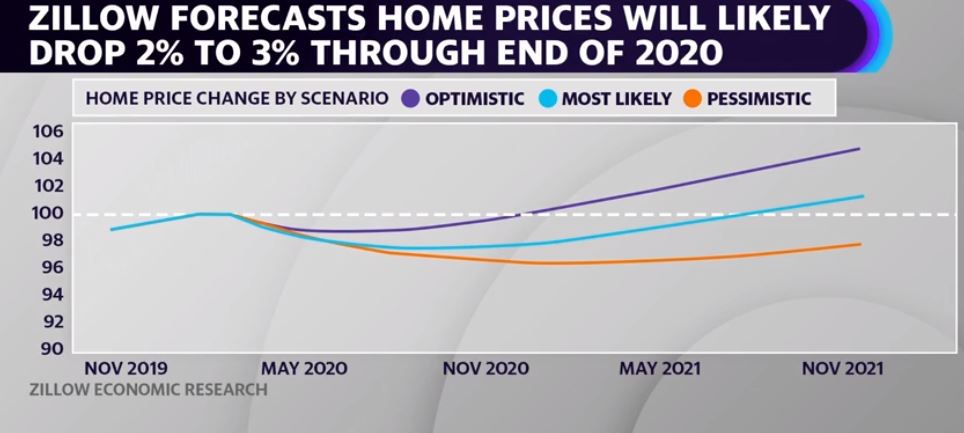

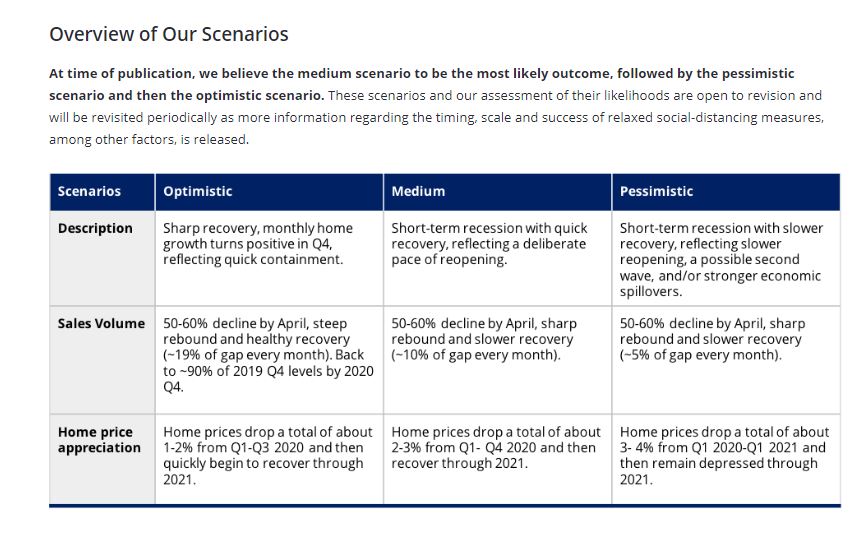

The continued economic fallout from the spread of COVID-19 has introduced immense uncertainty into the housing market as consumers step back from large purchases and social distancing puts a chill on necessary market services. As a result, Zillow expects home prices will most likely fall 2%-to-3% through the end of the year from pre-coronavirus levels, and home sales to fall as much as 60%, before both begin to slowly recover to baseline levels by the end of 2021.

The latest forecasts, based on published and proprietary macroeconomic and housing data, also include more pessimistic or optimistic projections based on the duration of the pandemic and the depth of its impact on the broader economy.

The forecasts center around a baseline prediction of a 4.9% decrease in United States GDP in 2020 and a subsequent 5.7% increase in 2021.

Under the baseline scenario, we expect:

A 2%-3% drop in prices through the end of 2020, followed by a slow recovery throughout 2021. Prices will return to Q4 2019 levels by Q3 2021.

A 50% decline in home sales from their pre-coronavirus levels, as measured at the end of 2019. Home sales will bottom out in Q2 before beginning to improve near the end of Q2 2020.

Sales volume will recover to about 97% of Q4 2019 levels by the end of 2021.

The pace of recovery is what distinguishes our three scenarios from one another.

Each of our scenarios implies very different paths for home prices and sales volumes. Our optimistic scenario features a small dip in house prices in Q2-Q3 followed by a robust recovery. The baseline medium scenario features a U-shaped trough in Q4 followed by a slower recovery and our pessimistic scenario features continued weakness through all of 2021 (more of a “long U” shape). Under our more-optimistic assumptions, the market could experience a fast, V-shaped “snapback”similar to what happened in the Hong Kong real estate market after the 2003 SARS outbreak. The medium scenario features a “check-mark” shaped recovery and our pessimistic scenario features more of a “wide-U” recovery, with a longer bottom and more gradual pace of improvement.

Spencer Rascoff, the co-founder and former CEO of Zillow, has put his Brentwood Park estate on the market for $24 million, according to Redfin. The asking price is $7 million over the “Zestimate,” or Zillow’s appraisal of what the home is worth.

Property records show that Rascoff paid $19.7 million for the property in 2016.

The listing states that the 12,700-square-foot home – remodeled by architects Ken Ungar and Steve Giannetti – is located on a half acre in a gated neighborhood. The Zillow Zestimate for the house suggests it’s worth $16.7 million.

Rascoff purchased the house from investment banker Michael J. Richter, who reportedly paid $9.3 million for the Parkyns Street manse in 2012.

The home has six bedrooms and nine bathrooms, along with a “spectacular” chef’s kitchen, a state-of-the-art theater with stadium seating, a fitness studio and a large master suite with a large balcony. The estate also features a two-bedroom guest wing, a motor court, and a spa, pool and mudroom.

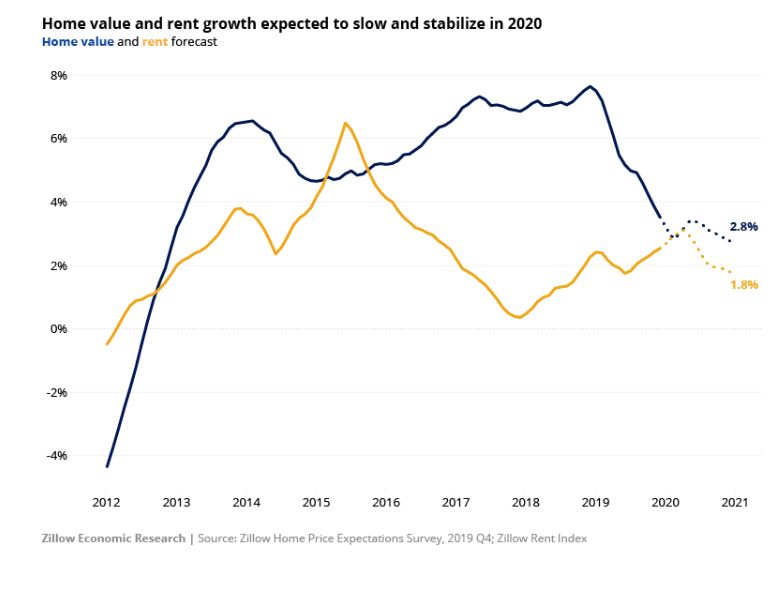

With the housing market stabilizing from the drama of the early years of home price recovery and the subsequent slowdown during 2019’s home shopping season, we have a rare moment of calm to reflect on what housing might look like in the year to come.

If current trends hold, then slower means healthier and smaller means more affordable. Yes, we expect a slower market than we’ve become accustomed to the last few years. But don’t mistake this for a buyer-friendly environment – consumers will continue to absorb available inventory and the market will remain competitive in much of the country.

But while the national story is a confident one, housing in some manufacturing-heavy markets may see adversity. The struggle could be even more stark, since similarly affordable housing markets with a more balanced job profile may be 2020’s rising stars.

There are several 50,000-foot reasons why we expect this gentle downsizing to continue:

Many of today’s younger, millennial home buyers have expressed a preference for denser, more urban homes that are more walkable to shared amenities.

Younger buyers are struggling to afford large homes built in prior decades

Eco-consciousness is also growing broadly.

Today’s older homeowners are expressing a desire for smaller, less maintenance-heavy and more accessible (read: fewer stairs) homes as they age and move into newer homes. In 2019, 56% of new construction home buyers were 40 or older, according to the 2019 Zillow Group Consumer Housing Trends Report.

Home builders are constrained by a shortage of buildable land in desirable areas. Prices on key building materials including lumber and steel are increasingly volatile. And competition for skilled construction labor is fierce, pushing wages up.

Each of these trends points to a continuation of this downsizing of new homes – smaller homes are inherently more dense, walkable and affordable; smaller homes are efficient and eco-friendly; smaller homes require less maintenance and are more accessible; smaller homes enable builders to do more with less.

There will always be demand for large, suburban homes on big lots – but on net, we expect attitudes to shift away from that and toward a lifestyle with a smaller footprint.

Mortgage Rates Will Stay Low, Keeping Housing Demand High

Mortgage rates fell markedly in 2019, and are expected to remain near their current, relatively low levels for the bulk of 2020. Softening GDP growth and investment, continued global weakness due in part to the U.S.-China trade conflict, and below-target inflation will continue to hold rates in check. Barring marked improvements in these indicators, the Fed will have no reason to return to rate hikes.

If low mortgage rates persist, this will keep home purchase demand strong and continue to fuel decent price growth in the nation’s most broadly affordable markets. But low rates won’t be enough to reignite high growth rates in the nation’s highest-priced markets, notably on the West Coast and in the Northeast. In these markets, buyers seem to have hit an affordability ceiling where even low rates can’t bring many homes into the typical first-time buyer’s budget range, especially because low rates don’t help overcome the upfront hurdle of high down payment requirements. In those high-priced markets, buyers will continue to fan out in search of more affordable areas.

Looking ahead at 2020, we think home sales will continue to climb, but slowly. Why?

Although a small fraction of overall sales, new homes sales grew significantly in 2019. That has helped buoy builder confidence and lead to some of the most robust permit and starts numbers in a long time.

If builders in 2020 deliver on their promises to build smaller and at more affordable price points, new construction will continue to be attractive to buyers unable to find a match in the competitive and limited existing home market.

Yes, inventory is tight – but when we say that, we’re really talking about the number of homes available to buy relative to demand from buyers. Sales can remain strong while inventory remains tight – and a sudden jump in the number of sales will result in a corresponding drop in inventory.

What really matters is the flow of homes onto the market – the turnover or velocity of home sales, not months’ supply or overall level of available inventory, that constrains home sales numbers.

And we have reason to believe that turnover among a given segment of homeowners will be made more possible now in a way that it wasn’t before. iBuyer business models, like Zillow Offers, are ultimately about lowering sellers’ transaction costs. Economics 101 says that lowering transaction costs and making transactions themselves easier will mean those transactions will happen more often.

Hat tip to RK for sending in this article – an excerpt:

I asked a realtor there that I know to do a CMA on the property. When she was done, her number came out to $460,000. Zillow’s offer was $440,000. This is where things got interesting. Their pitch is that with Zillow’s service, you would be provided with a dedicated selling advisor, the ability to sell without showings, the buyer would make repairs, and you get to choose your closing date. Zillow then proceeds to inform you, the client, that “all you receive” in a traditional sale is a dedicated selling advisor. When you continue to scroll down, Zillow quotes the average realtor’s commission at 6% and then says their Zillow Service Charge is 12.9%. To their credit, they don’t hide the fact that you will pay substantially more money using their service. At the bottom of the email, it estimated my net proceeds would be $383,240 using Zillow, and if I used a realtor proceeds would be roughly $413,600.